You might also like

- Case Study - Financial ServiceDocument5 pagesCase Study - Financial ServiceNia ニア Mulyaningsih0% (1)

- Tugas Sipi Kelompok 5 - There Be Thieves in Texas!Document25 pagesTugas Sipi Kelompok 5 - There Be Thieves in Texas!wlseptiara100% (2)

- Jawaban Case B TexasDocument7 pagesJawaban Case B TexasGilangRamadhanNo ratings yet

- Case 5 LOD StudycoDocument1 pageCase 5 LOD StudycoImeldaNo ratings yet

- Case 2 Nothern DigitalDocument2 pagesCase 2 Nothern Digitalzzz202xNo ratings yet

- ERP Helps Productivity at Northern Digital IncDocument10 pagesERP Helps Productivity at Northern Digital IncLihin100% (1)

- Erm Appendix CDocument4 pagesErm Appendix CNatasha ChairaNo ratings yet

- Kasus MillerDocument3 pagesKasus MillerFirman NurzamanNo ratings yet

- Solutions/solution Manual15Document50 pagesSolutions/solution Manual15Bea BlancoNo ratings yet

- Unilever, Leader in Social Responsibility: E-135: Corporate Sustainability StrategyDocument4 pagesUnilever, Leader in Social Responsibility: E-135: Corporate Sustainability StrategyVictor TorresNo ratings yet

- Case 7 Three LODDocument6 pagesCase 7 Three LODPintonov PutraNo ratings yet

- Kuis Pararel AML Pra UAS Gsl2021RevDocument3 pagesKuis Pararel AML Pra UAS Gsl2021RevLula BellaNo ratings yet

- Chapter 3 IT at WorkDocument19 pagesChapter 3 IT at WorkfarisNo ratings yet

- CF Chap024Document25 pagesCF Chap024aziezoelNo ratings yet

- Chapter 15Document12 pagesChapter 15Zack ChongNo ratings yet

- SOAL 14 - 6: Prevention Appraisal Internal Failure External FailureDocument6 pagesSOAL 14 - 6: Prevention Appraisal Internal Failure External FailureIndra YeniNo ratings yet

- How Management Accounting Information Supports Decision MakingDocument36 pagesHow Management Accounting Information Supports Decision MakingZbRZivPQ51pEZ9PUNo ratings yet

- 6640 06102014 Summary Performance Measurement and Control Systems For Implementing StrategyDocument22 pages6640 06102014 Summary Performance Measurement and Control Systems For Implementing StrategyAzaan Kaul100% (2)

- Hertz Goes Wireless PG 252Document8 pagesHertz Goes Wireless PG 252Manisha PuriNo ratings yet

- 10 - 11 - 12 - Data Cruncher Plus InstructionDocument6 pages10 - 11 - 12 - Data Cruncher Plus InstructionatikasaNo ratings yet

- Chapter 5Document56 pagesChapter 5Sugim Winata Einstein100% (1)

- Chapter 13: Risk, Cost of Capital, and Capital Budgeting: Corporate Finance Ross, Westerfield, and JaffeDocument15 pagesChapter 13: Risk, Cost of Capital, and Capital Budgeting: Corporate Finance Ross, Westerfield, and JaffePháp NguyễnNo ratings yet

- Nutratask Inc Is A Pharmaceutical Manufacturer of Amino Acid Chelated Minerals andDocument3 pagesNutratask Inc Is A Pharmaceutical Manufacturer of Amino Acid Chelated Minerals andAmit PandeyNo ratings yet

- Credit Risk PT Telkom IndonesiaDocument4 pagesCredit Risk PT Telkom IndonesiaamadilaaNo ratings yet

- Albrecht 4e Student CH 13 Pertemuan 5Document10 pagesAlbrecht 4e Student CH 13 Pertemuan 5eugeniaNo ratings yet

- HRP Final PPT Seimens Case StudyDocument17 pagesHRP Final PPT Seimens Case StudyRohitNo ratings yet

- NYTDigitalDocument21 pagesNYTDigitalRuchi SainiNo ratings yet

- Financial Shenanigans: Dr. Howard M. SchilitDocument15 pagesFinancial Shenanigans: Dr. Howard M. SchilitAbdullah AdreesNo ratings yet

- Texas Instrument and Hewlett-PackardDocument3 pagesTexas Instrument and Hewlett-PackardMuhammad KamilNo ratings yet

- Mexico Covid 19 Case Study EnglishDocument63 pagesMexico Covid 19 Case Study EnglishutahNo ratings yet

- CH 15 Multinational OrganizationsDocument18 pagesCH 15 Multinational OrganizationsKentia PexiNo ratings yet

- Earnings Management & Different ScandalsDocument16 pagesEarnings Management & Different ScandalsHasnain MinhasNo ratings yet

- Siemens Team5Document8 pagesSiemens Team5nevin04No ratings yet

- Responsibility CentersDocument15 pagesResponsibility CentersAkashdeep GhummanNo ratings yet

- Professional Due CareDocument19 pagesProfessional Due CareIqbal LhutfiNo ratings yet

- Financial Shenanigans-Earning ManipulationDocument23 pagesFinancial Shenanigans-Earning ManipulationFani anitaNo ratings yet

- ISA 240: The Auditor's Responsibilities Related To Fraud in An Audit of Financial StatementsDocument25 pagesISA 240: The Auditor's Responsibilities Related To Fraud in An Audit of Financial StatementsIndriNo ratings yet

- ERP Helps Productivity at Northern Digital IncDocument10 pagesERP Helps Productivity at Northern Digital IncImeldaNo ratings yet

- Enron: The Accounting ScandalDocument20 pagesEnron: The Accounting ScandalPooja PitaleNo ratings yet

- David MillerDocument3 pagesDavid MillerClaire BesmanosNo ratings yet

- Sarboox ScooterDocument6 pagesSarboox ScooterNisa SuriantoNo ratings yet

- 420 Dominion PresentationDocument17 pages420 Dominion PresentationPingkan TaraditaNo ratings yet

- Manual Journal Entry Testing: Data Analytics and The Risk of FraudDocument14 pagesManual Journal Entry Testing: Data Analytics and The Risk of FraudArtho KasihNo ratings yet

- Mayora Indah TBK PDFDocument84 pagesMayora Indah TBK PDFsherlijulianiNo ratings yet

- Case 1: Anna'S Business IdeaDocument1 pageCase 1: Anna'S Business IdeaDivantri FaadhilahNo ratings yet

- Resume Chapter 1 Internal AuditDocument7 pagesResume Chapter 1 Internal AuditTommy Tia RaharjaNo ratings yet

- Kode Etik Akuntan Indonesia - SDWDocument122 pagesKode Etik Akuntan Indonesia - SDWDiah Ayu YunitasariNo ratings yet

- Tax Management On Outbond InvestmentDocument15 pagesTax Management On Outbond Investmentdummy yummyNo ratings yet

- Financial ShenanigansDocument24 pagesFinancial ShenaniganslordraiNo ratings yet

- Hoffman Discount Drug IncDocument1 pageHoffman Discount Drug IncJacky DoanNo ratings yet

- (Excel) Wilbur TinaACC650 T3Document1 page(Excel) Wilbur TinaACC650 T3Tina Marie WilburNo ratings yet

- Chapter 7Document46 pagesChapter 7Sugim Winata Einstein50% (2)

- Kolesnichenko OB Sunshine CaseDocument4 pagesKolesnichenko OB Sunshine CaseStanislav KolesnichenkoNo ratings yet

- Arens Auditing16e SM 11Document20 pagesArens Auditing16e SM 11김현중No ratings yet

- Chapter 14working Capital and Current Assets ManagementDocument1 pageChapter 14working Capital and Current Assets ManagementMaricris RellinNo ratings yet

- Pertemuan Asistensi 8 (Performance Measurement)Document2 pagesPertemuan Asistensi 8 (Performance Measurement)Sholkhi ArdiansyahNo ratings yet

- Levers of Control: Assessor Mengindikasikan Kebutuhan Yang Perlu DipenuhiDocument5 pagesLevers of Control: Assessor Mengindikasikan Kebutuhan Yang Perlu DipenuhiciciNo ratings yet

- 14 Kasus Kelemahan Dari Narasi Suatu Siklus AkuntansiDocument6 pages14 Kasus Kelemahan Dari Narasi Suatu Siklus AkuntansiAdi Prawira ArfanNo ratings yet

- Modul 10Document9 pagesModul 10Herdian KusumahNo ratings yet

- Wisconsin Special Counsel Gableman Election Integrity Investigation Interim ReportDocument25 pagesWisconsin Special Counsel Gableman Election Integrity Investigation Interim ReportUncoverDCNo ratings yet

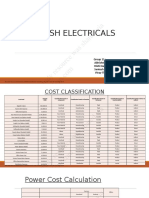

- Harsh Electricals: This Study Resource Was Shared ViaDocument9 pagesHarsh Electricals: This Study Resource Was Shared ViaPintonov PutraNo ratings yet

- AKEM 6.27 and 6.30, PINTONOV SULUNG PUTRADocument6 pagesAKEM 6.27 and 6.30, PINTONOV SULUNG PUTRAPintonov PutraNo ratings yet

- Case 7 Three LODDocument6 pagesCase 7 Three LODPintonov PutraNo ratings yet

- Tugas Studi Kasus 4 - ColorscopeDocument12 pagesTugas Studi Kasus 4 - ColorscopePintonov PutraNo ratings yet

- B1 B2 - Malala YousafzaiDocument5 pagesB1 B2 - Malala YousafzaiFlorencia SanseauNo ratings yet

- Also Known As : Free Trade Zones and Trade in ODSDocument4 pagesAlso Known As : Free Trade Zones and Trade in ODSaryanNo ratings yet

- Pol SC Class 12 Study MaterialDocument3 pagesPol SC Class 12 Study MaterialMuskan SandujaNo ratings yet

- Ravel Scarbo No 3Document20 pagesRavel Scarbo No 3Eugene Mironovich IosilevichNo ratings yet

- Unit 8 - Collective BargainingDocument8 pagesUnit 8 - Collective BargainingDylan BanksNo ratings yet

- Tejada vs. PalanaDocument4 pagesTejada vs. PalanaBowthen BoocNo ratings yet

- Unit-4 Cloud ComputingDocument11 pagesUnit-4 Cloud ComputingMansi JadonNo ratings yet

- Analysis of Rizal's WorksDocument9 pagesAnalysis of Rizal's WorksJeny Rose Bayate QuirogNo ratings yet

- 6 Melgar v. People (2018)Document2 pages6 Melgar v. People (2018)CedrickNo ratings yet

- Usurpation of Real Property With RapeDocument3 pagesUsurpation of Real Property With RapeNorberto Pilotin100% (1)

- Stéphane Legrand - Foucault's Forgotten MarxismDocument20 pagesStéphane Legrand - Foucault's Forgotten MarxismSebastian LeonNo ratings yet

- Expansionism Monroe DoctrineDocument23 pagesExpansionism Monroe Doctrineapi-3699641No ratings yet

- ACI 347R-14, Guide To Formwork For ConcreteDocument40 pagesACI 347R-14, Guide To Formwork For Concretejxsnyder100% (1)

- Harvard Model United Nations 2022: A Background Guide For Community of Latin American and Caribbean StatesDocument56 pagesHarvard Model United Nations 2022: A Background Guide For Community of Latin American and Caribbean StatesSebastián AguilarNo ratings yet

- Ins Eng SR 25957Document1 pageIns Eng SR 25957km0722312No ratings yet

- Philippine Christian University College of Arts, Sciences and Social Work Department of English and Mass CommunicationDocument4 pagesPhilippine Christian University College of Arts, Sciences and Social Work Department of English and Mass CommunicationAngel HernandoNo ratings yet

- Module 5Document15 pagesModule 5Pedro Reyes100% (1)

- LineamientosDocument133 pagesLineamientosnari lemaNo ratings yet

- Bruce B. Weber: Revised Term AppointmentDocument2 pagesBruce B. Weber: Revised Term AppointmentMatt BrownNo ratings yet

- KingshipmamDocument34 pagesKingshipmamShiwanjali kawaleNo ratings yet

- Cofield v. United States, 360 U.S. 472 (1959)Document1 pageCofield v. United States, 360 U.S. 472 (1959)Scribd Government DocsNo ratings yet

- Barangay Anti-Drug Abuse CouncilDocument19 pagesBarangay Anti-Drug Abuse Councilmykz zykm100% (1)

- Water and The (Infra-) Structure of Political Rule: A SynthesisDocument17 pagesWater and The (Infra-) Structure of Political Rule: A SynthesisMarie CandauNo ratings yet

- Luciano Vs Estrella Et - AlDocument2 pagesLuciano Vs Estrella Et - AlElijah B BersabalNo ratings yet

- State Street Bank & Trust Co. v. Signature Financial Group, Inc., 149 F.3d 1368, 47 U.S.P.Q.2d 1596 (Fed. Cir. 1998) (Re: Business Method Exception)Document2 pagesState Street Bank & Trust Co. v. Signature Financial Group, Inc., 149 F.3d 1368, 47 U.S.P.Q.2d 1596 (Fed. Cir. 1998) (Re: Business Method Exception)Eugene LabellaNo ratings yet

- National Difference in Business EthicsDocument5 pagesNational Difference in Business EthicsVinay Ramane100% (2)

- CRIME MAPPING C-WPS OfficeDocument4 pagesCRIME MAPPING C-WPS OfficeIvylen Gupid Japos CabudbudNo ratings yet

- Aggregate Costing For MatarbariDocument1 pageAggregate Costing For Matarbarihabib rahman100% (1)

- Union Manufacturing Co Case GR 27932Document3 pagesUnion Manufacturing Co Case GR 27932Alvin-Evelyn GuloyNo ratings yet

- Motion For Summary JudgmentDocument43 pagesMotion For Summary JudgmentLisa Lisa100% (4)