You might also like

- Logical ProblemsDocument14 pagesLogical ProblemskaedelarosaNo ratings yet

- Logical ProblemsDocument14 pagesLogical ProblemskaedelarosaNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- The NEC4 Engineering and Construction Contract: A CommentaryFrom EverandThe NEC4 Engineering and Construction Contract: A CommentaryNo ratings yet

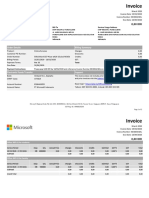

- Invoiceoffice 365Document2 pagesInvoiceoffice 365Muhammad Irfan Ilyas AssagafNo ratings yet

- Employment Claims without a Lawyer: A Handbook for Litigants in Person, Revised 2nd editionFrom EverandEmployment Claims without a Lawyer: A Handbook for Litigants in Person, Revised 2nd editionNo ratings yet

- Answer Key Tax 501 by AmponganDocument41 pagesAnswer Key Tax 501 by AmponganHarriet Caryn Albaño57% (21)

- Litigation Services Handbook: The Role of the Financial ExpertFrom EverandLitigation Services Handbook: The Role of the Financial ExpertNo ratings yet

- The Real Estate Rehab Investing Bible: A Proven-Profit System for Finding, Funding, Fixing, and Flipping Houses...Without Lifting a PaintbrushFrom EverandThe Real Estate Rehab Investing Bible: A Proven-Profit System for Finding, Funding, Fixing, and Flipping Houses...Without Lifting a PaintbrushRating: 5 out of 5 stars5/5 (1)

- Schneiderman v. The Trump Entrepreneur Initiative LLC Complaint OCRDocument39 pagesSchneiderman v. The Trump Entrepreneur Initiative LLC Complaint OCRLaw&CrimeNo ratings yet

- Clarke, Silva, & Thorley 2012 - Risk Parity, Maximum Diversification and Minimum Variance - An Analytic PerspectiveDocument15 pagesClarke, Silva, & Thorley 2012 - Risk Parity, Maximum Diversification and Minimum Variance - An Analytic Perspectivegchagas6019No ratings yet

- Accounting (PT - Financial Assets)Document66 pagesAccounting (PT - Financial Assets)Micko Lagundino33% (3)

- Deductions From Gross Estate: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersDocument9 pagesDeductions From Gross Estate: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersJEPZ LEDUNANo ratings yet

- Deductions From Gross Estate: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersDocument9 pagesDeductions From Gross Estate: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersGhatz CondaNo ratings yet

- Chapter 4 - Deductions From Gross Estate2013Document9 pagesChapter 4 - Deductions From Gross Estate2013incubus_yeah90% (10)

- Chapter 4 - Deductions From Gross Estate2013Document9 pagesChapter 4 - Deductions From Gross Estate2013Rozel Joy Labasano100% (1)

- Chapt 4 Gross IncomeDocument8 pagesChapt 4 Gross IncomeJhon Mark VillonNo ratings yet

- Chapter 2 - Transfer Taxes and Basic SuccessionDocument6 pagesChapter 2 - Transfer Taxes and Basic SuccessionKatrina AngelicaNo ratings yet

- Taxestate TaxDocument9 pagesTaxestate TaxEngel Racraquin Bristol0% (1)

- Chapter 6 - Donor's TaxDocument12 pagesChapter 6 - Donor's TaxCai0450% (2)

- Chapter 6 - Donor S Tax2013Document12 pagesChapter 6 - Donor S Tax2013incubus_yeah100% (8)

- Chapter 2 - Transfer Taxes and Basic Succession2013Document6 pagesChapter 2 - Transfer Taxes and Basic Succession2013iamjan_10150% (4)

- Chapter 5 - Estate TaxDocument11 pagesChapter 5 - Estate TaxMargery Bumagat100% (1)

- Chapter 5 - Estate Tax2013Document12 pagesChapter 5 - Estate Tax2013Anjo Ellis100% (2)

- Transfer Taxes and Basic Succession: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersDocument7 pagesTransfer Taxes and Basic Succession: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersChristine VinasNo ratings yet

- Chapter 6 Donor S TaxDocument9 pagesChapter 6 Donor S Taxkatniss0013No ratings yet

- Exclusion From Gross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersDocument5 pagesExclusion From Gross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersShynEdwardNo ratings yet

- Chapt-5 Exclude From Gross IncomeDocument4 pagesChapt-5 Exclude From Gross IncomehumnarviosNo ratings yet

- Chap 3 Concepts of Income2013Document8 pagesChap 3 Concepts of Income2013Quennie Jane Siblos100% (1)

- Income Tax of Individuals: Income Taxation 5Th Edition (By: Valencia & Roxas)Document10 pagesIncome Tax of Individuals: Income Taxation 5Th Edition (By: Valencia & Roxas)Aiden PatsNo ratings yet

- Chapt-11 Income Tax - IndividualsDocument10 pagesChapt-11 Income Tax - Individualshumnarvios100% (4)

- Chapt 11+Income+Tax+ +individuals2013fDocument13 pagesChapt 11+Income+Tax+ +individuals2013fiamjan_10180% (15)

- Chapt-7 Dealings in PropDocument14 pagesChapt-7 Dealings in Prophumnarvios0% (1)

- Ch4 - Gross IncomeDocument12 pagesCh4 - Gross IncomeJuan FrivaldoNo ratings yet

- MarkDocument9 pagesMarkMark Joseph D. LausNo ratings yet

- Chapter 3 - Gross Estate2013Document8 pagesChapter 3 - Gross Estate2013rayjoshua12No ratings yet

- Gross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersDocument7 pagesGross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersAnonymous qpUaTkNo ratings yet

- Chapt 14+Income+Taxes+ +estates+ 26+trusts2013fDocument11 pagesChapt 14+Income+Taxes+ +estates+ 26+trusts2013fLouie De La Torre100% (1)

- Ultimate Accounting TestDocument89 pagesUltimate Accounting TestKen ZafraNo ratings yet

- Chapt-3 Concepts of IncomeDocument4 pagesChapt-3 Concepts of Incomehumnarvios50% (2)

- Income Taxes of Estates & Trusts: Income Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersDocument13 pagesIncome Taxes of Estates & Trusts: Income Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersJane Mae CruzNo ratings yet

- Answer Key Tax 501 by AmponganDocument37 pagesAnswer Key Tax 501 by AmponganRegina Dela RosaNo ratings yet

- Chapter 3 - Gross EstateDocument6 pagesChapter 3 - Gross EstateKatrina AngelicaNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- J.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnNo ratings yet

- J.K. Lasser's Your Income Tax 2024, Professional EditionFrom EverandJ.K. Lasser's Your Income Tax 2024, Professional EditionNo ratings yet

- Tax Planning and Compliance for Tax-Exempt Organizations: Rules, Checklists, ProceduresFrom EverandTax Planning and Compliance for Tax-Exempt Organizations: Rules, Checklists, ProceduresNo ratings yet

- Digital Wealth: An Automatic Way to Invest SuccessfullyFrom EverandDigital Wealth: An Automatic Way to Invest SuccessfullyRating: 4.5 out of 5 stars4.5/5 (3)

- Property & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsFrom EverandProperty & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsNo ratings yet

- Retirement Income for Life: Getting More without Saving More (Third Edition)From EverandRetirement Income for Life: Getting More without Saving More (Third Edition)No ratings yet

- J.K. Lasser's Your Income Tax 2019: For Preparing Your 2018 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2019: For Preparing Your 2018 Tax ReturnNo ratings yet

- Managing Concentrated Stock Wealth: An Advisor's Guide to Building Customized SolutionsFrom EverandManaging Concentrated Stock Wealth: An Advisor's Guide to Building Customized SolutionsNo ratings yet

- Private Client Practice: An Expert Guide, 2nd editionFrom EverandPrivate Client Practice: An Expert Guide, 2nd editionNo ratings yet

- To Whomsoever It May ConcernDocument6 pagesTo Whomsoever It May ConcernkaedelarosaNo ratings yet

- Cambridge University: "Creditum Est Excellentia"Document1 pageCambridge University: "Creditum Est Excellentia"kaedelarosaNo ratings yet

- Narrative Reports: Elise's Learner Narrative: "I Like Reading, But I Don't Like Chatter."Document7 pagesNarrative Reports: Elise's Learner Narrative: "I Like Reading, But I Don't Like Chatter."kaedelarosaNo ratings yet

- Comparative AnalysisDocument3 pagesComparative AnalysiskaedelarosaNo ratings yet

- (Read and Understand. Do Not Just Print) : On Love Kahlil GibranDocument2 pages(Read and Understand. Do Not Just Print) : On Love Kahlil GibrankaedelarosaNo ratings yet

- Ten Years Have Passed Since The Fall of TroyDocument10 pagesTen Years Have Passed Since The Fall of TroykaedelarosaNo ratings yet

- Prep Time Cook Time Total Time: How To Prepare Shrimp For Shrimp TempuraDocument10 pagesPrep Time Cook Time Total Time: How To Prepare Shrimp For Shrimp TempurakaedelarosaNo ratings yet

- Western CuisineDocument2 pagesWestern CuisinekaedelarosaNo ratings yet

- BIBIMBAP (Korean Mixed Rice With Meat and Assorted Vegetables)Document14 pagesBIBIMBAP (Korean Mixed Rice With Meat and Assorted Vegetables)kaedelarosaNo ratings yet

- Analects of Confucius SimplifiedDocument1 pageAnalects of Confucius SimplifiedkaedelarosaNo ratings yet

- Johnice Dhane E. de La Rosa: #23 Magallanes St. Tuguegarao City, Cagayan 0936295093Document4 pagesJohnice Dhane E. de La Rosa: #23 Magallanes St. Tuguegarao City, Cagayan 0936295093kaedelarosaNo ratings yet

- Mahatma Gandhi: South Africa Apartheid Injustice of Racial SegregationDocument19 pagesMahatma Gandhi: South Africa Apartheid Injustice of Racial SegregationkaedelarosaNo ratings yet

- BSPDocument1 pageBSPkaedelarosaNo ratings yet

- CsuDocument2 pagesCsukaedelarosaNo ratings yet

- University of Saint Louis Tuguegarao School of Business Administration and AccountancyDocument2 pagesUniversity of Saint Louis Tuguegarao School of Business Administration and AccountancykaedelarosaNo ratings yet

- Aves Means BirdsDocument3 pagesAves Means BirdskaedelarosaNo ratings yet

- Production Capacity and ForecastDocument1 pageProduction Capacity and ForecastkaedelarosaNo ratings yet

- Using Candlestick Charts To Improve Profitability: Presented by Vema RTDocument17 pagesUsing Candlestick Charts To Improve Profitability: Presented by Vema RTVema Reddy TungaNo ratings yet

- A Project Report On Financial Performance Evaluation With Key Ratios at Vasavadatta Cement Kesoram Industries LTD Sedam Gulbarga PDFDocument82 pagesA Project Report On Financial Performance Evaluation With Key Ratios at Vasavadatta Cement Kesoram Industries LTD Sedam Gulbarga PDFK Sagar Kondolla100% (1)

- Full - Statement - Account 70510046895Document3 pagesFull - Statement - Account 70510046895Lameck SwaloNo ratings yet

- Interview Capsule For CUB ExecutivesDocument169 pagesInterview Capsule For CUB Executivesvenkatesh pkNo ratings yet

- India International ExchangeDocument1 pageIndia International ExchangeSugan Pragasam100% (1)

- Pei 135 - Pei300Document13 pagesPei 135 - Pei300Anonymous Rwa38rT8GVNo ratings yet

- Pakistan Mergers and Acquisitions PDFDocument10 pagesPakistan Mergers and Acquisitions PDFadeelarustamNo ratings yet

- Yalgaar Eco Mid SD SD Mrunal-Sir CompressedDocument185 pagesYalgaar Eco Mid SD SD Mrunal-Sir CompressedAbhishek RaiNo ratings yet

- MBA Assignment QuestionDocument4 pagesMBA Assignment QuestionPoorna SethuramanNo ratings yet

- CH 4 Zakat and Tax PlanningDocument48 pagesCH 4 Zakat and Tax Planningabdihakimmohamed628No ratings yet

- Practice Questions Lecture 4-6Document5 pagesPractice Questions Lecture 4-6Komi ChNo ratings yet

- EPF ESIC and PT Calculation Below and Above 15000 PAY SLIPDocument7 pagesEPF ESIC and PT Calculation Below and Above 15000 PAY SLIPchan_thong_1No ratings yet

- A Study On Mergers and Acquisitions of Indian Banking SectorDocument9 pagesA Study On Mergers and Acquisitions of Indian Banking SectorEditor IJTSRDNo ratings yet

- GE403 Engineering Economy First Semester 1443HDocument42 pagesGE403 Engineering Economy First Semester 1443HnorahNo ratings yet

- Suntec ReitDocument398 pagesSuntec ReitGymmy YeoNo ratings yet

- Business Combination Final ExamDocument9 pagesBusiness Combination Final Examcharlene lizardoNo ratings yet

- 9706 s09 Ms 21,22Document13 pages9706 s09 Ms 21,22roukaiya_peerkhan100% (1)

- AHTM 2007 - OpenDoors - PKDocument9 pagesAHTM 2007 - OpenDoors - PKWaleed KhalidNo ratings yet

- Tle ModuleDocument3 pagesTle ModuleThalia ManzanillaNo ratings yet

- Kota Fibers LTDDocument18 pagesKota Fibers LTDpdxjayNo ratings yet

- Dabur India LTD.: Equity Research ReportDocument40 pagesDabur India LTD.: Equity Research ReportshakeDNo ratings yet

- Sebi AifDocument11 pagesSebi AifsarasmuzumdarNo ratings yet

- Accounting Explained With Brief History and Modern Job RequirementsDocument10 pagesAccounting Explained With Brief History and Modern Job RequirementsDarlen Jazztin ReyesNo ratings yet

- Vilfredo Pareto: An Intellectual Biography: The Illusions and Disillusions OF LIBERTY (1891-1898)Document322 pagesVilfredo Pareto: An Intellectual Biography: The Illusions and Disillusions OF LIBERTY (1891-1898)Ibrahim Ben IaqobNo ratings yet

- OpTransactionHistoryUX320 12 2023Document41 pagesOpTransactionHistoryUX320 12 2023Jamnas JamaludheenNo ratings yet

- (Resume Suit) Creative Resume With Self-Recommendation 11Document3 pages(Resume Suit) Creative Resume With Self-Recommendation 11প্রমিত সরকারNo ratings yet