You might also like

- Audit of InventoriesDocument35 pagesAudit of InventoriesPau100% (2)

- Audit of Inventories, Investments, PpeDocument14 pagesAudit of Inventories, Investments, PpeconsulivyNo ratings yet

- Inv and CGSDocument19 pagesInv and CGSCOMMERCIAL OPERATIONNo ratings yet

- Audit ProceduresDocument36 pagesAudit ProceduresRoshaan AhmadNo ratings yet

- The Audit of InventoriesDocument6 pagesThe Audit of InventoriesIftekhar Ifte100% (3)

- Chapter 3Document7 pagesChapter 3Jarra AbdurahmanNo ratings yet

- 4-Auditing 2 - Chapter FourDocument8 pages4-Auditing 2 - Chapter Foursamuel debebeNo ratings yet

- Audit II Week 7Document15 pagesAudit II Week 7EfratianKristisonNo ratings yet

- Audit Inventory Warehousing CycleDocument9 pagesAudit Inventory Warehousing CycleREG.B/0115103003/ERSA KUSUMAWARDANINo ratings yet

- Auditing InventoriesDocument8 pagesAuditing Inventorieshabtamu tadesseNo ratings yet

- Receivables From An Audit Perspective?: 3.why Are Returns and Allowances Sensitive Issues in Receivables Audit?Document7 pagesReceivables From An Audit Perspective?: 3.why Are Returns and Allowances Sensitive Issues in Receivables Audit?Bekeri MohammedNo ratings yet

- Chapter 4 Auditing For Inventories and Cost of Goods SoldDocument3 pagesChapter 4 Auditing For Inventories and Cost of Goods SoldsteveiamidNo ratings yet

- Gold Audit/ Gold Inspection LmsDocument16 pagesGold Audit/ Gold Inspection LmsRaghu.GNo ratings yet

- The Audit of InventoriesDocument7 pagesThe Audit of InventoriesRae Alariao-CabicoNo ratings yet

- Audit-Of-Inventories - Highlights of Technical ClinicDocument4 pagesAudit-Of-Inventories - Highlights of Technical Clinicapi-256556206No ratings yet

- Chapter Four: 2. Audit of Inventory, Cost of Sales and Related AccountsDocument8 pagesChapter Four: 2. Audit of Inventory, Cost of Sales and Related AccountsZelalem HassenNo ratings yet

- Unit One: Accounting For Merchandising InventoriesDocument24 pagesUnit One: Accounting For Merchandising Inventoriesmelaku muka100% (1)

- I. Audit of Inventories of Retail and E-CommerceDocument4 pagesI. Audit of Inventories of Retail and E-CommerceRhea Joy OrcioNo ratings yet

- Presentation4 - Audit of Inventories, Cost of Sales and Other Related AccountsDocument19 pagesPresentation4 - Audit of Inventories, Cost of Sales and Other Related AccountsRoseanne Dela CruzNo ratings yet

- Audit II 4newDocument22 pagesAudit II 4newTesfaye Megiso BegajoNo ratings yet

- Comprehensive Problem 1Document5 pagesComprehensive Problem 1Coke Aidenry SaludoNo ratings yet

- Inventory Audit Procedures - AccountingToolsDocument2 pagesInventory Audit Procedures - AccountingToolsMd Rakibul HasanNo ratings yet

- Chapter 5 Inventory and Warehousing Cyle AuditDocument24 pagesChapter 5 Inventory and Warehousing Cyle AuditDawit WorkuNo ratings yet

- Chapter 4 Audit of Inventory and CGSDocument9 pagesChapter 4 Audit of Inventory and CGSminichelNo ratings yet

- Audit EvidanceDocument16 pagesAudit Evidancemiam67830No ratings yet

- Module 5 - Audit of InventoriesDocument23 pagesModule 5 - Audit of InventoriesIvan LandaosNo ratings yet

- ACREV 426 - AP 03 InventoryDocument8 pagesACREV 426 - AP 03 InventoryEdwin Jr KingNo ratings yet

- Audit of The Inventory and Warehousing Cycle Business Functions in The Cycle and Related Documents and RecordsDocument3 pagesAudit of The Inventory and Warehousing Cycle Business Functions in The Cycle and Related Documents and RecordsvvNo ratings yet

- Week 10lecture InventoryDocument34 pagesWeek 10lecture InventoryShalin LataNo ratings yet

- Lecture 7-Internal Control & AssertionsDocument6 pagesLecture 7-Internal Control & AssertionsFadil RushNo ratings yet

- InventoryDocument4 pagesInventoryPrio DebnathNo ratings yet

- Curs VI - Inventories - RetailDocument12 pagesCurs VI - Inventories - RetailSTANCIU DIANA-MIHAELANo ratings yet

- AC414 - Audit and Investigations II - Audit of InventoryDocument29 pagesAC414 - Audit and Investigations II - Audit of InventoryTsitsi AbigailNo ratings yet

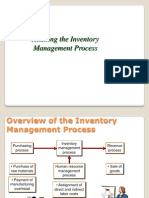

- Auditing The Inventory Management ProcessDocument15 pagesAuditing The Inventory Management ProcessGohar Mahmood100% (1)

- Chapter 1 (Updated) - Audit On Financial StatementDocument100 pagesChapter 1 (Updated) - Audit On Financial Statement黄勇添No ratings yet

- What Is Auditing InventoryDocument4 pagesWhat Is Auditing InventoryVertex DataNo ratings yet

- AC404 - Inventory and Production Cycle Class NotesDocument28 pagesAC404 - Inventory and Production Cycle Class NotesObey KamutsamombeNo ratings yet

- Reviewer 5- Audit of InventoriesDocument2 pagesReviewer 5- Audit of InventoriesCASAMAYOR JOVELYN B.No ratings yet

- Aud ch4Document9 pagesAud ch4kitababekele26No ratings yet

- Chapter Four-Auditing IIDocument9 pagesChapter Four-Auditing IIBantamkak FikaduNo ratings yet

- Auditing Inventories and Fixed AssetsDocument10 pagesAuditing Inventories and Fixed AssetsbeershebaNo ratings yet

- Backup of Chap008Document26 pagesBackup of Chap008Aeson Dela CruzNo ratings yet

- Aud - InventoriesDocument5 pagesAud - InventoriesKaila Mae Tan DuNo ratings yet

- Audit Procedure Lecture 4Document11 pagesAudit Procedure Lecture 4Farman UllahNo ratings yet

- Auditing-Review Questions Chapter 12Document4 pagesAuditing-Review Questions Chapter 12meiwin manihingNo ratings yet

- Audit Powerpoint PresentationDocument21 pagesAudit Powerpoint PresentationSmashed PotatoNo ratings yet

- Audit of InventoryDocument5 pagesAudit of InventoryMa. Hazel Donita DiazNo ratings yet

- ARIBA, Fretzyl Bless A. - Chapter 11 - Substantive Test of Inventories and Cost of Sales - ReflectionDocument3 pagesARIBA, Fretzyl Bless A. - Chapter 11 - Substantive Test of Inventories and Cost of Sales - ReflectionFretzyl JulyNo ratings yet

- Module 5 INVENTORIES AND RELATED EXPENSESDocument4 pagesModule 5 INVENTORIES AND RELATED EXPENSESNiño Mendoza MabatoNo ratings yet

- Chapter 21 Solutions ManualDocument28 pagesChapter 21 Solutions ManualDewiair100% (3)

- Assignment 4 Wida Widiawati 19AKJ 194020034Document6 pagesAssignment 4 Wida Widiawati 19AKJ 194020034wida widiawatiNo ratings yet

- PA603 - Audit ApproachDocument75 pagesPA603 - Audit ApproachnikazidaNo ratings yet

- Stores Accounting & Stock VerificationDocument8 pagesStores Accounting & Stock VerificationDhanraj KumawatNo ratings yet

- Notes Chapter 4 AUDDocument8 pagesNotes Chapter 4 AUDcpacfa100% (10)

- Auditing Inventory Valuation and Cutoff ProceduresDocument22 pagesAuditing Inventory Valuation and Cutoff ProceduressantaulinasitorusNo ratings yet

- Substantive Tests of Transactions and Account Balances EditedDocument85 pagesSubstantive Tests of Transactions and Account Balances EditedPiaElemos100% (2)

- AA Chapter21Document28 pagesAA Chapter21Jia Hui PekNo ratings yet

- Topic 34 Substantive Audit Procedures InventoryDocument10 pagesTopic 34 Substantive Audit Procedures InventoryRafik BelkahlaNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Perfect Pancake RecipesDocument3 pagesPerfect Pancake RecipesJesse NgaliNo ratings yet

- Introduction To Accounting: Earning BjectivesDocument22 pagesIntroduction To Accounting: Earning Bjectiveslalu morwalNo ratings yet

- Pa 2320-3 PDFDocument4 pagesPa 2320-3 PDFaian joseph100% (1)

- Bba 104Document418 pagesBba 104Alma Landero100% (1)

- Timing Is Everything With ASC 606: The New Revenue Recognition StandardDocument4 pagesTiming Is Everything With ASC 606: The New Revenue Recognition StandardJesse NgaliNo ratings yet

- Are You Ready For The New Revenue Recognition Standard?: Liz Farr, CpaDocument3 pagesAre You Ready For The New Revenue Recognition Standard?: Liz Farr, CpaJesse NgaliNo ratings yet

- Practice Exam Chapters 1-4 Solutions: Problem IDocument6 pagesPractice Exam Chapters 1-4 Solutions: Problem IJesse NgaliNo ratings yet

- Exam 1 5Document6 pagesExam 1 5Alex Schuldiner0% (1)

- Lawquiz PDFDocument6 pagesLawquiz PDFAliya NaseemNo ratings yet

- Exam 1 8Document9 pagesExam 1 8Kenneth DelacruzNo ratings yet

- Practice Exam Chapters 1-5 Adjusting EntriesDocument7 pagesPractice Exam Chapters 1-5 Adjusting Entriesswoop9No ratings yet

- AFF01 Satellite Tutorial Week 10Document15 pagesAFF01 Satellite Tutorial Week 10Jesse NgaliNo ratings yet

- The Government Inspector NotesDocument23 pagesThe Government Inspector Notesmichaelchuc123No ratings yet

- 22 JFin Crime 79Document26 pages22 JFin Crime 79Ankitha ReddyNo ratings yet

- Cybercrimes ThesisDocument5 pagesCybercrimes ThesisacademicsandpapersNo ratings yet

- Rfli FinalsDocument24 pagesRfli FinalsKatrina PaquizNo ratings yet

- Food Fraud Mitigation Program (Ebook - Eng)Document37 pagesFood Fraud Mitigation Program (Ebook - Eng)Ramesh GarimellaNo ratings yet

- Forensic Accounting FGFOA Nov06Document44 pagesForensic Accounting FGFOA Nov06saurabh_kumbhareNo ratings yet

- Introduction Lie Detection TechniqueDocument18 pagesIntroduction Lie Detection TechniqueRaven SantosNo ratings yet

- Desmoparan V People (Crim) PDFDocument7 pagesDesmoparan V People (Crim) PDFNingkolingNo ratings yet

- Utmost Good FaithDocument10 pagesUtmost Good FaithAditya PrakashNo ratings yet

- Forensic and Investigative Accounting Module 1Document18 pagesForensic and Investigative Accounting Module 1Jhelson SoaresNo ratings yet

- Shrek's magical contract analyzedDocument2 pagesShrek's magical contract analyzedLeanne Quinto100% (1)

- Integrity: Example: Client AcceptanceDocument2 pagesIntegrity: Example: Client AcceptanceMary Rose JuanNo ratings yet

- Forensic Accounting and Fraud Control in Nigeria: A Critical ReviewDocument10 pagesForensic Accounting and Fraud Control in Nigeria: A Critical ReviewKunleNo ratings yet

- The Consolidated Case Of: GR No. 183464 30 June 2014Document13 pagesThe Consolidated Case Of: GR No. 183464 30 June 2014Ryan CalanoNo ratings yet

- PHILIPPINE DEPOSIT INSURANCE CORPORATION v. MANU GIDWANIDocument28 pagesPHILIPPINE DEPOSIT INSURANCE CORPORATION v. MANU GIDWANIFaustina del RosarioNo ratings yet

- Wa0058.Document4 pagesWa0058.Erwin PariNo ratings yet

- Raport OLAFDocument60 pagesRaport OLAFliviugstanNo ratings yet

- G.R. No. 215132Document12 pagesG.R. No. 215132Rap VillarinNo ratings yet

- (Soriano v. BSP)Document2 pages(Soriano v. BSP)Patrick ManaloNo ratings yet

- Detecting Fraud in Financial Statements (DFSDocument3 pagesDetecting Fraud in Financial Statements (DFSPaula Mae DacanayNo ratings yet

- ReviewDocument4 pagesReviewMilfsHookup100% (3)

- Avoiding Academic DishonestyDocument31 pagesAvoiding Academic DishonestyJustt RoderichNo ratings yet

- Cyber Crimes in Banking SectorDocument23 pagesCyber Crimes in Banking SectorAUNNESHA DEYNo ratings yet

- Online ScammingDocument25 pagesOnline ScammingERICKSON JUAN50% (2)

- BUSINESS LAW KEY TERMSDocument25 pagesBUSINESS LAW KEY TERMSMeister PrabaNo ratings yet

- Crim Law 2Document161 pagesCrim Law 2Robert Kane Malcampo ReyesNo ratings yet

- Effect of Whistle Blowing On Fraud Prevention and Detection in Nigeria Public SectorDocument14 pagesEffect of Whistle Blowing On Fraud Prevention and Detection in Nigeria Public SectorEfosaNo ratings yet

- Affidavit of Authenticity of DocumentDocument1 pageAffidavit of Authenticity of DocumentCybill Astrids Rey RectoNo ratings yet

- Respondent After 12 PMDocument28 pagesRespondent After 12 PMvinay sharmaNo ratings yet

- Scam in Banking Sectors, IndiaDocument3 pagesScam in Banking Sectors, IndiaRon NNo ratings yet