You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- PayslipDocument1 pagePayslipmallikarjunamargam100% (3)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Accounting Procedures and ConceptsDocument36 pagesAccounting Procedures and ConceptsIlwynFreiresGascal0% (1)

- Financial ManagementDocument97 pagesFinancial ManagementGuruKPO100% (17)

- Lecture On Taxation Law - 2020Document143 pagesLecture On Taxation Law - 2020Jay RamNo ratings yet

- SocGen End of The Super Cycle 7-20-2011Document5 pagesSocGen End of The Super Cycle 7-20-2011Red911TNo ratings yet

- Obli 15Document15 pagesObli 15Shane JesuitasNo ratings yet

- 7-1 Scale and Scope: Short Answer QuestionsDocument2 pages7-1 Scale and Scope: Short Answer QuestionsShane Jesuitas100% (1)

- Obli 13Document2 pagesObli 13Shane JesuitasNo ratings yet

- Short Answer Questions: 12-1 Parking Lot OptimizationDocument3 pagesShort Answer Questions: 12-1 Parking Lot OptimizationShane JesuitasNo ratings yet

- Multiple Choice QuestionsDocument2 pagesMultiple Choice QuestionsShane JesuitasNo ratings yet

- Noun Phrases As Noun Phrase Modifiers: ClausesDocument1 pageNoun Phrases As Noun Phrase Modifiers: ClausesShane JesuitasNo ratings yet

- Acctg 121 MidtermsDocument8 pagesAcctg 121 MidtermsShane JesuitasNo ratings yet

- Accounting System-Special Journals Accounting System - Special JournalsDocument27 pagesAccounting System-Special Journals Accounting System - Special JournalsShane Jesuitas100% (1)

- Bank Case StudiesDocument6 pagesBank Case StudiesRazib Ghani50% (4)

- Almario Bsa2d At4 Fin2Document4 pagesAlmario Bsa2d At4 Fin2Tracy CamilleNo ratings yet

- Role of Financial Derivatives in Financial Risk ManagementDocument16 pagesRole of Financial Derivatives in Financial Risk ManagementTYBMS-A 3001 Ansh AgarwalNo ratings yet

- Methods of Project Finance White Paper White Paper: Why Is It Important To Understand Project Finance?Document18 pagesMethods of Project Finance White Paper White Paper: Why Is It Important To Understand Project Finance?nfkrecNo ratings yet

- Fraud Prevention For Commercial Real Estate Valuation (PDFDrive)Document128 pagesFraud Prevention For Commercial Real Estate Valuation (PDFDrive)consmoNo ratings yet

- BA (1st) May2020Document3 pagesBA (1st) May2020Manjot KaurNo ratings yet

- Property Tax: OwnerDocument2 pagesProperty Tax: OwnerAnkit A DesaiNo ratings yet

- Profit & Loss: Velka Engineering LTDDocument10 pagesProfit & Loss: Velka Engineering LTDparthsavaniNo ratings yet

- Annexure Car IvDocument3 pagesAnnexure Car IvRahul kumarNo ratings yet

- MCQs - Objective Type - Poonam GandhiDocument55 pagesMCQs - Objective Type - Poonam GandhifarhaanNo ratings yet

- BGS Micro NotesDocument1 pageBGS Micro NotesAvinash JhaNo ratings yet

- Barangay Budget Preparation andDocument13 pagesBarangay Budget Preparation andMimi OlshopeNo ratings yet

- The Big Mac TheoryDocument4 pagesThe Big Mac TheoryGemini_0804No ratings yet

- Outline On Articles of IncorporationDocument4 pagesOutline On Articles of IncorporationkaiaceegeesNo ratings yet

- MCQ Paper 17Document34 pagesMCQ Paper 17ABC 123No ratings yet

- CE Interim ReportingDocument2 pagesCE Interim ReportingalyssaNo ratings yet

- ABL FMR JULY 23 Shariah CompliantDocument13 pagesABL FMR JULY 23 Shariah CompliantAniqa AsgharNo ratings yet

- Sunlight Equipment Manufacturers Sem Makes Barbecue Equipment The Company Has PDFDocument2 pagesSunlight Equipment Manufacturers Sem Makes Barbecue Equipment The Company Has PDFFreelance WorkerNo ratings yet

- Trading Bitcoin Master-Class 1Document15 pagesTrading Bitcoin Master-Class 1Sean SmythNo ratings yet

- Dividend Policy: FM, PGDM 2019-21Document27 pagesDividend Policy: FM, PGDM 2019-21chandel08No ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2011 Question Paper For The Guidance of TeachersDocument6 pages9706 Accounting: MARK SCHEME For The October/November 2011 Question Paper For The Guidance of TeachersProto Proffesor TshumaNo ratings yet

- Solution Question 2 Quiz 2005 PDFDocument3 pagesSolution Question 2 Quiz 2005 PDFsaurabhsaurs100% (1)

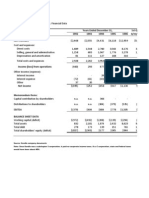

- Exhibit 1 Kendle International Inc. Financial Data Years Ended December 31Document12 pagesExhibit 1 Kendle International Inc. Financial Data Years Ended December 31Kito Minying ChenNo ratings yet

- AA Activity HistoryDocument4 pagesAA Activity HistoryMrCHANTHA100% (1)

- IC38 Concise-1Document30 pagesIC38 Concise-1Swanand VlogsNo ratings yet