You might also like

- 33 1-3 - 093 - J Dilla's Donuts - Jordan Ferguson (Retail) PDFDocument147 pages33 1-3 - 093 - J Dilla's Donuts - Jordan Ferguson (Retail) PDFNicolas GomezNo ratings yet

- Natural Law's Rise and FallDocument17 pagesNatural Law's Rise and FallNoel James100% (2)

- The Advanced Trauma Operative Management Course inDocument6 pagesThe Advanced Trauma Operative Management Course inFathiH.SaadNo ratings yet

- RDSO Drawings Download LinkDocument76 pagesRDSO Drawings Download Linksudhakarrrrrr73% (15)

- Presentation of E Commerce Website ProjectDocument13 pagesPresentation of E Commerce Website ProjectSibu Star25% (4)

- Artificial Lift For Guest LectureDocument117 pagesArtificial Lift For Guest LectureZenga Harsya Prakarsa100% (1)

- RDSO Master List of DrawingsDocument65 pagesRDSO Master List of Drawingssudhakarrrrrr100% (1)

- Railway Overhead Conductors CatalogDocument14 pagesRailway Overhead Conductors CatalogsudhakarrrrrrNo ratings yet

- Indonesia Cement Industry Focus: Supply Glut and Stiff Competition to Pressure MarginsDocument25 pagesIndonesia Cement Industry Focus: Supply Glut and Stiff Competition to Pressure MarginsRendy SentosaNo ratings yet

- Jltre Reinsurance Market Prospective 2018 Final PDFDocument24 pagesJltre Reinsurance Market Prospective 2018 Final PDFbhaskar_58No ratings yet

- Why Invest in TurkeyDocument20 pagesWhy Invest in TurkeyAli Gokhan KocanNo ratings yet

- Jakarta Officemarket Report 2q 2012 PDFDocument10 pagesJakarta Officemarket Report 2q 2012 PDFRizal NoorNo ratings yet

- ETFS Investment Insights April 2017 - Broad Commodities A Key Alternative InvestmentDocument3 pagesETFS Investment Insights April 2017 - Broad Commodities A Key Alternative InvestmentAnonymous Ht0MIJNo ratings yet

- 2024 M&A outlookDocument9 pages2024 M&A outlookyinjara.buyerNo ratings yet

- The Rise of Intangible Investments and The Implications For InvestorsDocument34 pagesThe Rise of Intangible Investments and The Implications For InvestorsLaurent MilletNo ratings yet

- Beckhoff Products 2021Document104 pagesBeckhoff Products 2021amir12345678No ratings yet

- 580c2bd2-6d1c-4689-8c18-7f84c03352be-2105895954Document4 pages580c2bd2-6d1c-4689-8c18-7f84c03352be-2105895954Sirapob ChitmeesilpNo ratings yet

- Trade Integration in Latin America and the Caribbean: Opportunities and ChallengesDocument10 pagesTrade Integration in Latin America and the Caribbean: Opportunities and Challengessteve britoNo ratings yet

- IDirect Pidilite Q1FY22Document8 pagesIDirect Pidilite Q1FY22Ranjith ChackoNo ratings yet

- Steel Authority of India Limited - 44 - QuarterUpdateDocument14 pagesSteel Authority of India Limited - 44 - QuarterUpdateNaveen KhandelwalNo ratings yet

- Fy 201112 Annual ReportDocument135 pagesFy 201112 Annual ReportNguyễn Thị Thanh ThúyNo ratings yet

- Public Economics Indirect TaxationDocument41 pagesPublic Economics Indirect TaxationTimore FrancisNo ratings yet

- Horizon Housing REIT PLC FactsheetDocument3 pagesHorizon Housing REIT PLC FactsheetSean SongNo ratings yet

- Measuring Manufacturing Production in SingaporeDocument16 pagesMeasuring Manufacturing Production in SingaporeSanja AngNo ratings yet

- HK Macro EnglishDocument14 pagesHK Macro EnglishEmily TranNo ratings yet

- Century SPARK Q2FY21 12nov20Document5 pagesCentury SPARK Q2FY21 12nov20Tai TranNo ratings yet

- Ayala 2012 BriefingDocument27 pagesAyala 2012 BriefingAnthony GalayNo ratings yet

- Indonesia Cement SectorDocument4 pagesIndonesia Cement SectorRendy SentosaNo ratings yet

- The Contango Trade A Cost of Capital Competition PDF DataDocument7 pagesThe Contango Trade A Cost of Capital Competition PDF DataSandesh Tukaram GhandatNo ratings yet

- UPL Company Update - 030520 - Emkay PDFDocument15 pagesUPL Company Update - 030520 - Emkay PDFshaikhsaadahmedNo ratings yet

- Cement Sector 11-07-2017-Next CapitalDocument30 pagesCement Sector 11-07-2017-Next Capitalusamamalik1989No ratings yet

- Bangkok Residential MarketView Q3 2017Document4 pagesBangkok Residential MarketView Q3 2017AnthonNo ratings yet

- Project Blue Nile - Take Home ONe TEmplate PDFDocument2 pagesProject Blue Nile - Take Home ONe TEmplate PDFYogesh PanwarNo ratings yet

- IO Motorcycle 2017 EN PDFDocument7 pagesIO Motorcycle 2017 EN PDFKaren PendumaNo ratings yet

- J.P. Morgan report analyzes factors driving Bitcoin mining costsDocument5 pagesJ.P. Morgan report analyzes factors driving Bitcoin mining costsmittleNo ratings yet

- NBCC GovtDocument40 pagesNBCC GovtDr. Anamika JhaNo ratings yet

- The India Advantage After The Comprehensive Economic Partnership AgreementDocument51 pagesThe India Advantage After The Comprehensive Economic Partnership Agreementrohitgupta11288No ratings yet

- FOXBORO IA - Series - Lifecycle - Product - Phase - ListingDocument26 pagesFOXBORO IA - Series - Lifecycle - Product - Phase - Listingtricucha priyantoNo ratings yet

- Oklahoma Budget Trends and Outlook (Rev. Jan 13, 2010)Document39 pagesOklahoma Budget Trends and Outlook (Rev. Jan 13, 2010)dblattokNo ratings yet

- Hugh Donovan, Eight-Year Review of The Full Depth Reclamation Process in The City of EdmontonDocument40 pagesHugh Donovan, Eight-Year Review of The Full Depth Reclamation Process in The City of Edmontoneye2iNo ratings yet

- BASF Chemicals ConferenceDocument49 pagesBASF Chemicals ConferenceValeria ShakarovaNo ratings yet

- 2023 09 YPF Investor-Presentation Sep23Document9 pages2023 09 YPF Investor-Presentation Sep23dsv.newNo ratings yet

- On RIL AND RPLDocument27 pagesOn RIL AND RPLpramod_2300No ratings yet

- BajajDocument4 pagesBajajAkhtar RazaNo ratings yet

- Analysts 20030227Document41 pagesAnalysts 20030227gsameera676No ratings yet

- CanadiansForTaxFairness eDocument7 pagesCanadiansForTaxFairness ejuliawilma123321No ratings yet

- Mariana Mazzucato Beyond Markert FailureDocument36 pagesMariana Mazzucato Beyond Markert FailureFrancisco Gallo MNo ratings yet

- All The Money in The World September 20, 2018 PDFDocument48 pagesAll The Money in The World September 20, 2018 PDFSittidath PrasertrungruangNo ratings yet

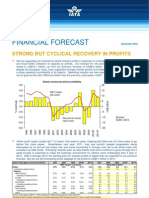

- STRONG BUT CYCLICAL RECOVERY IN AIRLINE PROFITS FORECASTDocument4 pagesSTRONG BUT CYCLICAL RECOVERY IN AIRLINE PROFITS FORECASTDaniel WongNo ratings yet

- Business Growth PlanDocument29 pagesBusiness Growth PlanSanjeev KhannaNo ratings yet

- Can We Get Rid of Palm OilDocument3 pagesCan We Get Rid of Palm OiljaboerboyNo ratings yet

- BC WatershedDocument15 pagesBC Watershedshihan ZhangNo ratings yet

- How earnings growth drives share prices over the long runDocument20 pagesHow earnings growth drives share prices over the long runravstuhiNo ratings yet

- Esmap Vulnerability MoroccoDocument25 pagesEsmap Vulnerability Moroccoanouar topologyNo ratings yet

- Country Risk Analysis - PPTDocument12 pagesCountry Risk Analysis - PPTsridhar mohantyNo ratings yet

- r22 AllocationDocument1 pager22 AllocationHarry CoxNo ratings yet

- Rebuilding Our Tomorrow: Kobe Steel Group Annual Report 2013Document82 pagesRebuilding Our Tomorrow: Kobe Steel Group Annual Report 2013Didit PandithaNo ratings yet

- An Empirical Study in Albania of Foreign Direct Investments and Economic Growth RelationshipDocument10 pagesAn Empirical Study in Albania of Foreign Direct Investments and Economic Growth RelationshipVidya YuniantiNo ratings yet

- Consumer Durables Lockdown Mars Performance Yet Again HSIE 2021Document22 pagesConsumer Durables Lockdown Mars Performance Yet Again HSIE 2021GowtamdNo ratings yet

- Nse: Itc PRICE: INR 203.10Document7 pagesNse: Itc PRICE: INR 203.10Shresth GuptaNo ratings yet

- Energy: Figure 3.1: Power ShortageDocument18 pagesEnergy: Figure 3.1: Power ShortageSyed Muhammad Ahsan RizviNo ratings yet

- BTS Q1 2023 FinalDocument12 pagesBTS Q1 2023 FinalAroa López de CalleNo ratings yet

- Transition Report 2015 16 D Credit CrunchDocument22 pagesTransition Report 2015 16 D Credit CrunchindosiataNo ratings yet

- Minda Industries - Q2FY21 - Result Update-202011180844080344898Document3 pagesMinda Industries - Q2FY21 - Result Update-202011180844080344898flying400No ratings yet

- Dividend DecisionsDocument36 pagesDividend DecisionsMohammed ZakriyaNo ratings yet

- Evolution of The Indian Economy 2006 - LemoineDocument30 pagesEvolution of The Indian Economy 2006 - LemoineNeha KantNo ratings yet

- Clay Refractory Products World Summary: Market Sector Values & Financials by CountryFrom EverandClay Refractory Products World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Irussor Sor 24 12 2019 PDFDocument128 pagesIrussor Sor 24 12 2019 PDFPARTH DOSHI0% (1)

- VSP BrochureDocument33 pagesVSP BrochuresudhakarrrrrrNo ratings yet

- Product enDocument35 pagesProduct enmeetvinayak2007No ratings yet

- Handbook On Breakdown Management of OHE PDFDocument54 pagesHandbook On Breakdown Management of OHE PDFPrabjyot SinghNo ratings yet

- Smartdek 51Document12 pagesSmartdek 51Fairly InsurgentNo ratings yet

- Dr. Fixit Raincoat Waterproof CoatingDocument3 pagesDr. Fixit Raincoat Waterproof CoatingsudhakarrrrrrNo ratings yet

- Asian Paints SmartCare Damp Proof WaterproofingDocument2 pagesAsian Paints SmartCare Damp Proof WaterproofingchandanNo ratings yet

- Project management key for pharma successDocument13 pagesProject management key for pharma successsudhakarrrrrrNo ratings yet

- Top 10 Communication Skills - What Are TheyDocument6 pagesTop 10 Communication Skills - What Are TheysudhakarrrrrrNo ratings yet

- NABL Accredited SKC Compliance Lab Pvt. Ltd. Product Testing and Certification ServicesDocument23 pagesNABL Accredited SKC Compliance Lab Pvt. Ltd. Product Testing and Certification ServicessudhakarrrrrrNo ratings yet

- 5NRJHL Saipem FY2020 Results JMEEBODocument42 pages5NRJHL Saipem FY2020 Results JMEEBOsudhakarrrrrrNo ratings yet

- Energy Resources 2Document20 pagesEnergy Resources 2ParmeshwarPaulNo ratings yet

- Print - The Worldwide Market For Power Transmission & Distribution (T&D) Equipment, 2019 - New Infrastructure, Upgrade and Expansion Projects in Developing Countries Offer Immense Growth PotentialDocument6 pagesPrint - The Worldwide Market For Power Transmission & Distribution (T&D) Equipment, 2019 - New Infrastructure, Upgrade and Expansion Projects in Developing Countries Offer Immense Growth PotentialsudhakarrrrrrNo ratings yet

- Dr. Fixit Primeseal - AE: High Opacity Primer For Wall CoatingDocument2 pagesDr. Fixit Primeseal - AE: High Opacity Primer For Wall CoatingsudhakarrrrrrNo ratings yet

- KPTL Annual Report 2017 18Document252 pagesKPTL Annual Report 2017 18Saurabh PatelNo ratings yet

- Option Chain (Equity Derivatives)Document1 pageOption Chain (Equity Derivatives)sudhakarrrrrrNo ratings yet

- Irena 2019Document60 pagesIrena 2019madhanNo ratings yet

- Bajfin-OC-17th May - 30th MayDocument2 pagesBajfin-OC-17th May - 30th MaysudhakarrrrrrNo ratings yet

- Nifty - 25th Apr Exp at 3.12 PMDocument2 pagesNifty - 25th Apr Exp at 3.12 PMsudhakarrrrrrNo ratings yet

- Nifty - 11th Apr Expiry at 3 PMDocument2 pagesNifty - 11th Apr Expiry at 3 PMsudhakarrrrrrNo ratings yet

- Option Chain (Equity Derivatives)Document2 pagesOption Chain (Equity Derivatives)sudhakarrrrrrNo ratings yet

- Option Chain (Equity Derivatives)Document2 pagesOption Chain (Equity Derivatives)sudhakarrrrrrNo ratings yet

- ABB India Ltd. - Multiple Chart Pattern Breakout Confirmation - Investing - Com IndiaDocument3 pagesABB India Ltd. - Multiple Chart Pattern Breakout Confirmation - Investing - Com IndiasudhakarrrrrrNo ratings yet

- Ultratech Cement Limited - Ultracemco: Prev. Close Open High Low CloseDocument1 pageUltratech Cement Limited - Ultracemco: Prev. Close Open High Low ClosesudhakarrrrrrNo ratings yet

- Option Chain (Equity Derivatives)Document2 pagesOption Chain (Equity Derivatives)sudhakarrrrrrNo ratings yet

- Nifty OC 08-04-11th ExpDocument2 pagesNifty OC 08-04-11th ExpsudhakarrrrrrNo ratings yet

- Option Chain (Equity Derivatives)Document2 pagesOption Chain (Equity Derivatives)sudhakarrrrrrNo ratings yet

- Finals (3. LP) Termination and RepairDocument4 pagesFinals (3. LP) Termination and RepairAmelyn Goco MañosoNo ratings yet

- FF6GABAYDocument520 pagesFF6GABAYaringkinkingNo ratings yet

- Controller Spec SheetDocument4 pagesController Spec SheetLuis JesusNo ratings yet

- MPT Training CentreDocument11 pagesMPT Training CentreGrace PMNo ratings yet

- Grammar Marwa 22Document5 pagesGrammar Marwa 22YAGOUB MUSANo ratings yet

- Cost EstimationDocument4 pagesCost EstimationMuhammed Azhar P JNo ratings yet

- Customer Satisfaction Towards Honda Two Wheeler: Presented By: Somil Modi (20152002) BBA-MBA 2015Document9 pagesCustomer Satisfaction Towards Honda Two Wheeler: Presented By: Somil Modi (20152002) BBA-MBA 2015Inayat BaktooNo ratings yet

- Airframe QuestionsDocument41 pagesAirframe QuestionsJDany Rincon Rojas100% (1)

- Subtraction Strategies That Lead To RegroupingDocument6 pagesSubtraction Strategies That Lead To Regroupingapi-171857844100% (1)

- Dade Girls SoccerDocument1 pageDade Girls SoccerMiami HeraldNo ratings yet

- Srimad Bhagavatam 2nd CantoDocument25 pagesSrimad Bhagavatam 2nd CantoDeepak K OONo ratings yet

- Capstone PosterDocument1 pageCapstone Posterapi-538849894No ratings yet

- Case Study - FGD PDFDocument9 pagesCase Study - FGD PDFLuthfanTogarNo ratings yet

- Instructions: Skim The Following Job Advertisements. Then, Scan The Text That Follows andDocument2 pagesInstructions: Skim The Following Job Advertisements. Then, Scan The Text That Follows andVasu WinNo ratings yet

- Geoboards in The ClassroomDocument37 pagesGeoboards in The ClassroomDanielle VezinaNo ratings yet

- A CHAIN OF THUNDER: A Novel of The Siege of Vicksburg by Jeff ShaaraDocument13 pagesA CHAIN OF THUNDER: A Novel of The Siege of Vicksburg by Jeff ShaaraRandom House Publishing Group20% (5)

- Data Compilation TemplateDocument257 pagesData Compilation TemplateemelyseuwaseNo ratings yet

- 19C.Revolution and Counter Rev. in Ancient India PARTIII PDFDocument94 pages19C.Revolution and Counter Rev. in Ancient India PARTIII PDFVeeramani ManiNo ratings yet

- Test Your Knowledge - Python and Automation - Coursera100Document1 pageTest Your Knowledge - Python and Automation - Coursera100Mario 1229No ratings yet

- Poultry Fool & FinalDocument42 pagesPoultry Fool & Finalaashikjayswal8No ratings yet

- Snorkel: Rapid Training Data Creation With Weak SupervisionDocument17 pagesSnorkel: Rapid Training Data Creation With Weak SupervisionStephane MysonaNo ratings yet

- HCPN Certification Agreement, Partner Agreement-HUAWEI CLOUDDocument9 pagesHCPN Certification Agreement, Partner Agreement-HUAWEI CLOUDSolNo ratings yet

- Recon OpticalDocument3 pagesRecon Opticalthekingfisher1No ratings yet

- ?PMA 138,39,40,41LC Past Initials-1Document53 pages?PMA 138,39,40,41LC Past Initials-1Saqlain Ali Shah100% (1)

- PRACTICE-10 BảnDocument5 pagesPRACTICE-10 BảnBinh Pham ThanhNo ratings yet

- English Reviewer Subject-Verb Agreement Exercise 1Document3 pagesEnglish Reviewer Subject-Verb Agreement Exercise 1Honeybel EmbeeNo ratings yet