You might also like

- Feasibility Study-Egg Farm - HermelDocument10 pagesFeasibility Study-Egg Farm - Hermelalambaha100% (20)

- Archaeological Systems Theory and Early Mesoamerica - Flannery PDFDocument13 pagesArchaeological Systems Theory and Early Mesoamerica - Flannery PDFYadira Tapia Díaz75% (4)

- Broiler Chicken Production Business Plan ContentsDocument3 pagesBroiler Chicken Production Business Plan Contentskharronn star100% (5)

- Broiler Chicken Production Business Plan ContentsDocument3 pagesBroiler Chicken Production Business Plan Contentskharronn star100% (5)

- AG SCI 208 - Advance Ruminant Production and Management SyllabusDocument4 pagesAG SCI 208 - Advance Ruminant Production and Management SyllabusKRIZZAPEARL VER100% (2)

- Starting Goat Dairy Farm Business PlanDocument5 pagesStarting Goat Dairy Farm Business PlanBHAWANI SINGH TANWAR100% (1)

- Poultry Farm ProposalDocument17 pagesPoultry Farm ProposalNes-tValdez50% (2)

- Table of Contents Poultry Egg Farming Business PlanDocument3 pagesTable of Contents Poultry Egg Farming Business PlanGustafaGovachefMotivatiNo ratings yet

- Documents-Nutrient Solution Formulation For Hydroponic (Perlite Rockwool NFT) Tomatoes in FloridaDocument11 pagesDocuments-Nutrient Solution Formulation For Hydroponic (Perlite Rockwool NFT) Tomatoes in FloridaFadhilah Suroto50% (2)

- 3.1.2 - Indigenous Relationships 24 - WebDocument26 pages3.1.2 - Indigenous Relationships 24 - WebMatthew Pringle100% (1)

- Agriculture: A Value Culture ForDocument12 pagesAgriculture: A Value Culture ForTin DanNo ratings yet

- Dairy Farming For Small FarmerDocument41 pagesDairy Farming For Small Farmersanu_ninjaNo ratings yet

- AG Dairy Farm Project PlanDocument11 pagesAG Dairy Farm Project Planvinay kumar0% (1)

- PiggeryDocument33 pagesPiggerySaurabh Sanand100% (1)

- Dairy Farming 1. Why Do Dairy Farming ?: Animal HusbandryDocument6 pagesDairy Farming 1. Why Do Dairy Farming ?: Animal HusbandryvishwaswarnaNo ratings yet

- Form 4 Agri Science Term 1 2020-2021 Handout 6 Week 9Document24 pagesForm 4 Agri Science Term 1 2020-2021 Handout 6 Week 9Ishmael Samuel 4Y ABCCNo ratings yet

- Angora Rabbit Farming GuideDocument17 pagesAngora Rabbit Farming GuideLEELAJA100% (2)

- Prepare Dairy Farm Project ProposalDocument11 pagesPrepare Dairy Farm Project ProposalAdonis Kum75% (20)

- Cattle PlanDocument39 pagesCattle PlanMariam SharifNo ratings yet

- Expanding A Dairy Business Affects Business Risk Financial RiskDocument4 pagesExpanding A Dairy Business Affects Business Risk Financial Riskjorgeortizramos1936No ratings yet

- EManual AGRI 1Document63 pagesEManual AGRI 1Kumar RajnishNo ratings yet

- 2022 Sheep Productions JV SouthDocument14 pages2022 Sheep Productions JV SouthCatatan Faizin 2No ratings yet

- IFRS Accounting for AgricultureDocument4 pagesIFRS Accounting for AgriculturebikilahussenNo ratings yet

- Pig FarmingDocument25 pagesPig Farmingসপ্তক মন্ডল100% (1)

- Analysis and Preparation of Financial Statement: Presented byDocument38 pagesAnalysis and Preparation of Financial Statement: Presented byDhruv PatelNo ratings yet

- Organizing farm expenses and incomeDocument75 pagesOrganizing farm expenses and incometinyikoNo ratings yet

- Agricultural Credit & Crop InsuranceDocument20 pagesAgricultural Credit & Crop InsuranceRupesh KandurwarNo ratings yet

- Credit Functions - Developmental and Promotional Functions - Supervisory FunctionsDocument32 pagesCredit Functions - Developmental and Promotional Functions - Supervisory FunctionscrajkumarsinghNo ratings yet

- Strawberry Profit$: - . - Profit Planning Tools For An Alberta Strawberry EnterpriseDocument4 pagesStrawberry Profit$: - . - Profit Planning Tools For An Alberta Strawberry EnterpriseZeki ZekijaNo ratings yet

- 2006 Michigan Dairy Farm Business AnalysDocument63 pages2006 Michigan Dairy Farm Business AnalysmekuanitNo ratings yet

- Sheep Farming GuideDocument26 pagesSheep Farming Guidemkumar116No ratings yet

- Project Proposal On The Establishment of Animal Feed Producing Plant in Gondar Zuriya Woreda Maksegnit TownDocument44 pagesProject Proposal On The Establishment of Animal Feed Producing Plant in Gondar Zuriya Woreda Maksegnit TownTesfaye Degefa100% (2)

- Broiler - Production - Management - 2017 Final PDFDocument36 pagesBroiler - Production - Management - 2017 Final PDFNAFUYE BRIANNo ratings yet

- Farm Business Dairy PlanDocument5 pagesFarm Business Dairy Planravi140177No ratings yet

- I. Production PlanDocument28 pagesI. Production PlanOmphile KgosiemangNo ratings yet

- Farmville PVT LTDDocument21 pagesFarmville PVT LTDHina MirNo ratings yet

- Balance Sheet: An Introduction To Basic Farm Financial StatementsDocument14 pagesBalance Sheet: An Introduction To Basic Farm Financial StatementsLuyinda KevinNo ratings yet

- Dairy Farm Project ReportDocument30 pagesDairy Farm Project ReportRiya Singh88% (17)

- Poultry Broiler FarmingDocument10 pagesPoultry Broiler FarmingVinod Kumar AsthanaNo ratings yet

- Steckler Mowing and ConditioningDocument12 pagesSteckler Mowing and ConditioningAaron StecklerNo ratings yet

- Chart of Accounts - ImpDocument11 pagesChart of Accounts - Impravirambo_pNo ratings yet

- Eco DairyDocument16 pagesEco DairyNilamdeen Mohamed ZamilNo ratings yet

- Whos A FarmerDocument6 pagesWhos A Farmertrevor cisneyNo ratings yet

- Comparing Land Use Options Tool Helps Farmers Evaluate AlternativesDocument3 pagesComparing Land Use Options Tool Helps Farmers Evaluate AlternativesAmranul HaqueNo ratings yet

- Building Business Success Hazelnut PlanningDocument10 pagesBuilding Business Success Hazelnut PlanningTo RteNo ratings yet

- Feasibility Study Egg Farm HermelDocument13 pagesFeasibility Study Egg Farm HermelSamuel FanijoNo ratings yet

- Generic Meat Plant Business PlanDocument34 pagesGeneric Meat Plant Business PlanSolid Work and Mechanical software TutorialNo ratings yet

- Offarm Labor and DebtDocument20 pagesOffarm Labor and Debthewan2008No ratings yet

- Oxford University Press Agricultural & Applied Economics AssociationDocument7 pagesOxford University Press Agricultural & Applied Economics AssociationmaribardNo ratings yet

- Account PresentationDocument11 pagesAccount PresentationAtul KhotNo ratings yet

- Jasons PDF RemediatedDocument4 pagesJasons PDF Remediatedsalah.rekani542No ratings yet

- A Local Cooperative's Financial and Strategic Analysis of The Evaluation of Potential Merger PartnersDocument18 pagesA Local Cooperative's Financial and Strategic Analysis of The Evaluation of Potential Merger PartnersChess NutsNo ratings yet

- Come Hell or High Water: IrrigationDocument4 pagesCome Hell or High Water: Irrigationapi-297281784No ratings yet

- Basics of financial record keeping for cow herd profitabilityDocument8 pagesBasics of financial record keeping for cow herd profitabilityJorge Ortiz RamosNo ratings yet

- Gibe Diary farm final final11Document28 pagesGibe Diary farm final final11shiferaw kumbiNo ratings yet

- Crop Residue TMR FeedDocument19 pagesCrop Residue TMR FeedRuel PerochoNo ratings yet

- Wilmar International Ltd. (WIL) : Executive SummaryDocument48 pagesWilmar International Ltd. (WIL) : Executive Summaryaimran_amirNo ratings yet

- The Chicken Millionaire's Handbook: What It Takes To Earn A Good Fortune From Chicken FarmingFrom EverandThe Chicken Millionaire's Handbook: What It Takes To Earn A Good Fortune From Chicken FarmingNo ratings yet

- Solar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitFrom EverandSolar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitNo ratings yet

- Food Outlook: Biannual Report on Global Food Markets May 2019From EverandFood Outlook: Biannual Report on Global Food Markets May 2019No ratings yet

- Summary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionFrom EverandSummary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionNo ratings yet

- Poultry Business Plan Sample Brick and Mortar Final Copy 1Document40 pagesPoultry Business Plan Sample Brick and Mortar Final Copy 1suelaNo ratings yet

- Aiba Company PresentationDocument20 pagesAiba Company PresentationsuelaNo ratings yet

- IndexDocument107 pagesIndexsuelaNo ratings yet

- Lse Che 2014Document88 pagesLse Che 2014suelaNo ratings yet

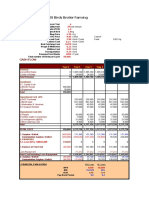

- Cash Flow For 50,000 Birds Broiler FarmingDocument1 pageCash Flow For 50,000 Birds Broiler FarmingsuelaNo ratings yet

- Final Report On Economic and Financial of The Poultry Farming in GambiaDocument21 pagesFinal Report On Economic and Financial of The Poultry Farming in GambiasuelaNo ratings yet

- WP 0465Document30 pagesWP 0465lemich0118No ratings yet

- The Effect of Depreciation of The Exchange Rate On Trade Balance of AlbaniaDocument19 pagesThe Effect of Depreciation of The Exchange Rate On Trade Balance of AlbaniasuelaNo ratings yet

- Poultry Breeding, Meat Processing and Trade - Business Plan For A New CompanyDocument59 pagesPoultry Breeding, Meat Processing and Trade - Business Plan For A New Companymetro hydraNo ratings yet

- The Role of Exchange Rates in International Trade Models: Does The Marshall-Lerner Condition Hold in Albania?Document56 pagesThe Role of Exchange Rates in International Trade Models: Does The Marshall-Lerner Condition Hold in Albania?suelaNo ratings yet

- Nertila FeruliDocument69 pagesNertila FerulisuelaNo ratings yet

- Business Plan For Establishing A Poultry Farm in Ni-Geria A General Overview For An EntrepreneurDocument37 pagesBusiness Plan For Establishing A Poultry Farm in Ni-Geria A General Overview For An Entrepreneurpradeep andraNo ratings yet

- Goose Breeding Project-EngDocument8 pagesGoose Breeding Project-EngSachin KuteNo ratings yet

- Real Exchange Rate Volatility and International Trade The Case of AlbaniaDocument9 pagesReal Exchange Rate Volatility and International Trade The Case of AlbaniasuelaNo ratings yet

- Effect of Depreciation of The Exchange Rate On TheDocument10 pagesEffect of Depreciation of The Exchange Rate On ThesuelaNo ratings yet

- Adriatic Sea Albania and Pottery TradeDocument1 pageAdriatic Sea Albania and Pottery TradesuelaNo ratings yet

- Effect of Depreciation of The Exchange Rate On TheDocument10 pagesEffect of Depreciation of The Exchange Rate On ThesuelaNo ratings yet

- 1989 NY Poultry Farm Business SummaryDocument30 pages1989 NY Poultry Farm Business SummarysuelaNo ratings yet

- Edoc - Tips - Free Poultry Business Plan PDF Poultry Farming PoultryDocument2 pagesEdoc - Tips - Free Poultry Business Plan PDF Poultry Farming PoultrysuelaNo ratings yet

- Pork Market Crisis in Romania: Pig Livestock, Pork Production, Consumption, Import, Export, Trade Balance and PriceDocument15 pagesPork Market Crisis in Romania: Pig Livestock, Pork Production, Consumption, Import, Export, Trade Balance and PricesuelaNo ratings yet

- Decision Tools For Family Poultry DeveloDocument123 pagesDecision Tools For Family Poultry DevelosuelaNo ratings yet

- Complete Poultry Farming Business Plan for 2,400 Layers FarmDocument8 pagesComplete Poultry Farming Business Plan for 2,400 Layers FarmAlina zainabNo ratings yet

- Digital Financial Capabilities and Household EntrepreneurshipDocument50 pagesDigital Financial Capabilities and Household EntrepreneurshipsuelaNo ratings yet

- The Central and Eastern European Online Library: SourceDocument19 pagesThe Central and Eastern European Online Library: SourcesuelaNo ratings yet

- Digital-Related Capabilities and Financial Performance: The Mediating Effect of Performance Measurement SystemsDocument15 pagesDigital-Related Capabilities and Financial Performance: The Mediating Effect of Performance Measurement SystemssuelaNo ratings yet

- Role of Financial Capabilities in Harnessing Digital Mobile Payments For Enterprise SuccessDocument2 pagesRole of Financial Capabilities in Harnessing Digital Mobile Payments For Enterprise SuccesssuelaNo ratings yet

- Poultry Development and Marketing EnterpriseDocument32 pagesPoultry Development and Marketing EnterpriseKassaye KA Arage100% (1)

- Evidence of Specified Work 1263Document4 pagesEvidence of Specified Work 1263Marie MicheauNo ratings yet

- The Rise of Amul - India's Iconic Dairy CooperativeDocument22 pagesThe Rise of Amul - India's Iconic Dairy Cooperativeamansrivastava007No ratings yet

- Slave NarrativesDocument195 pagesSlave NarrativesGutenberg.orgNo ratings yet

- 201109062010371.muestra 2º EsoDocument8 pages201109062010371.muestra 2º EsoMarta Charlin AlvarezNo ratings yet

- Khoe Peoples of S. AfricaDocument19 pagesKhoe Peoples of S. AfricaMichelleNo ratings yet

- 25472050Document52 pages25472050morgan8353No ratings yet

- Reviewer Meat Lesson 2Document10 pagesReviewer Meat Lesson 2Rose LynnNo ratings yet

- Developmental Economics School Farm ProposalDocument41 pagesDevelopmental Economics School Farm Proposalandrei4i2005100% (1)

- Agra ScriptDocument3 pagesAgra ScriptMark Hiro NakagawaNo ratings yet

- Trece Store Product Range-Bentz Jaz Indonesia Oct2023Document4 pagesTrece Store Product Range-Bentz Jaz Indonesia Oct2023Dickdoyo LanggengNo ratings yet

- Arjo DidessaDocument8 pagesArjo Didessaburqa100% (5)

- Cocoa Development Project of Belize: O. 1815 N. Lynn ST., Suite 200, Arlington, VA 22209 USA (703) 276-1800Document67 pagesCocoa Development Project of Belize: O. 1815 N. Lynn ST., Suite 200, Arlington, VA 22209 USA (703) 276-1800MBI TABENo ratings yet

- Investment - Project - Miepo 02 11 12 FinalDocument24 pagesInvestment - Project - Miepo 02 11 12 FinalOrganizația de Atragere a Investițiilor și Promovarea Exportului din MoldovaNo ratings yet

- Poultry Farm Checklist - E&LDocument6 pagesPoultry Farm Checklist - E&LMT CNo ratings yet

- Planets and Their Karakatwas (Significance)Document3 pagesPlanets and Their Karakatwas (Significance)Subramanya RaoNo ratings yet

- POS Training ModuleDocument81 pagesPOS Training Moduleshalini iyer0% (1)

- Fulvic Acid Minerals May Prevent Cancer GrowthDocument42 pagesFulvic Acid Minerals May Prevent Cancer Growthdarlene918No ratings yet

- MGT 489 ProjectDocument28 pagesMGT 489 ProjectBiplob ShathiNo ratings yet

- Organic Farmers and Farms of KeralaDocument16 pagesOrganic Farmers and Farms of KeralaNyah KingsleyNo ratings yet

- Yl4 Looking For The Dog UkDocument5 pagesYl4 Looking For The Dog UkSylwiaNo ratings yet

- History of Urbanization and Urban Planning in Western Countries and Indonesia - Nida Humaida (201456801)Document5 pagesHistory of Urbanization and Urban Planning in Western Countries and Indonesia - Nida Humaida (201456801)Nida HumaidaNo ratings yet

- Wagyu Breeders Handbook: An Introduction To WagyuDocument31 pagesWagyu Breeders Handbook: An Introduction To WagyuGermaine IsaacsonNo ratings yet

- 04 Management PGD 13jan08Document26 pages04 Management PGD 13jan08AnisaNo ratings yet

- Basicknifeskillsanddifferenttypesofvegetablecutting 171031042435Document43 pagesBasicknifeskillsanddifferenttypesofvegetablecutting 171031042435myratura50% (2)

- 1 Comparison of Short AdjectivesDocument2 pages1 Comparison of Short AdjectivesThy Vuong67% (3)