You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- General Journal, Joannamarie Uy ProblemDocument4 pagesGeneral Journal, Joannamarie Uy ProblemFeiya Liu100% (6)

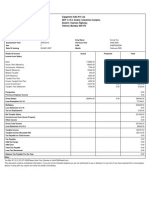

- Amit Dec 2020 PayslipDocument1 pageAmit Dec 2020 PayslipAmit GhangasNo ratings yet

- Solved Stan Rented An Office Building To Clay For 3 000 PerDocument1 pageSolved Stan Rented An Office Building To Clay For 3 000 PerAnbu jaromiaNo ratings yet

- Ghosh Engineering Corporation: Proforma InvoiceDocument1 pageGhosh Engineering Corporation: Proforma InvoiceKABIR CHOPRANo ratings yet

- Sanitiser Tax InvoiceDocument1 pageSanitiser Tax InvoiceSanjeev RanjanNo ratings yet

- Asifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-11 PDFDocument11 pagesAsifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-11 PDFaemanNo ratings yet

- GST TaxDocument1 pageGST Taxandreatorres10082001No ratings yet

- Krrish Price ListDocument5 pagesKrrish Price ListPriyankar MathuriaNo ratings yet

- 2 Topic2 Residence StatusDocument19 pages2 Topic2 Residence StatusIskandar Zulkarnain KamalluddinNo ratings yet

- 1701 Annual Income Tax Return: (From Part VI Item 5) (From Part VII Item 10)Document5 pages1701 Annual Income Tax Return: (From Part VI Item 5) (From Part VII Item 10)Jennylyn TagubaNo ratings yet

- PAYSLIP JanDocument2 pagesPAYSLIP JanPaddu KingNo ratings yet

- Kerala Gazette: ExtraordinaryDocument2 pagesKerala Gazette: ExtraordinaryArjun Manghav PuthanpurayilNo ratings yet

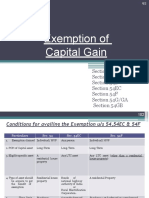

- Unit 3 Capital Gain ExemptionsDocument9 pagesUnit 3 Capital Gain ExemptionsAnshu kumarNo ratings yet

- Constitutional Provisions Relating To TaxDocument9 pagesConstitutional Provisions Relating To Taxrakshitha9reddy-1No ratings yet

- 2010 ADSO As DGPA Tax ReturnDocument17 pages2010 ADSO As DGPA Tax ReturnDentist The MenaceNo ratings yet

- Withholding Tax (Eng)Document10 pagesWithholding Tax (Eng)WN TV programsNo ratings yet

- Blank 5Document1 pageBlank 5Abbas RizviNo ratings yet

- 2223TPG0008838Document1 page2223TPG0008838Huskee CokNo ratings yet

- Tributaria e Aduaneira Declaracao de Rendimentos IRS Modelo 3 Contrato Saphal LamaDocument6 pagesTributaria e Aduaneira Declaracao de Rendimentos IRS Modelo 3 Contrato Saphal LamasitalghimireNo ratings yet

- Nigerian PAYE Calculator 4.0Document2 pagesNigerian PAYE Calculator 4.0obumuyaemesi100% (1)

- GST Invoice Format PDFDocument1 pageGST Invoice Format PDFAnanya NairNo ratings yet

- BIR Form 2307Document1 pageBIR Form 2307Aizhel Villegas ArcipeNo ratings yet

- Employee Payroll - Apex Accounting - Liam Doyle - Employee PayrollDocument1 pageEmployee Payroll - Apex Accounting - Liam Doyle - Employee Payrollapi-590120200No ratings yet

- Incometaxstatement2009 2010Document2 pagesIncometaxstatement2009 2010api-3725541No ratings yet

- Credit 243112012575 12 2023Document2 pagesCredit 243112012575 12 2023bhawesh joshiNo ratings yet

- Solved The President and Vice President of Usa Corporation Receive BenefitsDocument1 pageSolved The President and Vice President of Usa Corporation Receive BenefitsAnbu jaromiaNo ratings yet

- Annex (A1)Document1 pageAnnex (A1)Jana Jonathan0% (1)

- 2 Pdfsam Datey Customs ActDocument1 page2 Pdfsam Datey Customs ActdskrishnaNo ratings yet

- In Voice 8077122617129115647Document2 pagesIn Voice 8077122617129115647Vibrant PixelsNo ratings yet

- Income Tax Payment Challan: PSID #: 138638394Document1 pageIncome Tax Payment Challan: PSID #: 138638394naeem1990No ratings yet