You might also like

- Gibbs-vs.-Collector-of-Internal-RevenueDocument15 pagesGibbs-vs.-Collector-of-Internal-RevenueChristle CorpuzNo ratings yet

- 260-Republic v. Limaco & de Guzman Commercial Co., Inc. G.R. No. L-13081 August 31, 1962Document4 pages260-Republic v. Limaco & de Guzman Commercial Co., Inc. G.R. No. L-13081 August 31, 1962Jopan SJNo ratings yet

- Eli D. Goodstein v. Commissioner of Internal Revenue, Commissioner of Internal Revenue v. Eli D. Goodstein, 267 F.2d 127, 1st Cir. (1959)Document7 pagesEli D. Goodstein v. Commissioner of Internal Revenue, Commissioner of Internal Revenue v. Eli D. Goodstein, 267 F.2d 127, 1st Cir. (1959)Scribd Government DocsNo ratings yet

- United States Court of Appeals Third CircuitDocument6 pagesUnited States Court of Appeals Third CircuitScribd Government DocsNo ratings yet

- Court Rules in Favor of Government in Tax Collection CaseDocument4 pagesCourt Rules in Favor of Government in Tax Collection CaseChristiane Marie BajadaNo ratings yet

- Print This DudsDocument65 pagesPrint This DudsNico NicoNo ratings yet

- Pirovano v. CIRDocument2 pagesPirovano v. CIRKennethQueRaymundo100% (1)

- Nannie Carr Harris, Incompetent, and Robert A. Eubanks, Guardian v. Commissioner of Internal Revenue, 477 F.2d 812, 4th Cir. (1973)Document9 pagesNannie Carr Harris, Incompetent, and Robert A. Eubanks, Guardian v. Commissioner of Internal Revenue, 477 F.2d 812, 4th Cir. (1973)Scribd Government DocsNo ratings yet

- Rosenthal v. Commissioner of Internal Revenue, 205 F.2d 505, 2d Cir. (1953)Document10 pagesRosenthal v. Commissioner of Internal Revenue, 205 F.2d 505, 2d Cir. (1953)Scribd Government DocsNo ratings yet

- Gonzales V Court of Tax AppealsDocument10 pagesGonzales V Court of Tax AppealsadeeNo ratings yet

- Lladoc Vs Commisioner of Internal RevenueDocument13 pagesLladoc Vs Commisioner of Internal RevenuekitakatttNo ratings yet

- Tax Deduction Allowed for Interest Paid on Estate and Inheritance TaxesDocument5 pagesTax Deduction Allowed for Interest Paid on Estate and Inheritance Taxeskim zeus ga-anNo ratings yet

- United States v. Bernard Feinberg, Administrator of The Estate of Joseph Saladoff, Deceased, 372 F.2d 352, 3rd Cir. (1967)Document21 pagesUnited States v. Bernard Feinberg, Administrator of The Estate of Joseph Saladoff, Deceased, 372 F.2d 352, 3rd Cir. (1967)Scribd Government DocsNo ratings yet

- Helen Rich Findlay v. Commissioner of Internal Revenue, 332 F.2d 620, 2d Cir. (1964)Document6 pagesHelen Rich Findlay v. Commissioner of Internal Revenue, 332 F.2d 620, 2d Cir. (1964)Scribd Government DocsNo ratings yet

- Lamb v. Smith, Collector of Internal Revenue, 183 F.2d 938, 3rd Cir. (1950)Document8 pagesLamb v. Smith, Collector of Internal Revenue, 183 F.2d 938, 3rd Cir. (1950)Scribd Government DocsNo ratings yet

- Gonzales Vs CTADocument6 pagesGonzales Vs CTAEANo ratings yet

- Philippines Supreme Court rules on tax deduction for US citizensDocument92 pagesPhilippines Supreme Court rules on tax deduction for US citizens001nooneNo ratings yet

- G.R. No. L-16626 October 29, 1966 Commissioner of Internal Revenue, Petitioner, CARLOS PALANCA, JR., RespondentDocument6 pagesG.R. No. L-16626 October 29, 1966 Commissioner of Internal Revenue, Petitioner, CARLOS PALANCA, JR., RespondentJopan SJNo ratings yet

- 66 CIR Vs LednickyDocument9 pages66 CIR Vs LednickyYaz CarlomanNo ratings yet

- United States Court of Appeals, Fifth CircuitDocument6 pagesUnited States Court of Appeals, Fifth CircuitScribd Government DocsNo ratings yet

- Commissioner vs. PalancaDocument6 pagesCommissioner vs. Palancacmv mendozaNo ratings yet

- Bradford Hotel Operating Co. v. Commissioner of Internal Revenue, 244 F.2d 876, 1st Cir. (1957)Document10 pagesBradford Hotel Operating Co. v. Commissioner of Internal Revenue, 244 F.2d 876, 1st Cir. (1957)Scribd Government DocsNo ratings yet

- United States Court of Appeals Third CircuitDocument11 pagesUnited States Court of Appeals Third CircuitScribd Government DocsNo ratings yet

- In Re Estate of Ida Wray Nissen, Deceased. Wachovia Bank and Trust Company v. Commissioner of Internal Revenue, 345 F.2d 230, 4th Cir. (1965)Document8 pagesIn Re Estate of Ida Wray Nissen, Deceased. Wachovia Bank and Trust Company v. Commissioner of Internal Revenue, 345 F.2d 230, 4th Cir. (1965)Scribd Government DocsNo ratings yet

- United States v. Consolidated Edison Co. of NY, 366 U.S. 380 (1961)Document9 pagesUnited States v. Consolidated Edison Co. of NY, 366 U.S. 380 (1961)Scribd Government DocsNo ratings yet

- Tax Cases: The Revised OneDocument16 pagesTax Cases: The Revised OneDaniel Danjur DagumanNo ratings yet

- Collector of Internal Revenue vs. FisherDocument25 pagesCollector of Internal Revenue vs. Fisherjosiah9_5No ratings yet

- Guide Notes On Donor'S Tax Donor'S TaxDocument10 pagesGuide Notes On Donor'S Tax Donor'S TaxNori LolaNo ratings yet

- United States Court of Appeals Second Circuit.: Nos. 64-67, Dockets 28244-28247Document10 pagesUnited States Court of Appeals Second Circuit.: Nos. 64-67, Dockets 28244-28247Scribd Government DocsNo ratings yet

- Property - Full Text - Co-OwnershipDocument80 pagesProperty - Full Text - Co-OwnershipElaine Belle OgayonNo ratings yet

- Conwi vs. CA (G.R. No. 48532 August 31, 1992) - 4Document8 pagesConwi vs. CA (G.R. No. 48532 August 31, 1992) - 4Amir Nazri KaibingNo ratings yet

- Tax Digests For January 30Document3 pagesTax Digests For January 30SuiNo ratings yet

- Palanca Vs CirDocument5 pagesPalanca Vs Ciryelina_kuranNo ratings yet

- Sales Case Digests (Set1)Document20 pagesSales Case Digests (Set1)Kara LeonidasNo ratings yet

- Joseph B. and Josephine L. Simon v. Commissioner of Internal Revenue, Commissioner of Internal Revenue v. Joseph B. and Josephine L. Simon, 285 F.2d 422, 3rd Cir. (1961)Document6 pagesJoseph B. and Josephine L. Simon v. Commissioner of Internal Revenue, Commissioner of Internal Revenue v. Joseph B. and Josephine L. Simon, 285 F.2d 422, 3rd Cir. (1961)Scribd Government DocsNo ratings yet

- Kay M. Offutt v. Commissioner of Internal Revenue, 276 F.2d 471, 4th Cir. (1960)Document7 pagesKay M. Offutt v. Commissioner of Internal Revenue, 276 F.2d 471, 4th Cir. (1960)Scribd Government DocsNo ratings yet

- Gibbs vs Commissioner: 30-Day Period to Contest Tax Ruling Begins Upon ReceiptDocument2 pagesGibbs vs Commissioner: 30-Day Period to Contest Tax Ruling Begins Upon ReceiptDannaIngaran100% (1)

- Income Tax CasesDocument19 pagesIncome Tax CasesDawn Lumbas100% (1)

- Conwi vs. CTADocument4 pagesConwi vs. CTAAnonymous sMqziwneNo ratings yet

- Commissioner of Internal Revenue v. Walter H. Mendel and Lillian Mendel, Walter H. Mendel and Lillian Mendel v. Commissioner of Internal Revenue, 351 F.2d 580, 4th Cir. (1965)Document6 pagesCommissioner of Internal Revenue v. Walter H. Mendel and Lillian Mendel, Walter H. Mendel and Lillian Mendel v. Commissioner of Internal Revenue, 351 F.2d 580, 4th Cir. (1965)Scribd Government DocsNo ratings yet

- Joseph R. Holsey and Eleanor T. Holsey v. Commissioner of Internal Revenue, 258 F.2d 865, 3rd Cir. (1958)Document6 pagesJoseph R. Holsey and Eleanor T. Holsey v. Commissioner of Internal Revenue, 258 F.2d 865, 3rd Cir. (1958)Scribd Government DocsNo ratings yet

- C. F. Williams and Jeanne v. Williams v. Commissioner of Internal Revenue, 627 F.2d 1032, 10th Cir. (1980)Document6 pagesC. F. Williams and Jeanne v. Williams v. Commissioner of Internal Revenue, 627 F.2d 1032, 10th Cir. (1980)Scribd Government DocsNo ratings yet

- George Fischer v. Commissioner of Internal Revenue, 288 F.2d 574, 3rd Cir. (1961)Document7 pagesGeorge Fischer v. Commissioner of Internal Revenue, 288 F.2d 574, 3rd Cir. (1961)Scribd Government DocsNo ratings yet

- Tax 2Document106 pagesTax 2Josh NapizaNo ratings yet

- Stephanie Bauer v. John E. Foley, As District Director of Internal Revenue Service, Buffalo District, and The United States, 404 F.2d 1215, 2d Cir. (1968)Document8 pagesStephanie Bauer v. John E. Foley, As District Director of Internal Revenue Service, Buffalo District, and The United States, 404 F.2d 1215, 2d Cir. (1968)Scribd Government DocsNo ratings yet

- United States v. Frank Palermo, Also Known As Frank 'Blinky' Palermo, 259 F.2d 872, 3rd Cir. (1958)Document15 pagesUnited States v. Frank Palermo, Also Known As Frank 'Blinky' Palermo, 259 F.2d 872, 3rd Cir. (1958)Scribd Government DocsNo ratings yet

- Kuehner v. Commissioner of Internal Revenue, 214 F.2d 437, 1st Cir. (1954)Document6 pagesKuehner v. Commissioner of Internal Revenue, 214 F.2d 437, 1st Cir. (1954)Scribd Government DocsNo ratings yet

- Tax DigestsDocument4 pagesTax DigestsRianna VelezNo ratings yet

- Gonzales v CTA Income Tax RulingDocument2 pagesGonzales v CTA Income Tax RulingAnonymous 5MiN6I78I0No ratings yet

- Co - Tax II Case DigestsDocument32 pagesCo - Tax II Case DigestsJoshua Joy CoNo ratings yet

- Donor'S Tax Compilation of Case DigestDocument8 pagesDonor'S Tax Compilation of Case DigestmarydalemNo ratings yet

- 142 - Obillos Vs CIRDocument2 pages142 - Obillos Vs CIRJai HoNo ratings yet

- Tax - Cases - 072017Document89 pagesTax - Cases - 072017Maria ThereseNo ratings yet

- Tax Cases Estate TaxDocument6 pagesTax Cases Estate TaxKristine Jay Perez-CabusogNo ratings yet

- Tax liability of siblings who sold inherited landDocument41 pagesTax liability of siblings who sold inherited landAisaia Jay ToralNo ratings yet

- Tax 2Document327 pagesTax 2Mikhaela Maria VaronaNo ratings yet

- Petitioner Respondents Eusebio D Morales Solicitor GeneralDocument6 pagesPetitioner Respondents Eusebio D Morales Solicitor GeneralHans LazaroNo ratings yet

- Transfer Tax Case DigestDocument30 pagesTransfer Tax Case DigestErneylou RanayNo ratings yet

- Pirovano-vs.-Commissioner-of-Internal-RevenueDocument19 pagesPirovano-vs.-Commissioner-of-Internal-RevenueChristle CorpuzNo ratings yet

- Tolentino v. Secretary of FinanceDocument130 pagesTolentino v. Secretary of FinanceAingel Joy DomingoNo ratings yet

- 5 Commissioner - of - Internal - Revenue - v. - de - La20210505-13-RhztwaDocument25 pages5 Commissioner - of - Internal - Revenue - v. - de - La20210505-13-RhztwaervingabralagbonNo ratings yet

- Petitioner Respondent: Planters Products, Inc., - Fertiphil CorporationDocument19 pagesPetitioner Respondent: Planters Products, Inc., - Fertiphil CorporationOfel Jemaimah OblanNo ratings yet

- 1 ABAKADA Guro v. ErmitaDocument226 pages1 ABAKADA Guro v. ErmitaHannah MedNo ratings yet

- Commissioner of Internal Revenue v. Court of Appeals, G.R. No. 124043, (October 14, 1998) PDFDocument21 pagesCommissioner of Internal Revenue v. Court of Appeals, G.R. No. 124043, (October 14, 1998) PDFArjayNo ratings yet

- Philippine Amusement and Gaming Corp. v. Bureau of Internal RevenueDocument21 pagesPhilippine Amusement and Gaming Corp. v. Bureau of Internal RevenueMichelle Marie TablizoNo ratings yet

- Gerochi v. Department of EnergyDocument18 pagesGerochi v. Department of EnergyAingel Joy DomingoNo ratings yet

- Drugstores Association of The Philippines, Inc. v. National Council On Disability AffairsDocument20 pagesDrugstores Association of The Philippines, Inc. v. National Council On Disability AffairsMichelle Marie TablizoNo ratings yet

- Philippine Court Decision on Tax Overpayment ClaimDocument9 pagesPhilippine Court Decision on Tax Overpayment ClaimNash LedesmaNo ratings yet

- Court Decision on Makati City Tax CaseDocument28 pagesCourt Decision on Makati City Tax CaseNash LedesmaNo ratings yet

- Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument9 pagesSecond Division: Republic of The Philippines Court of Tax Appeals Quezon CityNash LedesmaNo ratings yet

- Second Division: Court of Tax AppealsDocument26 pagesSecond Division: Court of Tax AppealsNash LedesmaNo ratings yet

- 2017-Southern Luzon Drug Corp. v. Department ofDocument56 pages2017-Southern Luzon Drug Corp. v. Department ofRafael Francesco GonzalesNo ratings yet

- VAT on Toll Fees CaseDocument7 pagesVAT on Toll Fees CaseR.A. GregorioNo ratings yet

- Samonte vs. La Salle Greenhills, Inc.Document8 pagesSamonte vs. La Salle Greenhills, Inc.Nash LedesmaNo ratings yet

- Cta 2D CV 07809 D 2009dec16 AssDocument39 pagesCta 2D CV 07809 D 2009dec16 AssNash LedesmaNo ratings yet

- Poseidon Fishing vs. NLRC examines validity of fixed-term contractsDocument9 pagesPoseidon Fishing vs. NLRC examines validity of fixed-term contractsNash LedesmaNo ratings yet

- D.M. Consunji, Inc. vs. GobresDocument7 pagesD.M. Consunji, Inc. vs. GobresNash LedesmaNo ratings yet

- Philippine American Life and General Insurance Company vs. Commissioner of Internal RevenueDocument10 pagesPhilippine American Life and General Insurance Company vs. Commissioner of Internal RevenueNash LedesmaNo ratings yet

- Supreme Court upholds regular status of farm workersDocument6 pagesSupreme Court upholds regular status of farm workersNash LedesmaNo ratings yet

- Abbott Laboratories vs. AlcarazDocument19 pagesAbbott Laboratories vs. AlcarazNash Ledesma100% (1)

- De la Rama Steamship Co. donation to heirs of deceased officer taxableDocument8 pagesDe la Rama Steamship Co. donation to heirs of deceased officer taxableNash LedesmaNo ratings yet

- Tang Ho vs. The Board of Tax AppealsDocument5 pagesTang Ho vs. The Board of Tax AppealsNash LedesmaNo ratings yet

- Kidnapping Case Against Clinic OwnersDocument6 pagesKidnapping Case Against Clinic OwnersNash LedesmaNo ratings yet

- Gonzales vs. AguinaldoDocument5 pagesGonzales vs. AguinaldoNash LedesmaNo ratings yet

- Cayao vs. Del MundoDocument4 pagesCayao vs. Del MundoNash LedesmaNo ratings yet

- Spouses Gestopa vs. Court of AppealsDocument5 pagesSpouses Gestopa vs. Court of AppealsNash LedesmaNo ratings yet

- Vera vs. Fernandez DigestDocument1 pageVera vs. Fernandez DigestNash LedesmaNo ratings yet

- Bureau of Internal Revenue: March 25, 2013 Concerning The Recovery of Unutilized Creditable Input TaxesDocument3 pagesBureau of Internal Revenue: March 25, 2013 Concerning The Recovery of Unutilized Creditable Input TaxesSammy AsanNo ratings yet

- Bank Reconciliation GuideDocument23 pagesBank Reconciliation GuideJohn Anjelo MoraldeNo ratings yet

- Chapter 2 2012Document53 pagesChapter 2 2012Onur YamukNo ratings yet

- Foundations of Finance 9th Edition Keown Solutions Manual 1Document32 pagesFoundations of Finance 9th Edition Keown Solutions Manual 1carita100% (38)

- Financial Statements ChecklistDocument1 pageFinancial Statements ChecklistAsis KoiralaNo ratings yet

- SALUDARES, Jomar S. (ASSIGNMENT FINALS) - ME3B - (ES301-Engineering Economics) PDFDocument2 pagesSALUDARES, Jomar S. (ASSIGNMENT FINALS) - ME3B - (ES301-Engineering Economics) PDFJohn A. CenizaNo ratings yet

- Chattels - Affidavit & Chattels TransferDocument4 pagesChattels - Affidavit & Chattels TransferEvelyn KyaniaNo ratings yet

- Solved Ramon Clarita and Juan Are Shareholders in The Computer ConsultingDocument1 pageSolved Ramon Clarita and Juan Are Shareholders in The Computer ConsultingAnbu jaromiaNo ratings yet

- Intermediate Accouting Testbank ch13Document23 pagesIntermediate Accouting Testbank ch13cthunder_192% (12)

- Original Certificate of Title: THOUSAND (50, 000) SQUARE METERS More orDocument4 pagesOriginal Certificate of Title: THOUSAND (50, 000) SQUARE METERS More orKeepy FamadorNo ratings yet

- MULTIPLE CHOICE FINANCE QUIZDocument2 pagesMULTIPLE CHOICE FINANCE QUIZabigail zipaganNo ratings yet

- Chapter 3-The Recording Process and Accounting CycleDocument7 pagesChapter 3-The Recording Process and Accounting CycleParvez TuhenNo ratings yet

- Banking Practice Unit 3: Opening Accounts of Various Types of CustomersDocument5 pagesBanking Practice Unit 3: Opening Accounts of Various Types of CustomersNandhini VirgoNo ratings yet

- Borrowing Costs: Use The Following Information For The Next Two QuestionsDocument3 pagesBorrowing Costs: Use The Following Information For The Next Two QuestionsXiena100% (1)

- Mid Corporate Branch Consortium ProposalDocument3 pagesMid Corporate Branch Consortium ProposalMSME SULABH TUMAKURUNo ratings yet

- Accounting For PartnershipDocument46 pagesAccounting For PartnershipRejean Dela Cruz100% (1)

- PMPC: Empowering Panabo Communities Through Cooperative ServicesDocument10 pagesPMPC: Empowering Panabo Communities Through Cooperative ServicesChristian MaghanoyNo ratings yet

- Accountancy XI Final Question Paper (2020-21)Document9 pagesAccountancy XI Final Question Paper (2020-21)Ashir SinghNo ratings yet

- Session 7 Case StudyDocument4 pagesSession 7 Case StudyDiajal HooblalNo ratings yet

- Partnership - LiquidationDocument11 pagesPartnership - LiquidationAiziel OrenseNo ratings yet

- Invincble Manufacturing Balance SheetDocument4 pagesInvincble Manufacturing Balance SheetArjun Pratap SinghNo ratings yet

- Legal Fees - CKHTDocument2 pagesLegal Fees - CKHTChe TaNo ratings yet

- Agricultural Land Antichresis AgreementDocument2 pagesAgricultural Land Antichresis AgreementGarNo ratings yet

- Trade and Other ReceivablesDocument21 pagesTrade and Other ReceivablesNoella Marie BaronNo ratings yet

- Amaia PampangaDocument1 pageAmaia PampangadusteezapedaNo ratings yet

- Consumer Lending 12Document131 pagesConsumer Lending 12Nana Akua AseiduaNo ratings yet

- Higher Education Loans BoardDocument8 pagesHigher Education Loans Boardobed jumaNo ratings yet

- Simple & Compound Interest Practice QuestionsDocument2 pagesSimple & Compound Interest Practice QuestionsShiVâ Sãi100% (1)

- Yates Financial ModellingDocument18 pagesYates Financial ModellingJerryJoshuaDiazNo ratings yet

- Module 5 Note Payable and Debt RestructureDocument15 pagesModule 5 Note Payable and Debt Restructuremmh100% (1)

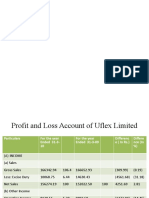

- Friday UFLEXDocument8 pagesFriday UFLEXOnkar TendulkarNo ratings yet