You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Solution Manual For Economics 22nd Edition Campbell Mcconnell Stanley Brue Sean FlynnDocument36 pagesSolution Manual For Economics 22nd Edition Campbell Mcconnell Stanley Brue Sean Flynnbethinkseptaned1zl7100% (30)

- Gyratory Crusher Reference List 20170619Document7 pagesGyratory Crusher Reference List 20170619Maruja Abigail Dominguez SalazarNo ratings yet

- DPWH Structural 01Document9 pagesDPWH Structural 01AndengBaduriaNo ratings yet

- Chap 1 Intro of BookkeepDocument14 pagesChap 1 Intro of BookkeepTan Shu YuinNo ratings yet

- Assignment With Solutions Day 4Document13 pagesAssignment With Solutions Day 4HIMANSHU Ak MISRANo ratings yet

- Resúmenes Del Debate BullionistaDocument21 pagesResúmenes Del Debate BullionistaJavi TolentinoNo ratings yet

- Faisalabad Electric Supply Company: Govt ConnectionDocument2 pagesFaisalabad Electric Supply Company: Govt ConnectionM Aqeel Ahmad KalyarNo ratings yet

- Bernette B05 Academy Sewing Machine Instruction ManualDocument82 pagesBernette B05 Academy Sewing Machine Instruction ManualiliiexpugnansNo ratings yet

- The Role of Transaction Advisers in A PPP Project PDFDocument15 pagesThe Role of Transaction Advisers in A PPP Project PDFOladunni AfolabiNo ratings yet

- Estimation and Hypothesis Testing: Two Populations: Prem Mann, Introductory Statistics, 7/EDocument75 pagesEstimation and Hypothesis Testing: Two Populations: Prem Mann, Introductory Statistics, 7/ETanvir AhmedNo ratings yet

- Econ Cheat SheetDocument3 pagesEcon Cheat SheetLarryNo ratings yet

- Auction Properties 16-06-2022Document115 pagesAuction Properties 16-06-2022Ramana ReddyNo ratings yet

- Foundations of Financial Management 16th Edition Block Test BankDocument35 pagesFoundations of Financial Management 16th Edition Block Test Bankwinifredholmesl39o6z100% (25)

- NCAHFSDocument1 pageNCAHFSPatricia San PabloNo ratings yet

- Deed of Sale of LandDocument9 pagesDeed of Sale of Landnoemi melayaNo ratings yet

- A Proposed Mactan Amusement Park: Analee Borres QuiapoDocument1 pageA Proposed Mactan Amusement Park: Analee Borres Quiapofppalawan plansNo ratings yet

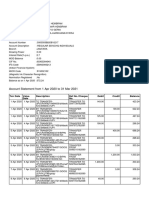

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNo ratings yet

- Excerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalDocument34 pagesExcerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalKaren PerezNo ratings yet

- RFL Lined Ball ValveDocument4 pagesRFL Lined Ball ValveRasaii Flow Lines Pvt. LtdNo ratings yet

- MC311 - Size LDocument30 pagesMC311 - Size LuyenmoclenNo ratings yet

- Fisa Tehnica Autocolant Furnir LemnDocument1 pageFisa Tehnica Autocolant Furnir LemnCatalina PopNo ratings yet

- 3BS (G)Document7 pages3BS (G)Vijay KrishnaNo ratings yet

- 203 - Engineering Eco 1 - IntroductionDocument21 pages203 - Engineering Eco 1 - IntroductionNPCNo ratings yet

- 1 - GDP Per CapitaDocument28 pages1 - GDP Per CapitaTrung TạNo ratings yet

- Story of A GarmentDocument14 pagesStory of A GarmentArunraj ArumugamNo ratings yet

- WA Minerals Fees & Charges - 2023Document2 pagesWA Minerals Fees & Charges - 2023aracgx9900No ratings yet

- Y11 MAA SL-Venn DiagramDocument9 pagesY11 MAA SL-Venn DiagramKezia TjandraNo ratings yet

- Traffic Impact Analysis of Urban Construction Projects Based On Traffic SimulationDocument5 pagesTraffic Impact Analysis of Urban Construction Projects Based On Traffic SimulationSasi KumarNo ratings yet

- PC-16 - Rahi - Corrigendum (Revisioni in Ans Key)Document1 pagePC-16 - Rahi - Corrigendum (Revisioni in Ans Key)Virendra RamtekeNo ratings yet

- Hazel Bumanglag Salomon: Employment HistoryDocument1 pageHazel Bumanglag Salomon: Employment HistoryJOEFRAN ENRIQUEZNo ratings yet