You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Quality Agreement TechnicalDocument35 pagesQuality Agreement TechnicalisralmayoorNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Estimating Lost Labor Productivity inDocument30 pagesEstimating Lost Labor Productivity inbulenthaticeyel100% (2)

- Zain Traders Assignment 2Document2 pagesZain Traders Assignment 2Bilal Ahmed100% (1)

- Project Report On PIA-SMDocument21 pagesProject Report On PIA-SMMohammad Usman Sheikh100% (1)

- HeinzDocument18 pagesHeinzkurtdias1No ratings yet

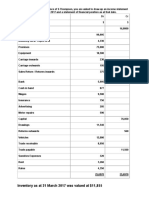

- Inventory As at 31 March 2017 Was Valued at $11,855Document2 pagesInventory As at 31 March 2017 Was Valued at $11,855Shoaib AslamNo ratings yet

- Accrued Expenses: Practice Question # 1Document4 pagesAccrued Expenses: Practice Question # 1Shoaib AslamNo ratings yet

- Scan 0002Document1 pageScan 0002Shoaib AslamNo ratings yet

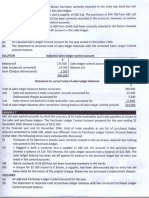

- Solution: 14.8 Advantages and Uses of Control AccountsDocument1 pageSolution: 14.8 Advantages and Uses of Control AccountsShoaib AslamNo ratings yet

- Control Accounts: Example 5Document1 pageControl Accounts: Example 5Shoaib AslamNo ratings yet

- Sample of Revision Plan - 10-cDocument3 pagesSample of Revision Plan - 10-cShoaib AslamNo ratings yet

- As Level Accounting Topic 1 OddDocument45 pagesAs Level Accounting Topic 1 OddShoaib AslamNo ratings yet

- Principles of Accounts: GCE Ordinary Level (2017) (Syllabus 7175)Document48 pagesPrinciples of Accounts: GCE Ordinary Level (2017) (Syllabus 7175)Shoaib AslamNo ratings yet

- Time Table IX M CrimsonDocument2 pagesTime Table IX M CrimsonShoaib AslamNo ratings yet

- DHS RFP Proposed DecisionDocument55 pagesDHS RFP Proposed DecisiondmronlineNo ratings yet

- SAP Success Factor Online TrainingDocument7 pagesSAP Success Factor Online Trainingharshali.allenticsNo ratings yet

- Virtual Worlds ExpoDocument5 pagesVirtual Worlds ExpoVirtualConf100% (1)

- Market PDFDocument30 pagesMarket PDFUzzalNo ratings yet

- Dissertation Proposal Name: Amanpreet Singh Course: MBA (Marketing)Document4 pagesDissertation Proposal Name: Amanpreet Singh Course: MBA (Marketing)Aman Singh Kailley50% (2)

- 21St Century Claims Processing For Insurance CompaniesDocument6 pages21St Century Claims Processing For Insurance CompanieszxxxNo ratings yet

- CH 14 - MCQ PDFDocument11 pagesCH 14 - MCQ PDFYAHIA ADELNo ratings yet

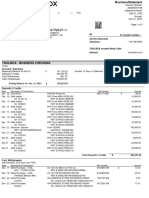

- HSBC Savings AccountDocument3 pagesHSBC Savings AccountLavanya VitNo ratings yet

- 2024 12 31 StatementDocument3 pages2024 12 31 StatementAlex NeziNo ratings yet

- KYC/AML - Introduction: 2013 ǀ ©polaris Financial Technology Ltd. ǀ Company ConfidentialDocument45 pagesKYC/AML - Introduction: 2013 ǀ ©polaris Financial Technology Ltd. ǀ Company Confidentiallokesh mishra100% (2)

- Jet Airways MRO MarketDocument16 pagesJet Airways MRO MarketRajat AgrawalNo ratings yet

- Step 1 - Enter Historical Financial Information: To Start - Download Our Free DCF Model Template in ExcelDocument15 pagesStep 1 - Enter Historical Financial Information: To Start - Download Our Free DCF Model Template in Excelrafa manggalaNo ratings yet

- CObIT-ISF CoverageDocument14 pagesCObIT-ISF Coveragerobb35mmNo ratings yet

- Journal of Ship Research Paper SubmissionDocument6 pagesJournal of Ship Research Paper Submissionhjqojzakf100% (3)

- Production Planning: It's Meaning and Objectives!Document52 pagesProduction Planning: It's Meaning and Objectives!Gautam KocherNo ratings yet

- Business ProposalDocument2 pagesBusiness Proposalapi-578943264No ratings yet

- Financial StatementsDocument34 pagesFinancial StatementsRadha GanesanNo ratings yet

- Curriculum Table For Business AdministrationDocument2 pagesCurriculum Table For Business AdministrationUmarNo ratings yet

- Value ChainDocument12 pagesValue ChainRitika sharmaNo ratings yet

- Waris Raees (905) Hassan Sardaar (973) Project MarketingDocument19 pagesWaris Raees (905) Hassan Sardaar (973) Project Marketingafia malikNo ratings yet

- 1000 Word ProposalDocument5 pages1000 Word ProposalOluwadamilolaNo ratings yet

- Balram Vishwakarma FinalDocument47 pagesBalram Vishwakarma FinalDurgesh KumarNo ratings yet

- Absorption Costing (Or Full Costing) and Marginal CostingDocument11 pagesAbsorption Costing (Or Full Costing) and Marginal CostingCharsi Unprofessional BhaiNo ratings yet

- Steinhoff Report - Stellenbosch UniversityDocument22 pagesSteinhoff Report - Stellenbosch UniversityTich100% (1)

- Chapter 2 2012Document53 pagesChapter 2 2012Onur YamukNo ratings yet