You might also like

- Taxation Cases (Digested)Document23 pagesTaxation Cases (Digested)Frizie Jane Sacasac Magbual100% (4)

- 10) Rizal Surety & Insurance Co. vs. Manila Railroad Company, 23 SCRA 205, No. L-24043 April 25, 1968Document4 pages10) Rizal Surety & Insurance Co. vs. Manila Railroad Company, 23 SCRA 205, No. L-24043 April 25, 1968Alexiss Mace JuradoNo ratings yet

- Sample Asset Purchase AgreementDocument58 pagesSample Asset Purchase AgreementJasmin Regis SyNo ratings yet

- Expected or Important Questions of International Law CSS by TahirDocument104 pagesExpected or Important Questions of International Law CSS by TahirTahir HabibNo ratings yet

- Statcon CasesDocument5 pagesStatcon CasesCzar Martinez100% (1)

- Definition of Income Tax Fisher - v. - TrinidadDocument15 pagesDefinition of Income Tax Fisher - v. - TrinidadnikkocandelariaNo ratings yet

- 4) Development Bank of The Philippines vs. Court of Appeals, 231 SCRA 370, G.R. No. 109937 March 21, 1994Document6 pages4) Development Bank of The Philippines vs. Court of Appeals, 231 SCRA 370, G.R. No. 109937 March 21, 1994Alexiss Mace JuradoNo ratings yet

- (C. Insurable Interest) Heirs of Loreto C. Maramag vs. Maramag, 588 SCRA 774, G.R. No. 181132 June 5, 2009Document9 pages(C. Insurable Interest) Heirs of Loreto C. Maramag vs. Maramag, 588 SCRA 774, G.R. No. 181132 June 5, 2009Alexiss Mace JuradoNo ratings yet

- Revised Rules and Regulations For The Issuance of Employment Permits To Foreign NationalsDocument19 pagesRevised Rules and Regulations For The Issuance of Employment Permits To Foreign NationalsBenmar DumdumNo ratings yet

- El Oriente Vs Posadas and CirDocument2 pagesEl Oriente Vs Posadas and CirRea RomeroNo ratings yet

- Manila Gas Corp Vs CIRDocument8 pagesManila Gas Corp Vs CIRlen_dy010487No ratings yet

- Digest 3rd Batch of Tax CasesDocument43 pagesDigest 3rd Batch of Tax CasesAnonymous rpZllEFb7No ratings yet

- RECEIPTDocument1 pageRECEIPTperguntas?No ratings yet

- Cash Management PresentationDocument28 pagesCash Management Presentationmailwalia100% (3)

- Federal Express Corporation vs. American Home Assurance CompanyDocument9 pagesFederal Express Corporation vs. American Home Assurance CompanyAlexiss Mace JuradoNo ratings yet

- Automatic Number Plate Recognition With Sms Reporting SystemDocument20 pagesAutomatic Number Plate Recognition With Sms Reporting SystemRithuNo ratings yet

- Manila Electric Co. v. Yatco, G.R. No. 45697, November 1, 1939Document4 pagesManila Electric Co. v. Yatco, G.R. No. 45697, November 1, 1939AkiNiHandiongNo ratings yet

- (C. Insurable Interest) Tai Tong Chuache & Co. vs. Insurance Commission, 158 SCRA 366, No. L-55397 February 29, 1988Document8 pages(C. Insurable Interest) Tai Tong Chuache & Co. vs. Insurance Commission, 158 SCRA 366, No. L-55397 February 29, 1988Alexiss Mace JuradoNo ratings yet

- 5) Zenith Insurance Corporation vs. Court of Appeals, 185 SCRA 398, G.R. No. 85296 May 14, 1990Document6 pages5) Zenith Insurance Corporation vs. Court of Appeals, 185 SCRA 398, G.R. No. 85296 May 14, 1990Alexiss Mace JuradoNo ratings yet

- Taxation Case DigestsDocument7 pagesTaxation Case DigestszzzNo ratings yet

- MGC Vs Collector SitusDocument5 pagesMGC Vs Collector SitusAira Mae P. LayloNo ratings yet

- Introduction To Administrative LawDocument38 pagesIntroduction To Administrative Lawrayosjl819100% (1)

- 8) Fireman's Fund Insurance Company vs. Jamila & Company, Inc., 70 SCRA 323, No. L-27427 April 7, 1976Document5 pages8) Fireman's Fund Insurance Company vs. Jamila & Company, Inc., 70 SCRA 323, No. L-27427 April 7, 1976Alexiss Mace JuradoNo ratings yet

- The Origami BookDocument45 pagesThe Origami Bookonur100% (1)

- 270 Philippine Reports Annotated: Enriquez vs. Sun Life Assurance Co. of CanadaDocument4 pages270 Philippine Reports Annotated: Enriquez vs. Sun Life Assurance Co. of CanadaAlexiss Mace JuradoNo ratings yet

- Case DigestDocument8 pagesCase DigestMadelle PinedaNo ratings yet

- El Oriente Fabrica v. PosadasDocument2 pagesEl Oriente Fabrica v. PosadasJohn Paul LordanNo ratings yet

- El Oriente v. Posadas, 56 Phil 147Document2 pagesEl Oriente v. Posadas, 56 Phil 147Homer SimpsonNo ratings yet

- Execution Petition in Ms Word Format DownloadDocument3 pagesExecution Petition in Ms Word Format DownloadHsk100% (1)

- Palileo vs. Cosio: 920 Philippine Reports AnnotatedDocument5 pagesPalileo vs. Cosio: 920 Philippine Reports AnnotatedAlexiss Mace JuradoNo ratings yet

- El Oriente Vs Posadas DigestDocument2 pagesEl Oriente Vs Posadas DigestMan2x Salomon100% (1)

- NetNumen U31 R22 (V12.15.10) Operation Guide (Common Operations) - V1.0Document412 pagesNetNumen U31 R22 (V12.15.10) Operation Guide (Common Operations) - V1.0kmad75% (8)

- 20 El Oriente, Fabrica de Tabacos, Inc., vs. Posadas 56 Phil. 147, September 21, 1931Document7 pages20 El Oriente, Fabrica de Tabacos, Inc., vs. Posadas 56 Phil. 147, September 21, 1931joyeduardoNo ratings yet

- Plaintiff-Appellant Vs Vs Defendant-Appellee Gibbs & Mcdonough Roman Ozaeta, Attorney-General JaranillaDocument4 pagesPlaintiff-Appellant Vs Vs Defendant-Appellee Gibbs & Mcdonough Roman Ozaeta, Attorney-General JaranillaGael MoralesNo ratings yet

- EL ORIENTE, FABRICA DE TABACOS, INC., Plaintiff-Appellant, vs. JUAN POSADASDocument5 pagesEL ORIENTE, FABRICA DE TABACOS, INC., Plaintiff-Appellant, vs. JUAN POSADASRobert Jayson UyNo ratings yet

- Insurance CasesDocument64 pagesInsurance CasesDANICA FLORESNo ratings yet

- Insurance CasesDocument63 pagesInsurance CasesDANICA FLORESNo ratings yet

- Gibbs and Mcdonough and Roman Ozaeta For Appellant. Attorney-General Jaranilla For AppelleeDocument3 pagesGibbs and Mcdonough and Roman Ozaeta For Appellant. Attorney-General Jaranilla For AppelleeAbegail AtokNo ratings yet

- 6 El Oriente Fabrica vs. Posadas PDFDocument4 pages6 El Oriente Fabrica vs. Posadas PDFKrisleen AbrenicaNo ratings yet

- El Oriente Fabrica vs. PosadasDocument3 pagesEl Oriente Fabrica vs. Posadasadek_saneNo ratings yet

- 17 El Oriente v. PosadasDocument2 pages17 El Oriente v. PosadasJericAquipelNo ratings yet

- G.R. No. 34774Document3 pagesG.R. No. 34774Hanifa D. Al-ObinayNo ratings yet

- El Oriente Vs Posadas and CirDocument2 pagesEl Oriente Vs Posadas and CirNatasha MilitarNo ratings yet

- Chapter 3 9 Cases TaxDocument15 pagesChapter 3 9 Cases TaxbcarNo ratings yet

- El Oriente v. Posadas 56 Phil 147 DoctrineDocument28 pagesEl Oriente v. Posadas 56 Phil 147 DoctrineShiela MarieNo ratings yet

- Gibbs and Mcdonough and Roman Ozaeta For Appellant. Attorney-General Jaranilla For AppelleeDocument7 pagesGibbs and Mcdonough and Roman Ozaeta For Appellant. Attorney-General Jaranilla For AppelleeMaisie ZabalaNo ratings yet

- 57 El Oriente vs. PosadasDocument7 pages57 El Oriente vs. PosadasisaaabelrfNo ratings yet

- 4 El Oriente Fabrica Vs PosadasDocument4 pages4 El Oriente Fabrica Vs PosadasAngelo ParaoNo ratings yet

- El Oriente v. Posadas - Taxability of Insurance Proceeds 56 PHIL 147 (1931)Document3 pagesEl Oriente v. Posadas - Taxability of Insurance Proceeds 56 PHIL 147 (1931)mcfalcantaraNo ratings yet

- Digest InsuraDocument35 pagesDigest InsuraMartynov MedinaNo ratings yet

- Case Digest 6Document7 pagesCase Digest 6Emmanuel Enrico de VeraNo ratings yet

- Fisher Vs TrinidadDocument11 pagesFisher Vs TrinidadJeff GomezNo ratings yet

- Fisher and de Witt and Antonio M. Opisso For Appellants. Acting Attorney-General Tuason For AppelleeDocument6 pagesFisher and de Witt and Antonio M. Opisso For Appellants. Acting Attorney-General Tuason For AppelleeAimie Razul-AparecioNo ratings yet

- Alson N. Johnson and Margaret C. Johnson v. Commissioner of Internal Revenue, 574 F.2d 189, 4th Cir. (1978)Document3 pagesAlson N. Johnson and Margaret C. Johnson v. Commissioner of Internal Revenue, 574 F.2d 189, 4th Cir. (1978)Scribd Government DocsNo ratings yet

- Commissioner of Internal Revenue v. Guerrero GR L 20942 22 September 1967 en Banc Fernando JDocument5 pagesCommissioner of Internal Revenue v. Guerrero GR L 20942 22 September 1967 en Banc Fernando JMidzfar OmarNo ratings yet

- m2 TaxDocument52 pagesm2 Taxsoojung jungNo ratings yet

- Insurable Interest El Oriente V PosadasDocument1 pageInsurable Interest El Oriente V PosadasJeremiah John Soriano NicolasNo ratings yet

- Fisher v. Trinidad G.R. No. L-17518 October 30, 1922Document10 pagesFisher v. Trinidad G.R. No. L-17518 October 30, 1922aNo ratings yet

- Cir v. Suter 27 Scra 152 (1969)Document4 pagesCir v. Suter 27 Scra 152 (1969)FranzMordenoNo ratings yet

- United States Court of Appeals Third CircuitDocument8 pagesUnited States Court of Appeals Third CircuitScribd Government DocsNo ratings yet

- Manila Electric Vs AL YatcoDocument4 pagesManila Electric Vs AL Yatcolen_dy010487No ratings yet

- Jurisprudence On Stock DividendDocument4 pagesJurisprudence On Stock Dividendfrancis_asd2003No ratings yet

- Corporation Code 3Document121 pagesCorporation Code 3Ber Sib JosNo ratings yet

- Dewitt, Perkins and Ponce Enrile For Appellant. Office of The Solicitor-General Hilado For AppelleeDocument14 pagesDewitt, Perkins and Ponce Enrile For Appellant. Office of The Solicitor-General Hilado For AppelleeSam B. SucalitNo ratings yet

- Young Motor Company, Inc. v. Commissioner of Internal Revenue, 339 F.2d 481, 1st Cir. (1964)Document3 pagesYoung Motor Company, Inc. v. Commissioner of Internal Revenue, 339 F.2d 481, 1st Cir. (1964)Scribd Government DocsNo ratings yet

- Taxation - Wave 2 CDDocument12 pagesTaxation - Wave 2 CDMenchu G. MabanNo ratings yet

- 16 Manila Electric Co Vs YatcoDocument5 pages16 Manila Electric Co Vs YatcoIsa AriasNo ratings yet

- Republic vs. Sunlife Assurance Company of Canada (GR No. 15805 OCTOBER 14, 2005)Document9 pagesRepublic vs. Sunlife Assurance Company of Canada (GR No. 15805 OCTOBER 14, 2005)Don TiansayNo ratings yet

- MANILA GAS CORPORATION, Plaintiff and Appellant, vs. THE COLLECTOR OF INTERNAL REVENUE, Defendant and AppelleeDocument77 pagesMANILA GAS CORPORATION, Plaintiff and Appellant, vs. THE COLLECTOR OF INTERNAL REVENUE, Defendant and AppelleeWarly PabloNo ratings yet

- Compañia General de Tabacos de Filipinas v. Collector of Internal Revenue, 275 U.S. 87 (1927)Document10 pagesCompañia General de Tabacos de Filipinas v. Collector of Internal Revenue, 275 U.S. 87 (1927)Scribd Government DocsNo ratings yet

- Gomez vs. PalomarDocument10 pagesGomez vs. PalomarANgel Go CasañaNo ratings yet

- Cathay Insurance Co., Inc. v. Court of AppealsDocument7 pagesCathay Insurance Co., Inc. v. Court of AppealsJico FarinasNo ratings yet

- 5 Commissioner - of - Internal - Revenue - v. - Court - of PDFDocument23 pages5 Commissioner - of - Internal - Revenue - v. - Court - of PDFdenbar15No ratings yet

- C. PEREZ RUBIO Vs CADocument4 pagesC. PEREZ RUBIO Vs CANympa VillanuevaNo ratings yet

- Qua Chee GanDocument10 pagesQua Chee GanAnthony AraulloNo ratings yet

- S. Jack Musick v. Puerto Rico Telephone Company, 357 F.2d 603, 1st Cir. (1966)Document4 pagesS. Jack Musick v. Puerto Rico Telephone Company, 357 F.2d 603, 1st Cir. (1966)Scribd Government DocsNo ratings yet

- Manila Electric Vs YatcoDocument6 pagesManila Electric Vs Yatcobraindead_91No ratings yet

- Fisher v. Trinidad, G.R. No. L-17518, October 30, 1922Document13 pagesFisher v. Trinidad, G.R. No. L-17518, October 30, 1922zacNo ratings yet

- Rizal Commercial Banking Corporation vs. Court of Appeals: 292 Supreme Court Reports AnnotatedDocument18 pagesRizal Commercial Banking Corporation vs. Court of Appeals: 292 Supreme Court Reports AnnotatedAlexiss Mace JuradoNo ratings yet

- Delsan Transport Lines, Inc. vs. Court of Appeals: 24 Supreme Court Reports AnnotatedDocument9 pagesDelsan Transport Lines, Inc. vs. Court of Appeals: 24 Supreme Court Reports AnnotatedAlexiss Mace JuradoNo ratings yet

- Pioneer Insurance & Surety Corporation vs. Court of Appeals: 668 Supreme Court Reports AnnotatedDocument12 pagesPioneer Insurance & Surety Corporation vs. Court of Appeals: 668 Supreme Court Reports AnnotatedAlexiss Mace JuradoNo ratings yet

- (C. Insurable Interest) Gaisano Cagayan, Inc. vs. Insurance Company of North America, 490 SCRA 286, G.R. No. 147839 June 8, 2006Document11 pages(C. Insurable Interest) Gaisano Cagayan, Inc. vs. Insurance Company of North America, 490 SCRA 286, G.R. No. 147839 June 8, 2006Alexiss Mace JuradoNo ratings yet

- (A. Subject Matter) Eastern Shipping Lines, Inc. vs. Prudential Guarantee and Assurance, Inc., 599 SCRA 565, G.R. No. 174116 September 11, 2009Document13 pages(A. Subject Matter) Eastern Shipping Lines, Inc. vs. Prudential Guarantee and Assurance, Inc., 599 SCRA 565, G.R. No. 174116 September 11, 2009Alexiss Mace JuradoNo ratings yet

- 3) Perez vs. Court of Appeals, 323 SCRA 613, G.R. No. 112329 January 28, 2000Document7 pages3) Perez vs. Court of Appeals, 323 SCRA 613, G.R. No. 112329 January 28, 2000Alexiss Mace JuradoNo ratings yet

- 12) Oriental Assurance Corporation vs. Ong, 842 SCRA 337, G.R. No. 189524 October 11, 2017Document19 pages12) Oriental Assurance Corporation vs. Ong, 842 SCRA 337, G.R. No. 189524 October 11, 2017Alexiss Mace JuradoNo ratings yet

- 9) F.F. Cruz and Co., Inc. vs. Court of Appeals, 164 SCRA 731, No. L-52732 August 29, 1988Document6 pages9) F.F. Cruz and Co., Inc. vs. Court of Appeals, 164 SCRA 731, No. L-52732 August 29, 1988Alexiss Mace JuradoNo ratings yet

- Assurance Company of Canada.: 264 Philippine Reports AnnotatedDocument4 pagesAssurance Company of Canada.: 264 Philippine Reports AnnotatedAlexiss Mace JuradoNo ratings yet

- (B. Parties To The Contract) Valenzuela vs. Court of Appeals, 191 SCRA 1, G.R. No. 83122 October 19, 1990Document13 pages(B. Parties To The Contract) Valenzuela vs. Court of Appeals, 191 SCRA 1, G.R. No. 83122 October 19, 1990Alexiss Mace JuradoNo ratings yet

- 538 Philippine Reports Annotated: Lampano vs. JoseDocument4 pages538 Philippine Reports Annotated: Lampano vs. JoseAlexiss Mace JuradoNo ratings yet

- Delsan Transport Lines, Inc. vs. Court of Appeals: 24 Supreme Court Reports AnnotatedDocument9 pagesDelsan Transport Lines, Inc. vs. Court of Appeals: 24 Supreme Court Reports AnnotatedAlexiss Mace JuradoNo ratings yet

- Rizal Commercial Banking Corporation vs. Court of Appeals: 292 Supreme Court Reports AnnotatedDocument18 pagesRizal Commercial Banking Corporation vs. Court of Appeals: 292 Supreme Court Reports AnnotatedAlexiss Mace JuradoNo ratings yet

- Insular Life v. EbradoDocument12 pagesInsular Life v. EbradoRaymund CallejaNo ratings yet

- Course Outline For RPHDocument1 pageCourse Outline For RPHkate buyuccanNo ratings yet

- Iut Iuat 015 ExDocument32 pagesIut Iuat 015 ExKyaw KyawNo ratings yet

- Case of Handyside v. The United KingdomDocument34 pagesCase of Handyside v. The United KingdomhilancelNo ratings yet

- Fabricated Presidential Pardon Attempted by Alexander LeszczynskiDocument11 pagesFabricated Presidential Pardon Attempted by Alexander LeszczynskiKinsey CrowleyNo ratings yet

- Schools Division of Isabela: November 26, 2020Document5 pagesSchools Division of Isabela: November 26, 2020Zahjid CallangNo ratings yet

- Slovacko DrzavljanstvoDocument4 pagesSlovacko DrzavljanstvoRadic DusanNo ratings yet

- Gateway 2 TB Unit 2 WM PDFDocument24 pagesGateway 2 TB Unit 2 WM PDFjohnNo ratings yet

- Case 71 - 80Document121 pagesCase 71 - 80Keplot LirpaNo ratings yet

- Signature Not VerifiedDocument43 pagesSignature Not VerifiedLAMOS TECHNOLOGY SOLUTIONS PRIVATE LIMITEDNo ratings yet

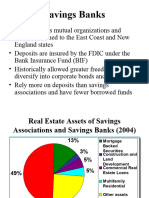

- Savings BanksDocument7 pagesSavings BanksLara KhanNo ratings yet

- Jonathan Moffett - 26 July 2008 Legitimate ExpectationDocument20 pagesJonathan Moffett - 26 July 2008 Legitimate ExpectationMaurizio BusuNo ratings yet

- Bone Grafting HCP Spine Marrow Cellution Bma Surgical Technique Guide Pmd018207Document16 pagesBone Grafting HCP Spine Marrow Cellution Bma Surgical Technique Guide Pmd018207Satyam PatelNo ratings yet

- Lewis Hanke - The Requerimiento and Its Interpreters Revista de Historia de América Nro 1 1938Document10 pagesLewis Hanke - The Requerimiento and Its Interpreters Revista de Historia de América Nro 1 1938FernandoHuyoaNo ratings yet

- WB Panchayat Act 1973 GDocument195 pagesWB Panchayat Act 1973 GArnab RayNo ratings yet

- FCC Factory - MATVDocument2 pagesFCC Factory - MATVViên LêNo ratings yet

- Sab 715823Document1 pageSab 715823Apoorva GowdaNo ratings yet

- Psychology of GraffitiDocument8 pagesPsychology of GraffitiMiles Kilometer CentimeterNo ratings yet

- +1 BIO-ZOO-TM-Vol 1Document42 pages+1 BIO-ZOO-TM-Vol 1arulmurugan pNo ratings yet

- LTD CasesDocument177 pagesLTD CasesjacquelinemactalNo ratings yet