You might also like

- Cash Flow Estimation Brigham Case SolutionDocument8 pagesCash Flow Estimation Brigham Case SolutionShahid MehmoodNo ratings yet

- Chapter 4 Text ProblemsDocument9 pagesChapter 4 Text ProblemsAnatasyaOktavianiHandriatiTataNo ratings yet

- Be Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItDocument6 pagesBe Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItSalman KhalidNo ratings yet

- S A Ipcc Nov 2011 - GR IDocument97 pagesS A Ipcc Nov 2011 - GR ISaibhumi100% (1)

- JRE300-April 2015 - Final Exam - SOLUTIONS KEYDocument11 pagesJRE300-April 2015 - Final Exam - SOLUTIONS KEYSCR PpelusaNo ratings yet

- IS628 DSS AssnDocument3 pagesIS628 DSS AssnArnold MatamboNo ratings yet

- MCO-05 ENG IgnouDocument51 pagesMCO-05 ENG Ignousanthi0% (1)

- Accounting IAS Model Answers Series 2 2010Document17 pagesAccounting IAS Model Answers Series 2 2010Aung Zaw HtweNo ratings yet

- 7-Completing The Accounting CycleDocument12 pages7-Completing The Accounting Cyclechobiipiggy26No ratings yet

- AP Module 01 - Accounting Changes and ErrorsDocument10 pagesAP Module 01 - Accounting Changes and ErrorsjasfNo ratings yet

- Solution Class 12 - Accountancy Full Paper Accounts: For Admission Contact 1 / 16Document16 pagesSolution Class 12 - Accountancy Full Paper Accounts: For Admission Contact 1 / 16Shaindra SinghNo ratings yet

- Midterm 2004Document12 pagesMidterm 2004Mạnh VănNo ratings yet

- PREP COF Sample Exam QuestionsDocument10 pagesPREP COF Sample Exam QuestionsLNo ratings yet

- Accounting Assignment Sample SolutionsDocument20 pagesAccounting Assignment Sample SolutionsHebrew JohnsonNo ratings yet

- Ac100 - 2008Document15 pagesAc100 - 2008jacqueline.x3No ratings yet

- Dr-Ayanlade-Tutorial - QuestionsDocument4 pagesDr-Ayanlade-Tutorial - QuestionsAkunwa GideonNo ratings yet

- ROI TecnologiasDocument27 pagesROI TecnologiasDiego SornozaNo ratings yet

- DepreciationDocument3 pagesDepreciationSumanth KumarNo ratings yet

- ACCT1200 (Fall 20) Lecture & Tutorial 5 Accounting Cycle 3Document9 pagesACCT1200 (Fall 20) Lecture & Tutorial 5 Accounting Cycle 3Lyaman TagizadeNo ratings yet

- Page 226 236 - Lyka Mae AdluzDocument9 pagesPage 226 236 - Lyka Mae AdluzWendell Maverick MasuhayNo ratings yet

- LixingcunDocument7 pagesLixingcunmuhammad iman bin kamarudinNo ratings yet

- F5 Division Roi RiDocument16 pagesF5 Division Roi RiMazni Hanisah100% (1)

- Financial ProjectionDocument29 pagesFinancial ProjectionAghitsni diliandri TimoriesNo ratings yet

- CH 11 - CF Estimation Mini Case Sols Word 1514edDocument13 pagesCH 11 - CF Estimation Mini Case Sols Word 1514edHari CahyoNo ratings yet

- Financial Analysis 4Document10 pagesFinancial Analysis 4Alaitz GNo ratings yet

- Depreciation Lesson 8Document39 pagesDepreciation Lesson 8Charos Aslonovna100% (5)

- 256 - MCO-5 - ENG D18 - CompressedDocument3 pages256 - MCO-5 - ENG D18 - CompressedTushar SharmaNo ratings yet

- ABC MedTech ROIDocument27 pagesABC MedTech ROIWei ZhangNo ratings yet

- District Resource Centre Mahbubnagar:, Pre-Final Examinations - Jan / Feb - 2011 Management AccountingDocument5 pagesDistrict Resource Centre Mahbubnagar:, Pre-Final Examinations - Jan / Feb - 2011 Management Accountingtadepalli patanjaliNo ratings yet

- A Level AccountingDocument5 pagesA Level AccountingMichal DomanskiNo ratings yet

- AC3193 ZA Final For UoLDocument9 pagesAC3193 ZA Final For UoLRigged RiggedNo ratings yet

- MANAGEMENT ACCOUNTING & CONTROL 306 Ele Paper IIIDocument5 pagesMANAGEMENT ACCOUNTING & CONTROL 306 Ele Paper IIItadepalli patanjaliNo ratings yet

- Sap NotesDocument38 pagesSap NotesJyotirmay SahuNo ratings yet

- Sap FicoDocument43 pagesSap FicoDhiraj PawarNo ratings yet

- Class DocsDocument32 pagesClass Docsgeorge antwiNo ratings yet

- Department of Commerce, Bahauddin Zakariya University, Multan Instructions For The ExamDocument1 pageDepartment of Commerce, Bahauddin Zakariya University, Multan Instructions For The ExamTHIND TAXLAWNo ratings yet

- Financial Statements - II: 360 AccountancyDocument65 pagesFinancial Statements - II: 360 AccountancyshantX100% (1)

- Class Examples SolutionsDocument4 pagesClass Examples Solutionsgwbadie7No ratings yet

- BUS 6140 6141 Mod 4 WorksheetDocument27 pagesBUS 6140 6141 Mod 4 WorksheetBryan MooreNo ratings yet

- 18-Arid-879 Managerial Accounting Final Ter Examination MGT-504 Syeda Tashifa Batool BBA 4th (B)Document9 pages18-Arid-879 Managerial Accounting Final Ter Examination MGT-504 Syeda Tashifa Batool BBA 4th (B)Syed Muhammed Sabeehul RehmanNo ratings yet

- AF208 FE S1 2019 Revision Package - QPDocument27 pagesAF208 FE S1 2019 Revision Package - QPRavinesh Amit PrasadNo ratings yet

- ACCA F9 Mock Examination 2Document5 pagesACCA F9 Mock Examination 2daria0% (1)

- Preview of Chapter Section 2 5Document65 pagesPreview of Chapter Section 2 5fentaw melkieNo ratings yet

- Paper - 5: Advanced Management Accounting Questions Limiting FactorDocument24 pagesPaper - 5: Advanced Management Accounting Questions Limiting FactorMohit MaheshwariNo ratings yet

- Paper - 5: Advanced Management Accounting Questions Limiting FactorDocument24 pagesPaper - 5: Advanced Management Accounting Questions Limiting FactorSrihariNo ratings yet

- Chapter 10 0Document39 pagesChapter 10 0Jennifer M. Ramos EnríquezNo ratings yet

- Be Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItDocument9 pagesBe Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItĐào Quốc AnhNo ratings yet

- Practice Questions (Not in Prescribed Textbook)Document7 pagesPractice Questions (Not in Prescribed Textbook)ayaNo ratings yet

- Lesson 13 Worksheet-1Document14 pagesLesson 13 Worksheet-1Slay MontefalcoNo ratings yet

- Accounting Chapter 5Document24 pagesAccounting Chapter 5Will TrầnNo ratings yet

- Quiz 3 Cap Budgeting Cap Structure Valuation Expanded Student VersionDocument21 pagesQuiz 3 Cap Budgeting Cap Structure Valuation Expanded Student Versionsalehaiman2019No ratings yet

- CPG PDFDocument20 pagesCPG PDFRehman MuzaffarNo ratings yet

- First 1302020Document9 pagesFirst 1302020fNo ratings yet

- Additional Illustratiions 2Document14 pagesAdditional Illustratiions 2Naman ChotiaNo ratings yet

- XYZ Energy ROIDocument27 pagesXYZ Energy ROIWei ZhangNo ratings yet

- 2203 BIZ201 Assessment 3 BriefDocument8 pages2203 BIZ201 Assessment 3 BriefAkshita ChordiaNo ratings yet

- Class 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIDocument70 pagesClass 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIPathan KausarNo ratings yet

- Ch2b Accounting TransactionDocument58 pagesCh2b Accounting TransactionLizette Janiya SumantingNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Direct Materials Used: Direct Material Inventory, January 2019Document2 pagesDirect Materials Used: Direct Material Inventory, January 2019Arina FelitaNo ratings yet

- Logical and Physical Views of DataDocument2 pagesLogical and Physical Views of DataArina FelitaNo ratings yet

- Rais12 SM CH03Document46 pagesRais12 SM CH03Bima Adetya90% (10)

- Problem No 5-4Document3 pagesProblem No 5-4Arina FelitaNo ratings yet

- IaDocument5 pagesIaArina FelitaNo ratings yet

- NODocument2 pagesNOArina FelitaNo ratings yet

- XXDocument2 pagesXXArina FelitaNo ratings yet

- IaDocument5 pagesIaArina FelitaNo ratings yet

- A. Unit Cost For Job 701Document2 pagesA. Unit Cost For Job 701Arina FelitaNo ratings yet

- FergusonDocument2 pagesFergusonArina FelitaNo ratings yet

- Differential Costs 5 2,500,000Document2 pagesDifferential Costs 5 2,500,000Arina FelitaNo ratings yet

- Audit Universe Time and Resources Limitations AuditDocument2 pagesAudit Universe Time and Resources Limitations AuditArina FelitaNo ratings yet

- Description - True Value and Social ValueDocument46 pagesDescription - True Value and Social ValueArina FelitaNo ratings yet

- BenchDocument2 pagesBenchArina FelitaNo ratings yet

- Collect Audit Evidence AppropriatelyDocument2 pagesCollect Audit Evidence AppropriatelyArina FelitaNo ratings yet

- Metric Value 1 - 5 Score 1 - 5 Metric Score Max. Value X Max. Score Metric %Document1 pageMetric Value 1 - 5 Score 1 - 5 Metric Score Max. Value X Max. Score Metric %Arina FelitaNo ratings yet

- General Meeting of ShareholdersDocument1 pageGeneral Meeting of ShareholdersArina FelitaNo ratings yet

- Aldi Brian - 12030117190228 - Quality Cost and SustainabilityDocument1 pageAldi Brian - 12030117190228 - Quality Cost and SustainabilityArina FelitaNo ratings yet

- Internal Audit Pt. Satria Putra Perkasa Maju BersamaDocument8 pagesInternal Audit Pt. Satria Putra Perkasa Maju BersamaArina FelitaNo ratings yet

- Unilever - Advertising & Marketing Management Function and Detail ListDocument1 pageUnilever - Advertising & Marketing Management Function and Detail ListArina FelitaNo ratings yet

- Steps in Internal AuditDocument2 pagesSteps in Internal AuditArina FelitaNo ratings yet

- Internal Control Framework: The COSO StandardDocument6 pagesInternal Control Framework: The COSO StandardArina FelitaNo ratings yet

- Definition of RiskDocument5 pagesDefinition of RiskArina FelitaNo ratings yet

- BU8201 Tutorial 1Document17 pagesBU8201 Tutorial 1Li Hui83% (6)

- BEDocument4 pagesBERhaiza PabelloNo ratings yet

- Subscriber Dispute FormDocument2 pagesSubscriber Dispute FormBryan BagayasNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document21 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Stella SabaoanNo ratings yet

- Financial Statement Analysis of ICICI Bank and A Comparative Study With Axis BankDocument7 pagesFinancial Statement Analysis of ICICI Bank and A Comparative Study With Axis Banksridharkar06100% (1)

- Govacc Finals DrillsDocument8 pagesGovacc Finals DrillsVon Andrei Medina100% (1)

- Cashflow A. Indirect Method: KM Manufacturing CompanyDocument2 pagesCashflow A. Indirect Method: KM Manufacturing CompanyArnold AdanoNo ratings yet

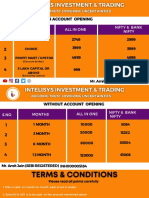

- Intelisys Pricing PlanDocument5 pagesIntelisys Pricing PlanregsNo ratings yet

- INVB6572Document24 pagesINVB6572János JuhászNo ratings yet

- Uday Project ReportDocument53 pagesUday Project ReportudayNo ratings yet

- Early Days of Investing: Ramdeo AggarwalDocument2 pagesEarly Days of Investing: Ramdeo AggarwalAditya SinghalNo ratings yet

- Origin and Evolution of Double Entry Bookkeeping A Study of Italian Practice From The Fourteenth Century by Edward Peragallo PDFDocument161 pagesOrigin and Evolution of Double Entry Bookkeeping A Study of Italian Practice From The Fourteenth Century by Edward Peragallo PDFDan PolakovicNo ratings yet

- Certified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasDocument63 pagesCertified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasAllen CarlNo ratings yet

- Documentation of Bank (Bank of Baroda)Document40 pagesDocumentation of Bank (Bank of Baroda)Devesh Verma100% (1)

- Introduction To BankingDocument24 pagesIntroduction To Bankingmihir kothariNo ratings yet

- Name of The Bank Ifsc Code Micr Code Branch NameDocument141 pagesName of The Bank Ifsc Code Micr Code Branch NameVijay BharathNo ratings yet

- Statement Details: Transaction Date Posting Date Description Debit Credit Posting Amount Posting Currency Auth CodeDocument2 pagesStatement Details: Transaction Date Posting Date Description Debit Credit Posting Amount Posting Currency Auth CodeTarek KareimNo ratings yet

- Debt To Total Asset RatioDocument13 pagesDebt To Total Asset RatioMjNo ratings yet

- FABM 1 Lesson 7 The Accounting EquationDocument19 pagesFABM 1 Lesson 7 The Accounting EquationTiffany Ceniza100% (1)

- Noncurrent AssetsDocument90 pagesNoncurrent Assetsfira tuapetelNo ratings yet

- Business Planning Taxation March 2023 ExamDocument10 pagesBusiness Planning Taxation March 2023 Examrwinchella2803No ratings yet

- Vodafone Quick BillPayDocument1 pageVodafone Quick BillPaysgplNo ratings yet

- Annuity Calculator: Withdrawal PlanDocument2 pagesAnnuity Calculator: Withdrawal Plansaurabhm590No ratings yet

- M-Pesa Corporate AccountsDocument6 pagesM-Pesa Corporate AccountsPeter K NjugunaNo ratings yet

- (BANKING LAWS) Classification of BanksDocument3 pages(BANKING LAWS) Classification of BanksZyril MarchanNo ratings yet

- The REIT Stuff: Investment ViewsDocument9 pagesThe REIT Stuff: Investment ViewsJerry ThngNo ratings yet

- Statement of Comprehensive Income (SCI) : Fabm IiDocument17 pagesStatement of Comprehensive Income (SCI) : Fabm IiAlyssa Nikki VersozaNo ratings yet

- Sebi 1234567890Document5 pagesSebi 1234567890John DaveNo ratings yet

- Dashboard Pinnacle CPA Review Study Guide (Sir Brad's Version)Document43 pagesDashboard Pinnacle CPA Review Study Guide (Sir Brad's Version)Mica TolentinoNo ratings yet

- Implementing Central Finance in SAP S4HANA S4F61 - EN - Col17 - 20Document1 pageImplementing Central Finance in SAP S4HANA S4F61 - EN - Col17 - 20sam kumarNo ratings yet