You might also like

- Original PDF Financial Management Core Concepts 4th Edition by Raymond Brooks PDFDocument42 pagesOriginal PDF Financial Management Core Concepts 4th Edition by Raymond Brooks PDFmathew.robertson818100% (35)

- More Gerund Infinitive PracticeDocument1 pageMore Gerund Infinitive PracticeKatieSalsburyNo ratings yet

- Soal Dan Jawaban Audit IIDocument22 pagesSoal Dan Jawaban Audit IIsantaulinasitorusNo ratings yet

- 01 BIWS Accounting Quick Reference PDFDocument2 pages01 BIWS Accounting Quick Reference PDFcarminatNo ratings yet

- Assignment 3 Apple BlossomDocument21 pagesAssignment 3 Apple BlossomMonica NainggolanNo ratings yet

- 2022FORM - GIS-Non-Stock 2023Document6 pages2022FORM - GIS-Non-Stock 2023TEODORICO PINLAC0% (1)

- CH 3 - Intro To Consolidated Fin StatDocument16 pagesCH 3 - Intro To Consolidated Fin StatMutia WardaniNo ratings yet

- Basic Accounting Table of ContentsDocument2 pagesBasic Accounting Table of ContentsrynnaNo ratings yet

- Bodie Industrial SupplyDocument14 pagesBodie Industrial SupplyHectorZaratePomajulca100% (2)

- Comprehensive Case-Campbell SoupDocument9 pagesComprehensive Case-Campbell SoupIlham Muhammad AkbarNo ratings yet

- Accounting Theory Godfrey - 5Document27 pagesAccounting Theory Godfrey - 5Daniel JosephNo ratings yet

- Target Costing PDFDocument44 pagesTarget Costing PDFAnonymous dPkadxxNo ratings yet

- Measurement Theory Sesi #5 Dr. Zaroni: Godfrey Hodgson Holmes TarcaDocument27 pagesMeasurement Theory Sesi #5 Dr. Zaroni: Godfrey Hodgson Holmes TarcaFELIX PANDIKANo ratings yet

- Sfac No.2 Fasb PDFDocument38 pagesSfac No.2 Fasb PDFayuputrityaNo ratings yet

- IPSAS Explained: A Summary of International Public Sector Accounting StandardsFrom EverandIPSAS Explained: A Summary of International Public Sector Accounting StandardsNo ratings yet

- Solution Manual For Cfin 6th by BesleyDocument8 pagesSolution Manual For Cfin 6th by BesleyHeatherBowmaniotfNo ratings yet

- CLEO - Annual Report - 2018 Dicetak Mulai Halaman 115-128Document196 pagesCLEO - Annual Report - 2018 Dicetak Mulai Halaman 115-128Dian AnjaniNo ratings yet

- Art 3 The Effect of Financial Ratios On Returns From Initial Public Offerings: An Application of Principal Components Analysis Min-Tsung ChengDocument9 pagesArt 3 The Effect of Financial Ratios On Returns From Initial Public Offerings: An Application of Principal Components Analysis Min-Tsung ChengArta Marisa ListyadeviNo ratings yet

- Case 6-1 (ANDI DIAN AULIA-46117022)Document5 pagesCase 6-1 (ANDI DIAN AULIA-46117022)dianNo ratings yet

- Akuntansi Keuangan Lanjutan - Chap 007Document39 pagesAkuntansi Keuangan Lanjutan - Chap 007Gugat jelang romadhonNo ratings yet

- MAGP Annual Report 2017Document86 pagesMAGP Annual Report 2017cindytantrianiNo ratings yet

- Kelompok 10 - Tugas P3 - Account ReceivableDocument16 pagesKelompok 10 - Tugas P3 - Account ReceivableRayhan MametNo ratings yet

- Chapter 2 - Understanding StrategiesDocument31 pagesChapter 2 - Understanding StrategiesSarah Laras WitaNo ratings yet

- Acg5205 Solutions Ch.16 - Christensen 12eDocument10 pagesAcg5205 Solutions Ch.16 - Christensen 12eRyan NguyenNo ratings yet

- Reports On Audited Financial Statements: CompanyDocument37 pagesReports On Audited Financial Statements: Companyhassan nassereddineNo ratings yet

- Accounting Theory (AcT) (Teori Akuntansi (TA) ) - Chapter 9 (Godfrey) - PPT-revenue (14 A)Document24 pagesAccounting Theory (AcT) (Teori Akuntansi (TA) ) - Chapter 9 (Godfrey) - PPT-revenue (14 A)Pindi YulinarNo ratings yet

- Auditing Ii Resume CH 17 Audit Sampling For Tests of Details of Balances (Contoh Audit Untuk Menguji Detail Dari Saldo)Document22 pagesAuditing Ii Resume CH 17 Audit Sampling For Tests of Details of Balances (Contoh Audit Untuk Menguji Detail Dari Saldo)juli kyoyaNo ratings yet

- Arens14e ch07 PPTDocument43 pagesArens14e ch07 PPTNindya Harum SolichaNo ratings yet

- Rangkuman TaDocument19 pagesRangkuman Tamutia rasyaNo ratings yet

- 3Q - 2016 - CPGT - Citra Maharlika Nusantara Corpora TBK PDFDocument107 pages3Q - 2016 - CPGT - Citra Maharlika Nusantara Corpora TBK PDFYudhi MahendraNo ratings yet

- Boynton SM Ch.08Document10 pagesBoynton SM Ch.08Eza RNo ratings yet

- RESUME SAP Financial Unit 3Document5 pagesRESUME SAP Financial Unit 3Novita WardaniNo ratings yet

- SOAL CASE 14 - 33 Dan CASE 16-35Document4 pagesSOAL CASE 14 - 33 Dan CASE 16-35Rictu SempakNo ratings yet

- Teori AkunDocument12 pagesTeori AkunErditama GeryNo ratings yet

- Resume Asi UasDocument24 pagesResume Asi UasanggiyusufNo ratings yet

- Solved Jerry Goff President of Harmony Electronics Was Concerned AbouDocument2 pagesSolved Jerry Goff President of Harmony Electronics Was Concerned AbouDoreenNo ratings yet

- Review Questions: Solutions Manual To Accompany Dunn, Enterprise Information Systems: A Pattern Based Approach, 3eDocument17 pagesReview Questions: Solutions Manual To Accompany Dunn, Enterprise Information Systems: A Pattern Based Approach, 3eOpirisky ApriliantyNo ratings yet

- Kelompok 6 ALK - Tugas Case 11-3Document6 pagesKelompok 6 ALK - Tugas Case 11-3Jaisyur Rahman SetyadharmaatmajaNo ratings yet

- BAB 4 Analyzing Investing Activities 220916 PDFDocument15 pagesBAB 4 Analyzing Investing Activities 220916 PDFHaniedar NadifaNo ratings yet

- National Tractor and Equipment - Case Study Solution - Performance MeasurementDocument4 pagesNational Tractor and Equipment - Case Study Solution - Performance MeasurementPiotr BartenbachNo ratings yet

- Akuntansi CabangDocument24 pagesAkuntansi Cabangdina sabilaNo ratings yet

- Chapter 15: Partnerships - Formation, Operations, and Changes in Ownership InterestsDocument42 pagesChapter 15: Partnerships - Formation, Operations, and Changes in Ownership InterestsKoko D'DemonsongNo ratings yet

- ch06 EDITDocument46 pagesch06 EDITAgoeng Susanto BrajewoNo ratings yet

- HDTX - Audit Report 2018 PDFDocument85 pagesHDTX - Audit Report 2018 PDFFajar PambudiNo ratings yet

- 18-32 (Objectives 18-2, 18-3, 18-4, 18-6)Document8 pages18-32 (Objectives 18-2, 18-3, 18-4, 18-6)image4all100% (1)

- Jawaban Chapter 19Document21 pagesJawaban Chapter 19Stephanie Felicia TiffanyNo ratings yet

- Accounting Theory Case 7.2Document3 pagesAccounting Theory Case 7.2Lutfiana Hermawati100% (1)

- Anthony & Govindarajan - CH 11Document3 pagesAnthony & Govindarajan - CH 11Astha Agarwal100% (1)

- Case 6.2Document5 pagesCase 6.2Azhar KanedyNo ratings yet

- Tugas Kelompok Auditing II 14-33Document5 pagesTugas Kelompok Auditing II 14-33Lela MilasantiNo ratings yet

- Prak. ALK Latihan Cash Flow - Assyva Naila Agustine - 023002001093Document2 pagesPrak. ALK Latihan Cash Flow - Assyva Naila Agustine - 023002001093nanaNo ratings yet

- 4 Jod OrderDocument32 pages4 Jod OrderSetia NurulNo ratings yet

- ch12 - F MDocument8 pagesch12 - F MAhmed Osama ElgebalyNo ratings yet

- FASB Accounting Standards Codification Topic 605Document2 pagesFASB Accounting Standards Codification Topic 605justwonder2No ratings yet

- Nama: Yandra Febriyanti No BP: 1810531018 P2-23 1) Equity Method Entroes On Peanut Company's BooksDocument7 pagesNama: Yandra Febriyanti No BP: 1810531018 P2-23 1) Equity Method Entroes On Peanut Company's BooksYandra FebriyantiNo ratings yet

- Pengaruh Persepsi Dan Motivasi Terhadap Minat Mahasiswa Jurusan Akuntasi Fakultas Ekonomi Dan Bisnis Universitas Brawijaya BerkDocument15 pagesPengaruh Persepsi Dan Motivasi Terhadap Minat Mahasiswa Jurusan Akuntasi Fakultas Ekonomi Dan Bisnis Universitas Brawijaya BerkRecca Damayanti0% (1)

- CrockerDocument6 pagesCrockersg31No ratings yet

- Problems P 15-1 Apply Threshold Tests: Net Income Tax RateDocument2 pagesProblems P 15-1 Apply Threshold Tests: Net Income Tax Rateardi yansyahNo ratings yet

- Assignment 10 Apple BlossomDocument16 pagesAssignment 10 Apple BlossomMonica NainggolanNo ratings yet

- Problems Problem 10.1: © John Wiley and Sons Australia, LTD 2010 10.21Document5 pagesProblems Problem 10.1: © John Wiley and Sons Australia, LTD 2010 10.21alfaressNo ratings yet

- Beams10e - Ch02 Stock Investments-Investor Accounting and ReportingDocument37 pagesBeams10e - Ch02 Stock Investments-Investor Accounting and ReportingNadiaAmaliaNo ratings yet

- Partnership OperationDocument37 pagesPartnership OperationMuchamad RifaiNo ratings yet

- Case Study 1 v.3 PDFDocument21 pagesCase Study 1 v.3 PDFAce DesabilleNo ratings yet

- Chapter 4 Consolidation HWDocument4 pagesChapter 4 Consolidation HWKhanh NguyenNo ratings yet

- The Size of Government: Measurement, Methodology and Official StatisticsFrom EverandThe Size of Government: Measurement, Methodology and Official StatisticsNo ratings yet

- TBChap 009Document36 pagesTBChap 009varun cywNo ratings yet

- Annuity MethodDocument2 pagesAnnuity MethodKaran GNo ratings yet

- Chapter 2 Capital Budgeting Principles and Techniques HOMEWORKDocument6 pagesChapter 2 Capital Budgeting Principles and Techniques HOMEWORKjimmy_chou13140% (1)

- Idx Fact Book 2008 (Upload)Document199 pagesIdx Fact Book 2008 (Upload)dwi_purnomo_7No ratings yet

- Summer Internship Project ReportDocument42 pagesSummer Internship Project Reportadishitole106No ratings yet

- Meaning and Types of SharesDocument4 pagesMeaning and Types of SharesFRANKMARTINAJNo ratings yet

- CF 2Document114 pagesCF 2Vishnu VardhanNo ratings yet

- Full Download Intermediate Accounting 2nd Edition Gordon Solutions ManualDocument35 pagesFull Download Intermediate Accounting 2nd Edition Gordon Solutions Manualashero2eford100% (49)

- 74690bos60485 Inter p1 cp4 U3Document28 pages74690bos60485 Inter p1 cp4 U3Ankita DebtaNo ratings yet

- Mark Scheme: November 2018Document14 pagesMark Scheme: November 2018BethanyNo ratings yet

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument85 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeSameen ArifNo ratings yet

- Chapter 13 Corporations and Stockholders' EquityDocument23 pagesChapter 13 Corporations and Stockholders' EquityKiri SorianoNo ratings yet

- Far-Single Entry PDFDocument7 pagesFar-Single Entry PDFJanica June FiscalNo ratings yet

- Illustrative Condensed Interim Financial StatemenstDocument44 pagesIllustrative Condensed Interim Financial Statemenstalina6523305No ratings yet

- Course Name: Master of Business Administration: Computation of Weighted Average Cost of CapitalDocument8 pagesCourse Name: Master of Business Administration: Computation of Weighted Average Cost of CapitalshriyaNo ratings yet

- IAS 16 - Property, Plant and Equipment: Date Development CommentsDocument7 pagesIAS 16 - Property, Plant and Equipment: Date Development CommentsPhebieon MukwenhaNo ratings yet

- Refer To The Information Provided in p10 2a p10 2a Donnie Hilfiger Has TwoDocument1 pageRefer To The Information Provided in p10 2a p10 2a Donnie Hilfiger Has TwoBube KachevskaNo ratings yet

- Mahindra Towers, Dr. G. M. Bhosale Marg, Worli, Mumbai 400 018 India Tel: +91 22 24901441 Fax: +91 22 24975081Document22 pagesMahindra Towers, Dr. G. M. Bhosale Marg, Worli, Mumbai 400 018 India Tel: +91 22 24901441 Fax: +91 22 24975081Mannu SinghNo ratings yet

- Case 1:: Industrial Industrial Capitalist CapitalistDocument3 pagesCase 1:: Industrial Industrial Capitalist CapitalistAnonnNo ratings yet

- Perusahaan DagangDocument7 pagesPerusahaan DagangWidad NadiaNo ratings yet

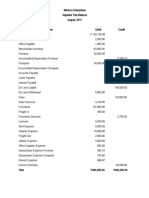

- Adjusted Trial BalanceDocument1 pageAdjusted Trial BalanceANDREA OLIVASNo ratings yet

- PutOrder DD214Document1 pagePutOrder DD214ajgtrustNo ratings yet

- F6 PIT AnswersDocument18 pagesF6 PIT AnswersHuỳnh TrungNo ratings yet

- Particulars Debit Credit: Date Bill No VCH Type VCH No. Balance 13/02/2022 8 - SIB Journal JV-22/02/002Document1 pageParticulars Debit Credit: Date Bill No VCH Type VCH No. Balance 13/02/2022 8 - SIB Journal JV-22/02/002Zazabor er MonNo ratings yet