You might also like

- Consumer Law Cheatsheet 2Document3 pagesConsumer Law Cheatsheet 2Josh Campbell100% (11)

- Stop Paying Affidavit (Template)Document3 pagesStop Paying Affidavit (Template)Akil Bey93% (28)

- 15 U.S. Code 1635 - Right of Rescission As To Certain TransactionsDocument7 pages15 U.S. Code 1635 - Right of Rescission As To Certain TransactionsHelpin Hand100% (6)

- Truth in Lending - Affidavit - TemplateDocument12 pagesTruth in Lending - Affidavit - TemplateMarsha Maines100% (14)

- Notice of RescissionDocument1 pageNotice of RescissionArmond Trakarian100% (1)

- FDCPA Sample ComplaintDocument7 pagesFDCPA Sample ComplaintIdont Haveaface100% (10)

- Billing ErrorDocument1 pageBilling ErrorKNOWLEDGE SOURCE100% (1)

- Fight Debt Collectors and Win: Win the Fight With Debt CollectorsFrom EverandFight Debt Collectors and Win: Win the Fight With Debt CollectorsRating: 5 out of 5 stars5/5 (12)

- Tila Right of Rescission and ConsequencesDocument7 pagesTila Right of Rescission and Consequencesboss4him100% (9)

- Rescind Your Loan Under TILA in Bankruptcy CourtDocument10 pagesRescind Your Loan Under TILA in Bankruptcy CourtCarrieonic91% (11)

- Truth in Lending Affidavit 02 07 12Document8 pagesTruth in Lending Affidavit 02 07 12xfritz100% (13)

- Step 1. Notice of Right To CancelDocument3 pagesStep 1. Notice of Right To Cancellabellaby100% (5)

- Sample Notice of Rescission Under Truth in Lending ActDocument2 pagesSample Notice of Rescission Under Truth in Lending ActStan Burman100% (12)

- Right of Recission ReportDocument15 pagesRight of Recission Reportwebuyhouses4782100% (3)

- Contracts DefinitionsDocument19 pagesContracts DefinitionsAaron Smith100% (1)

- Violations of The Fair Debt Collection Practices Act (Fdcpa)Document7 pagesViolations of The Fair Debt Collection Practices Act (Fdcpa)sawasinc75% (4)

- Prove A Creditor Is in Violation - Automatic Win For $1000Document7 pagesProve A Creditor Is in Violation - Automatic Win For $1000FreedomofMind100% (12)

- Using RICO To Handle Debt CollectorsDocument19 pagesUsing RICO To Handle Debt CollectorsRandy Rosado100% (10)

- TIPS On How To Respond To A Collection LawsuitDocument8 pagesTIPS On How To Respond To A Collection LawsuitWXYZ-TV Channel 7 Detroit100% (3)

- 46 Consumer Reporting Agencies Investigating YouFrom Everand46 Consumer Reporting Agencies Investigating YouRating: 4.5 out of 5 stars4.5/5 (6)

- Class V III ProspectusDocument209 pagesClass V III ProspectusCarrieonicNo ratings yet

- Avida ContractDocument7 pagesAvida ContractTeamon MallariNo ratings yet

- Damages For FDCPA ViolationsDocument9 pagesDamages For FDCPA Violationscj100% (12)

- Section 1637 - Open End Consumer Credit PlansDocument19 pagesSection 1637 - Open End Consumer Credit PlansSamuel75% (4)

- Truth in Lending Act Case LawDocument5 pagesTruth in Lending Act Case Lawdbush2778100% (2)

- How to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersFrom EverandHow to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersRating: 3 out of 5 stars3/5 (1)

- Debtors Remedies For Creditors WrongsDocument173 pagesDebtors Remedies For Creditors Wrongscyrusdh100% (4)

- Have Fun With Debt CollectorsDocument3 pagesHave Fun With Debt CollectorsTitle IV-D Man with a plan94% (17)

- Find Respa, Tila Fdcpa Fcra Violation CaselawDocument14 pagesFind Respa, Tila Fdcpa Fcra Violation CaselawDeon Thomas100% (1)

- Notice of Cancelation of LoanDocument7 pagesNotice of Cancelation of LoanJulie Hatcher-Julie Munoz Jackson100% (9)

- 15 USC 1635 - Right of Rescission As To Certain TransactionsDocument4 pages15 USC 1635 - Right of Rescission As To Certain TransactionslostvikingNo ratings yet

- Using Court Procedure To Defeat Debt Collectors 12-24-13 NOTESDocument10 pagesUsing Court Procedure To Defeat Debt Collectors 12-24-13 NOTESTRISTARUSA100% (18)

- Reg ZDocument62 pagesReg ZYolanda Lewis100% (1)

- 14 Debt ValidationDocument6 pages14 Debt Validationstarhoney82% (11)

- Doctrine of Clog and FettersDocument10 pagesDoctrine of Clog and FettersGautam Jayasurya100% (1)

- US Consumer Debt Relief: Industry, Overview, Laws & RegulationsFrom EverandUS Consumer Debt Relief: Industry, Overview, Laws & RegulationsNo ratings yet

- Truth in Lending Complaint SampleDocument3 pagesTruth in Lending Complaint SampleCarrieonic100% (3)

- TILA Mortgage RescissionDocument3 pagesTILA Mortgage Rescissionklg_consultant868833% (3)

- TILA Rescission Success Without Tender - HENRY BOTELHO, Plaintiff, V. U.S. BANK, N.a., As Trustee For The LXS 2007-4N Trust, DefendantDocument6 pagesTILA Rescission Success Without Tender - HENRY BOTELHO, Plaintiff, V. U.S. BANK, N.a., As Trustee For The LXS 2007-4N Trust, DefendantForeclosure Fraud100% (4)

- Tila Rescission - Rights and ConsequencesDocument8 pagesTila Rescission - Rights and ConsequencesTA WebsterNo ratings yet

- Fcra and FdcpaDocument4 pagesFcra and FdcpaFreedomofMind100% (1)

- RescissionNotice Fin Charge COMPLAINTDocument23 pagesRescissionNotice Fin Charge COMPLAINTLoanClosingAuditors100% (1)

- FDCPA ComplaintDocument5 pagesFDCPA ComplaintJesse Sweeney100% (4)

- DEBT COLLECTOR VIOLATIONS (1692g)Document9 pagesDEBT COLLECTOR VIOLATIONS (1692g)SLAVEFATHER100% (1)

- Form For Filing FDCPA Law SuitDocument18 pagesForm For Filing FDCPA Law Suitnutech18100% (2)

- TilaDocument83 pagesTilafisherre2000100% (1)

- Unsecured DebtDocument14 pagesUnsecured Debtapi-374440893% (15)

- TILA Regulators HandbookDocument137 pagesTILA Regulators HandbookCarrieonic100% (1)

- FDCPA FraudDocument44 pagesFDCPA FraudJeff Wilner92% (26)

- 15 Us Code Subchapter V Debt Collection Practices Very Basic Version With Keywords in Red 05012017Document9 pages15 Us Code Subchapter V Debt Collection Practices Very Basic Version With Keywords in Red 05012017api-356589607100% (5)

- 1C6-Truth in Lending ActDocument92 pages1C6-Truth in Lending Actmoor2010No ratings yet

- Notice of (Cancellation), (Revocation of Power of Attorney), and (Removal of Trustee and Beneficiary)Document2 pagesNotice of (Cancellation), (Revocation of Power of Attorney), and (Removal of Trustee and Beneficiary)hramcorp100% (7)

- Scribd Debt Collection LetterDocument4 pagesScribd Debt Collection LetterquickthoughtzNo ratings yet

- Consumer Protection OutlineDocument35 pagesConsumer Protection OutlineBrady Williams50% (2)

- Consumer IssuesDocument67 pagesConsumer IssuesWarriorpoet100% (2)

- Debt Collector DefenseDocument58 pagesDebt Collector DefenseClay Driskill100% (11)

- FDCPA Litigation Example 01Document67 pagesFDCPA Litigation Example 01Jeff Wilner100% (11)

- The Ultimate Weapon in Debt Elimination: Unlocking the Secrets in Debt EliminationFrom EverandThe Ultimate Weapon in Debt Elimination: Unlocking the Secrets in Debt EliminationRating: 5 out of 5 stars5/5 (1)

- Debt Cleanse: How To Settle Your Unaffordable Debts for Pennies on the Dollar (And Not Pay Some At All)From EverandDebt Cleanse: How To Settle Your Unaffordable Debts for Pennies on the Dollar (And Not Pay Some At All)Rating: 3 out of 5 stars3/5 (1)

- Legal Consumer Tips and Secrets: Avoiding Debtors’ Prison in the United StatesFrom EverandLegal Consumer Tips and Secrets: Avoiding Debtors’ Prison in the United StatesNo ratings yet

- Outline Foreclosure Defense - Tila & RespaDocument13 pagesOutline Foreclosure Defense - Tila & RespaEdward BrownNo ratings yet

- World Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013Document8 pagesWorld Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013CarrieonicNo ratings yet

- SEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214Document21 pagesSEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214CarrieonicNo ratings yet

- Fannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC2Document50 pagesFannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC283jjmackNo ratings yet

- Citigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SDocument5 pagesCitigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SCarrieonicNo ratings yet

- Bloomberg Markets Magazine - Citifraud July 2012Document10 pagesBloomberg Markets Magazine - Citifraud July 2012CarrieonicNo ratings yet

- FCA Citi Mortgage Complaint-In-InterventionDocument36 pagesFCA Citi Mortgage Complaint-In-InterventionjodiebrittNo ratings yet

- In RE CitiGroup Inc Securities Litigation 1Document547 pagesIn RE CitiGroup Inc Securities Litigation 1CarrieonicNo ratings yet

- FHFA V Citigroup Inc. (09-02-11)Document95 pagesFHFA V Citigroup Inc. (09-02-11)Master ChiefNo ratings yet

- r01c 079901Document522 pagesr01c 079901CarrieonicNo ratings yet

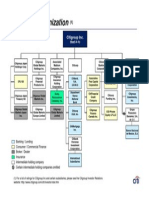

- Corp Struct CitigroupDocument1 pageCorp Struct CitigroupCarrieonicNo ratings yet

- Citi V SMITH WDocument4 pagesCiti V SMITH WCarrieonicNo ratings yet

- Citi Portfolio CorpDocument2 pagesCiti Portfolio CorpCarrieonicNo ratings yet

- Citi Subsidiarys 2010 Exhibit 21-01Document4 pagesCiti Subsidiarys 2010 Exhibit 21-01CarrieonicNo ratings yet

- Subsidiarys of Citigroup Inc. 2009 Exhibit21-01Document5 pagesSubsidiarys of Citigroup Inc. 2009 Exhibit21-01CarrieonicNo ratings yet

- Great Pacific Life Insurance v. CA - G.R. No. 113899 - Oct. 13, 1999Document2 pagesGreat Pacific Life Insurance v. CA - G.R. No. 113899 - Oct. 13, 1999Princess FaithNo ratings yet

- Features of A CompanyDocument4 pagesFeatures of A CompanyMostafa Ahmed SuntuNo ratings yet

- Philippine Health Care Providers VS CirDocument3 pagesPhilippine Health Care Providers VS CirClaudine Christine A. VicenteNo ratings yet

- Scheme For Financing of Industrial LandDocument3 pagesScheme For Financing of Industrial LandkamshaarmaNo ratings yet

- Independent Contractor Agreement SimpleDocument2 pagesIndependent Contractor Agreement SimplePhoebe Grace LopezNo ratings yet

- Chapter 14 PP 2nd Ed - 3 - Business and IP LawDocument27 pagesChapter 14 PP 2nd Ed - 3 - Business and IP LawUyen ThuNo ratings yet

- Business Law II Course OutlineDocument3 pagesBusiness Law II Course Outlinefrancis kaburuNo ratings yet

- TRansfer of PropertyDocument24 pagesTRansfer of PropertySwapna SinghNo ratings yet

- Chattel Mortgage SampleDocument2 pagesChattel Mortgage SamplerbonNo ratings yet

- Salomon V Salomon Case SummaryDocument6 pagesSalomon V Salomon Case SummaryAnirban ChakrabortyNo ratings yet

- Commercial Agency Agreement in MiddleEast, Setup Services For ForeignersDocument1 pageCommercial Agency Agreement in MiddleEast, Setup Services For Foreignersfortune xiuNo ratings yet

- 1L Contracts Outline (2 Semesters)Document7 pages1L Contracts Outline (2 Semesters)Natalie BakerNo ratings yet

- Lifting of The Corporate VeilDocument33 pagesLifting of The Corporate VeilEric Foo100% (2)

- Franchise Problems For DiscussionDocument4 pagesFranchise Problems For DiscussionRAGASA, John Carlo R.No ratings yet

- W5 ADDRESS SolutionDocument169 pagesW5 ADDRESS SolutionDemontre BeckettNo ratings yet

- Principles of Business Legal Aspects of A Business QuestionsDocument4 pagesPrinciples of Business Legal Aspects of A Business QuestionsKenoi HallNo ratings yet

- Bankruptcy Dismissal For Lone Ranger Holdings The Dwight Jory CompanyDocument5 pagesBankruptcy Dismissal For Lone Ranger Holdings The Dwight Jory CompanybelievethingsNo ratings yet

- CGVG International EnglishDocument3 pagesCGVG International EnglishBENILDA CAMASONo ratings yet

- Name - Rounak Jain ROLL NO - 20194442 Business Law Assignment - 1Document2 pagesName - Rounak Jain ROLL NO - 20194442 Business Law Assignment - 1NAMAN PRAKASHNo ratings yet

- Module 1 - Unit 2Document20 pagesModule 1 - Unit 2AlishaNo ratings yet

- SEGURO Redpoint CompanyDocument1 pageSEGURO Redpoint CompanyJim ShortNo ratings yet

- False. Because According To Art. 52.1. Except For The Cases Specified in Clause 4Document4 pagesFalse. Because According To Art. 52.1. Except For The Cases Specified in Clause 4Cu Thi Hong NhungNo ratings yet

- RFBT - Confusion or Merger of RightsDocument27 pagesRFBT - Confusion or Merger of RightsSherry AnnNo ratings yet

- Ang Vs Associated Bank E. Accomodation PartyDocument4 pagesAng Vs Associated Bank E. Accomodation Partydnel13No ratings yet

- Dissolution and Winding UpDocument16 pagesDissolution and Winding Upma.catherine merillenoNo ratings yet

- ERA Admin Manual 6Document188 pagesERA Admin Manual 6EdomNo ratings yet

- Oblicon QuestionsDocument2 pagesOblicon QuestionsGirlie SisonNo ratings yet