You might also like

- Bloomberg Cheat SheetDocument11 pagesBloomberg Cheat SheetKhalilBenlahccen100% (2)

- An Overview of Modeling Credit PortfoliosDocument23 pagesAn Overview of Modeling Credit PortfoliosKhaledNo ratings yet

- Black ScholesDocument41 pagesBlack ScholesImran MobinNo ratings yet

- Value-At-risk Based Portfolio Theory - Optimum Startegies and AllocationDocument35 pagesValue-At-risk Based Portfolio Theory - Optimum Startegies and AllocationDebNo ratings yet

- 5.4.3 Term Structure Model and Interest Rate Trees: Example 5.12 BDT Tree CalibrationDocument5 pages5.4.3 Term Structure Model and Interest Rate Trees: Example 5.12 BDT Tree CalibrationmoritemNo ratings yet

- Donchian Channel BreakoutDocument11 pagesDonchian Channel BreakoutShahzad Dalal100% (2)

- Credit DerivativesDocument37 pagesCredit DerivativesshehzadshroffNo ratings yet

- Asset Liability ManagementDocument18 pagesAsset Liability Managementmahesh19689No ratings yet

- Value at RiskDocument11 pagesValue at RiskRashmiroja SahuNo ratings yet

- Calculating and Applying Var: Learning ObjectivesDocument12 pagesCalculating and Applying Var: Learning Objectivesthao dinhNo ratings yet

- VAR Romain BerryDocument18 pagesVAR Romain BerryAbhishekNo ratings yet

- Chapter 7 PortfolioTheoryDocument42 pagesChapter 7 PortfolioTheoryAanchalNo ratings yet

- Binomial TreeDocument22 pagesBinomial TreeXavier Francis S. LutaloNo ratings yet

- Financial Risk Management Assignment: Submitted By: Name: Tanveer Ahmad Registered No: 0920228Document13 pagesFinancial Risk Management Assignment: Submitted By: Name: Tanveer Ahmad Registered No: 0920228Tanveer AhmadNo ratings yet

- Risk Management in Banking CompaniesDocument2 pagesRisk Management in Banking CompaniesPrashanth NaraenNo ratings yet

- Risk and Return - Lu-6Document54 pagesRisk and Return - Lu-6Mega capitalmarket100% (1)

- Presentation 04 - Risk and Return 2012.11.15Document54 pagesPresentation 04 - Risk and Return 2012.11.15SantaAgataNo ratings yet

- CFA Society Boston Level III 2021 Practice Exam Answer KeyDocument37 pagesCFA Society Boston Level III 2021 Practice Exam Answer KeySteph ONo ratings yet

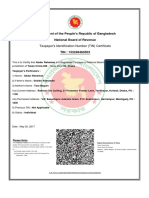

- NBR Tin Certificate 164138662022Document1 pageNBR Tin Certificate 164138662022Md. Jasim UddinNo ratings yet

- Capital Asset Pricing Theory and Arbitrage Pricing TheoryDocument19 pagesCapital Asset Pricing Theory and Arbitrage Pricing TheoryMohammed ShafiNo ratings yet

- Index: Acknowledgement Executive Summary Chapter-1Document85 pagesIndex: Acknowledgement Executive Summary Chapter-1Kiran KatyalNo ratings yet

- Asset Liability ManagementDocument71 pagesAsset Liability ManagementRohit SharmaNo ratings yet

- Var, CaR, CAR, Basel 1 and 2Document7 pagesVar, CaR, CAR, Basel 1 and 2ChartSniperNo ratings yet

- 17 Use of The Var Method For Measuring Market Risks and Calculating Capital AdequacyDocument5 pages17 Use of The Var Method For Measuring Market Risks and Calculating Capital AdequacyYounus AkhoonNo ratings yet

- An Introduction To Value at Risk (VAR)Document6 pagesAn Introduction To Value at Risk (VAR)AkshatNo ratings yet

- Chapter 08 Risk and Rates of ReturnDocument48 pagesChapter 08 Risk and Rates of ReturnNaida's StuffNo ratings yet

- Duration PDFDocument8 pagesDuration PDFMohammad Khaled Saifullah CdcsNo ratings yet

- Session 5 - Valuing Bonds and StocksDocument51 pagesSession 5 - Valuing Bonds and Stocksmaud balesNo ratings yet

- Stress Testing of Banks An IntroductionDocument14 pagesStress Testing of Banks An IntroductionRegards MDNo ratings yet

- Dynamic ALMDocument5 pagesDynamic ALMleonodisNo ratings yet

- Fixed Income Securities: Bond Basics: CRICOS Code 00025BDocument43 pagesFixed Income Securities: Bond Basics: CRICOS Code 00025BNurhastuty WardhanyNo ratings yet

- Portfolio Markowitz ModelDocument43 pagesPortfolio Markowitz Modelbcips100% (1)

- Forecasting Default With The KMV-Merton ModelDocument35 pagesForecasting Default With The KMV-Merton ModelEdgardo Garcia MartinezNo ratings yet

- Credit Risk Mgmt. at ICICIDocument60 pagesCredit Risk Mgmt. at ICICIRikesh Daliya100% (1)

- Financial FormulasDocument2 pagesFinancial FormulasCoreyNo ratings yet

- Value at RiskDocument4 pagesValue at RiskShubham PariharNo ratings yet

- Credit Risk Modelling - A PrimerDocument42 pagesCredit Risk Modelling - A PrimersatishdwnldNo ratings yet

- Caiib Material For Studying and Refreshing Asset Liability Management ofDocument62 pagesCaiib Material For Studying and Refreshing Asset Liability Management ofsupercoolvimiNo ratings yet

- VarDocument4 pagesVarmounabsNo ratings yet

- 3 - 1-Asset Liability Management PDFDocument26 pages3 - 1-Asset Liability Management PDFjayaNo ratings yet

- Introduction To Value-at-Risk PDFDocument10 pagesIntroduction To Value-at-Risk PDFHasan SadozyeNo ratings yet

- Quantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskFrom EverandQuantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskRating: 3.5 out of 5 stars3.5/5 (1)

- CH 5 MARKET RISK - VaRDocument29 pagesCH 5 MARKET RISK - VaRAisyah Vira AmandaNo ratings yet

- Chapter 10 - MarketDocument13 pagesChapter 10 - MarketTammie Henderson100% (1)

- Policy CycleDocument3 pagesPolicy CycleMd. Jasim Uddin100% (1)

- Presentation On Value at RiskDocument22 pagesPresentation On Value at RiskRomaMakhijaNo ratings yet

- Bond Yields and PricesDocument11 pagesBond Yields and PricesLeo Adam-lallaniNo ratings yet

- Interest Rates and Security ValuationDocument60 pagesInterest Rates and Security Valuationlinda zyongweNo ratings yet

- Ifrs 9 Ecl Template General ApproachDocument2 pagesIfrs 9 Ecl Template General ApproachTousief NaqviNo ratings yet

- Quantitative Risk Management: A Practical Guide to Financial RiskFrom EverandQuantitative Risk Management: A Practical Guide to Financial RiskNo ratings yet

- Credit Risk: Pricing, Measurement, and ManagementFrom EverandCredit Risk: Pricing, Measurement, and ManagementRating: 1 out of 5 stars1/5 (2)

- FRM Project On VaRDocument12 pagesFRM Project On VaRboldfaceaxisNo ratings yet

- Session 5 - Cost of CapitalDocument49 pagesSession 5 - Cost of CapitalMuhammad HanafiNo ratings yet

- Fabozzi BMAS8 CH03 IM GE VersionDocument29 pagesFabozzi BMAS8 CH03 IM GE VersionsophiaNo ratings yet

- MR Economics SlidesDocument170 pagesMR Economics SlidesMahmud ShetuNo ratings yet

- Model Building ApproachDocument7 pagesModel Building ApproachJessuel Larn-epsNo ratings yet

- Economic Capital in Banking v03Document10 pagesEconomic Capital in Banking v03AndreKochNo ratings yet

- Credit Risk Analysis Applying Logistic Regression, Neural Networks and Genetic Algorithms ModelsDocument12 pagesCredit Risk Analysis Applying Logistic Regression, Neural Networks and Genetic Algorithms ModelsIJAERS JOURNALNo ratings yet

- III.B.6 Credit Risk Capital CalculationDocument28 pagesIII.B.6 Credit Risk Capital CalculationvladimirpopovicNo ratings yet

- Scheinkman Common Factors Affecting Bond ReturnsDocument8 pagesScheinkman Common Factors Affecting Bond ReturnsjamaiccsNo ratings yet

- Risk Management Using Derivative ProductsDocument48 pagesRisk Management Using Derivative ProductschandranilNo ratings yet

- Basel 3 ImplementationDocument20 pagesBasel 3 Implementationsh_chandraNo ratings yet

- Interest Rate & Currency SwapsDocument35 pagesInterest Rate & Currency SwapsiftekharvhaiNo ratings yet

- Portfolio Theory PDFDocument44 pagesPortfolio Theory PDFDinhkhanh NguyenNo ratings yet

- Sonargaon University (Su)Document1 pageSonargaon University (Su)Md. Jasim Uddin100% (1)

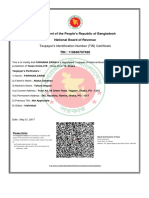

- NBR Tin Certificate 541484216851Document1 pageNBR Tin Certificate 541484216851Md. Jasim UddinNo ratings yet

- JSC Sugession & Modeltes-2015Document11 pagesJSC Sugession & Modeltes-2015Md. Jasim UddinNo ratings yet

- Schedule of 14th BJS Preliminary Examination 2021 1Document1 pageSchedule of 14th BJS Preliminary Examination 2021 1Md. Jasim UddinNo ratings yet

- NBR Tin Certificate 334030183882Document1 pageNBR Tin Certificate 334030183882Md. Jasim Uddin100% (1)

- Internship Report: A Study On "Automated Clearing House of Jamuna Bank LTD."Document6 pagesInternship Report: A Study On "Automated Clearing House of Jamuna Bank LTD."Md. Jasim Uddin100% (1)

- Assessment of English Language Skills at The Secondary Level in BangladeshDocument7 pagesAssessment of English Language Skills at The Secondary Level in BangladeshMd. Jasim UddinNo ratings yet

- NBR Tin Certificate 133248460503Document1 pageNBR Tin Certificate 133248460503Md. Jasim UddinNo ratings yet

- NBR Tin Certificate 119846707490Document1 pageNBR Tin Certificate 119846707490Md. Jasim UddinNo ratings yet

- Auvkhy Lvev Ii Afverwbz Ivm: M WpcîDocument50 pagesAuvkhy Lvev Ii Afverwbz Ivm: M WpcîMd. Jasim UddinNo ratings yet

- Letter of Transmittal 01Document10 pagesLetter of Transmittal 01Md. Jasim UddinNo ratings yet

- 3rd ChapterDocument17 pages3rd ChapterMd. Jasim UddinNo ratings yet

- Tender Document Procurement: FortheDocument19 pagesTender Document Procurement: FortheMd. Jasim UddinNo ratings yet

- 2013 GarmentbangladeshDocument115 pages2013 GarmentbangladeshMd. Jasim UddinNo ratings yet

- SL NO. Name Address Mobile No. Product Name QTY Source PriceDocument12 pagesSL NO. Name Address Mobile No. Product Name QTY Source PriceMd. Jasim UddinNo ratings yet

- BDT MillionDocument4 pagesBDT MillionMd. Jasim UddinNo ratings yet

- GMVM© Mygb G Uvicövbr: Mwbuvix KV Ri 'IDocument2 pagesGMVM© Mygb G Uvicövbr: Mwbuvix KV Ri 'IMd. Jasim UddinNo ratings yet

- Sumon EnterpriseDocument2 pagesSumon EnterpriseMd. Jasim UddinNo ratings yet

- Blue & Violet Shop Memo - Edit - 01Document1 pageBlue & Violet Shop Memo - Edit - 01Md. Jasim UddinNo ratings yet

- Portfolio Optimization: Stephen Boyd EE103 Stanford UniversityDocument34 pagesPortfolio Optimization: Stephen Boyd EE103 Stanford UniversitywoelfertNo ratings yet

- A Study On The Analysis of Financial Performance With Special Reference To Ramco Cement LTDDocument8 pagesA Study On The Analysis of Financial Performance With Special Reference To Ramco Cement LTDTJPRC PublicationsNo ratings yet

- The Effect of Income and Earnings Management On Firm Value - Empirical Evidence From Indonesia PDFDocument8 pagesThe Effect of Income and Earnings Management On Firm Value - Empirical Evidence From Indonesia PDFHafiz MamailaoNo ratings yet

- Bootcamp XDocument19 pagesBootcamp XVivek LasunaNo ratings yet

- Format For Preparing Cash Flow Statement-PBTDocument6 pagesFormat For Preparing Cash Flow Statement-PBTanurag_09No ratings yet

- Solution Manual For Financial Reporting and Analysis 13th Edition by GibsonDocument24 pagesSolution Manual For Financial Reporting and Analysis 13th Edition by GibsonRobertGonzalesyijx100% (35)

- Ranabir Sanyal: To, The Executive DirectorDocument13 pagesRanabir Sanyal: To, The Executive DirectorAbhilash KamtiNo ratings yet

- Accounting For Foreign Currency Transactions and TranslationDocument10 pagesAccounting For Foreign Currency Transactions and TranslationMark Gelo WinchesterNo ratings yet

- FM AssignmentDocument3 pagesFM Assignmentjeaner2008No ratings yet

- Types of MarketDocument6 pagesTypes of MarketCHINMAY AGRAWALNo ratings yet

- Lo1 - 4Document8 pagesLo1 - 4Panneer Selvam Usteevan RahulNo ratings yet

- Adani Ports and Special Economic Zone LTD.: Overall Industry Expectation of RatiosDocument10 pagesAdani Ports and Special Economic Zone LTD.: Overall Industry Expectation of RatiosChirag JainNo ratings yet

- Ratio Analysis of Square Pharmaceuticals LTDDocument4 pagesRatio Analysis of Square Pharmaceuticals LTDmd_waleedaNo ratings yet

- Marginal Costing PDFDocument16 pagesMarginal Costing PDFaditiNo ratings yet

- Contoh Soal AklanDocument8 pagesContoh Soal AklanVendola YolandaNo ratings yet

- ACC Group Assignment 1Document13 pagesACC Group Assignment 1aregahegn bisetNo ratings yet

- Bonds PayableDocument5 pagesBonds PayableAmbray Felyn Joy67% (3)

- Kavya's InternshipDocument11 pagesKavya's InternshipjijiNo ratings yet

- Capital Budgeting Practices by Corporates in India PPTDocument13 pagesCapital Budgeting Practices by Corporates in India PPTRVijaySai0% (1)

- Saroj ProposalDocument11 pagesSaroj ProposalSaroj SahNo ratings yet

- Ltcma Full ReportDocument150 pagesLtcma Full ReportJuan José Solis DelgadoNo ratings yet

- DERIVATIVESDocument30 pagesDERIVATIVESAyanda MabuthoNo ratings yet

- Annexure 9 Functional and Technical Requirement (UPDATED) Annexure 9.0 GeneralDocument47 pagesAnnexure 9 Functional and Technical Requirement (UPDATED) Annexure 9.0 GeneraldarshangoshNo ratings yet

- Accenture Reports Very Strong Fourth-Quarter and Full-Year Fiscal 2021 ResultsDocument14 pagesAccenture Reports Very Strong Fourth-Quarter and Full-Year Fiscal 2021 Resultssanath kumarNo ratings yet

- TPT550 - ExerciseDocument2 pagesTPT550 - ExerciseAzriNo ratings yet

- 01 Security Valuation - EquityDocument11 pages01 Security Valuation - Equitysoumyaduke700No ratings yet

- Greenlam Initiation JBWA 041022Document7 pagesGreenlam Initiation JBWA 041022PavanNo ratings yet