You might also like

- Filmore EnterprisesDocument7 pagesFilmore EnterprisesJoshua Everett100% (1)

- 2023 CFA LIII MockExamA-PMDocument23 pages2023 CFA LIII MockExamA-PMHugo VALERIO100% (1)

- Assignment 1 - Investment AnalysisDocument5 pagesAssignment 1 - Investment Analysisphillimon zuluNo ratings yet

- FINA 410 - Exercises (NOV)Document7 pagesFINA 410 - Exercises (NOV)said100% (1)

- Appendix B Solutions To Concept ChecksDocument31 pagesAppendix B Solutions To Concept Checkshellochinp100% (1)

- JUN18L1EQU/C01 Review QuestionsDocument3 pagesJUN18L1EQU/C01 Review QuestionsjuanNo ratings yet

- Integrated Case Merril Finch IncDocument10 pagesIntegrated Case Merril Finch IncEmman DtrtNo ratings yet

- Portfolio Variance 0.103Document4 pagesPortfolio Variance 0.103sidhant_nageliaNo ratings yet

- Communique - May 2010Document4 pagesCommunique - May 2010Pallavi YadalamNo ratings yet

- Assignment 1 - Investment AnalysisDocument5 pagesAssignment 1 - Investment Analysisphillimon zuluNo ratings yet

- IM 02 (Risk Return) 1Document54 pagesIM 02 (Risk Return) 1Niaz MorshedNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main ViewDocument47 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main ViewKazi FahimNo ratings yet

- Chapter 3Document73 pagesChapter 3Mark Arceo0% (1)

- FM 8th Edition Chapter 12 - Risk and ReturnDocument20 pagesFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoNo ratings yet

- FINS1612 Tutorial 4 - Investors in The Share MarketDocument10 pagesFINS1612 Tutorial 4 - Investors in The Share MarketRuben CollinsNo ratings yet

- Ans Question Bank Lv2Document36 pagesAns Question Bank Lv2Hiếu Nhi TrịnhNo ratings yet

- Revision Set 5 AnswerDocument8 pagesRevision Set 5 AnswerKian TuckNo ratings yet

- Solution To Points 1 - Escrow Accounts - Earn-Outs - Contingent Value Rights (CVRS)Document4 pagesSolution To Points 1 - Escrow Accounts - Earn-Outs - Contingent Value Rights (CVRS)fabriNo ratings yet

- Risk & Return: Page 1 of 5Document5 pagesRisk & Return: Page 1 of 5Saqib AliNo ratings yet

- Beta Coefficient and CAPM ModelDocument13 pagesBeta Coefficient and CAPM ModelMishal ArifNo ratings yet

- CHAPTER 08—RISK AND RATES OF RETURN Multiple Choice: ConceptualDocument6 pagesCHAPTER 08—RISK AND RATES OF RETURN Multiple Choice: ConceptualDavid LarryNo ratings yet

- ADocument2 pagesAPrincess BanquilNo ratings yet

- RB Answers CH13Document4 pagesRB Answers CH13Nayden GeorgievNo ratings yet

- Assignment 2Document2 pagesAssignment 2Aqsha NaufaldyNo ratings yet

- Risk and Return (Part II)Document22 pagesRisk and Return (Part II)mimiNo ratings yet

- Su 2023 Practice Problems Risk&ReturnDocument2 pagesSu 2023 Practice Problems Risk&Returnnishatur.rahman01No ratings yet

- Assignment Bond Equity Portfolio Management Strategies Chapter 8 Update 18.12.2022Document11 pagesAssignment Bond Equity Portfolio Management Strategies Chapter 8 Update 18.12.2022Tya FauzieNo ratings yet

- Corporate Finance Sample Exam 2A Dr. A. Frank ThompsonDocument6 pagesCorporate Finance Sample Exam 2A Dr. A. Frank Thompsonabed kayaliNo ratings yet

- FINA 410 - Exercises: Estimating the Beta and Capitalizing ExpendituresDocument7 pagesFINA 410 - Exercises: Estimating the Beta and Capitalizing ExpendituresDrSwati BhargavaNo ratings yet

- Case StudyDocument6 pagesCase StudyWelshfyn ConstantinoNo ratings yet

- Tutorial 5 QuestionsDocument3 pagesTutorial 5 QuestionshrfjbjrfrfNo ratings yet

- KRDTop100SFM PDFDocument215 pagesKRDTop100SFM PDFNag Sai NarahariNo ratings yet

- VC Lexicon Anti-Dilution Protection (Also Known As Anti-Dilution Provisions) : in The Event of A Down-RoundDocument6 pagesVC Lexicon Anti-Dilution Protection (Also Known As Anti-Dilution Provisions) : in The Event of A Down-RoundRaymond RodisNo ratings yet

- Paper - 2: Strategic Financial Management Questions Security ValuationDocument21 pagesPaper - 2: Strategic Financial Management Questions Security Valuationsam kapoorNo ratings yet

- 3017 Tutorial 11Document2 pages3017 Tutorial 11rosea267No ratings yet

- Beta Management's Strategy Change and Stock SelectionDocument15 pagesBeta Management's Strategy Change and Stock Selectionsuperwinnie1No ratings yet

- Paper - 2: Strategic Financial Management Questions Security ValuationDocument21 pagesPaper - 2: Strategic Financial Management Questions Security ValuationRITZ BROWNNo ratings yet

- Mutual Funds and Other Investment Companies: Session 5Document43 pagesMutual Funds and Other Investment Companies: Session 5Niyanthesh ReddyNo ratings yet

- Financial Management (8513) STEDocument7 pagesFinancial Management (8513) STEmuhammad yousafNo ratings yet

- Soal Asis 4 IPMDocument2 pagesSoal Asis 4 IPMPutri Dianasri ButarbutarNo ratings yet

- Beta CoefficientDocument3 pagesBeta CoefficientNahidul Islam IU100% (1)

- IIMC Corp Finance 2018-19Document54 pagesIIMC Corp Finance 2018-19Ambuj AgrawalNo ratings yet

- Financial Management - Theory & Practice by Brigham-266-273Document8 pagesFinancial Management - Theory & Practice by Brigham-266-273Muhammad AzeemNo ratings yet

- Private EquityDocument49 pagesPrivate EquityDavi SáNo ratings yet

- JUN18L1EQU/C01: Accurate About The Index?Document3 pagesJUN18L1EQU/C01: Accurate About The Index?rafav10No ratings yet

- Bionic Turtle FRM Practice Questions P1.T3. Financial Markets and Products Chapter 3. Fund ManagementDocument9 pagesBionic Turtle FRM Practice Questions P1.T3. Financial Markets and Products Chapter 3. Fund ManagementChristian Rey Magtibay100% (1)

- 2015 Ci Harbour F ClassDocument3 pages2015 Ci Harbour F ClassMarcelo MedeirosNo ratings yet

- Risk and Return AssignmentDocument2 pagesRisk and Return AssignmentHuzaifa Bin SaeedNo ratings yet

- Bkm9e Answers Chap004Document6 pagesBkm9e Answers Chap004AhmadYaseenNo ratings yet

- Alpha/Beta Separation: Getting What You Pay ForDocument15 pagesAlpha/Beta Separation: Getting What You Pay Forilham100% (1)

- Fm-May-June 2015Document18 pagesFm-May-June 2015banglauserNo ratings yet

- HW5 SolnDocument7 pagesHW5 SolnZhaohui Chen100% (1)

- Invesco WilderHill Clean Energy ETF Document SummaryDocument2 pagesInvesco WilderHill Clean Energy ETF Document SummaryRahul SalveNo ratings yet

- CH 02 Mini CaseDocument18 pagesCH 02 Mini CaseCuong LeNo ratings yet

- Kuis - Financial Lab ModelingDocument2 pagesKuis - Financial Lab Modelingalexandersur9No ratings yet

- Nanyang Business School AB1201 Financial Management Tutorial 5: Risk and Rates of Return (Common Questions)Document3 pagesNanyang Business School AB1201 Financial Management Tutorial 5: Risk and Rates of Return (Common Questions)asdsadsaNo ratings yet

- MBA711 - Chapter 9 - Answers To All ProblemsDocument19 pagesMBA711 - Chapter 9 - Answers To All ProblemsOoi Kenn50% (2)

- Triple Trouble2 (Mar09)Document10 pagesTriple Trouble2 (Mar09)Jolin MajminNo ratings yet

- Economics of The AirlinesDocument40 pagesEconomics of The AirlinesAdriel M.No ratings yet

- Consumer and Firm Behavior: The Work-Leisure Decision and Profit MaximizationDocument22 pagesConsumer and Firm Behavior: The Work-Leisure Decision and Profit MaximizationRachit BhagatNo ratings yet

- Supply Chain Analysis of Ambuja CementDocument42 pagesSupply Chain Analysis of Ambuja Cementpallavc100% (1)

- Barclays Case Study.Document2 pagesBarclays Case Study.ReemaNo ratings yet

- 25-RBA (Responsible Business Alliance) Member - LenovoDocument3 pages25-RBA (Responsible Business Alliance) Member - LenovoHernani BergamoNo ratings yet

- Prasad CVDocument2 pagesPrasad CVLikitha LavanyaNo ratings yet

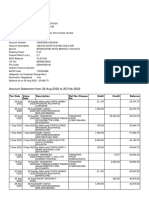

- Bank StatementDocument5 pagesBank StatementSANJIB GHOSHNo ratings yet

- Ba'Aad Wayn General Hospital: UNICEF Somalia Support Centre P.O. Box 44145-00100 Nairobi, KenyaDocument1 pageBa'Aad Wayn General Hospital: UNICEF Somalia Support Centre P.O. Box 44145-00100 Nairobi, KenyaEng abdallah HajiNo ratings yet

- Acct Statement XX2169 01102022Document22 pagesAcct Statement XX2169 01102022saurabh92prasadNo ratings yet

- Company Profile - Tri-Wall IndiaDocument35 pagesCompany Profile - Tri-Wall IndiaPrateek Singh SengarNo ratings yet

- Analysts See Upside in These Stocks Like Netflix & TeslaDocument14 pagesAnalysts See Upside in These Stocks Like Netflix & TeslaBenjamin ChongNo ratings yet

- Course Code Course Name Lecturer Assignment TitleDocument11 pagesCourse Code Course Name Lecturer Assignment TitleMuhd ArifNo ratings yet

- Legal Ethics Cases Week 1Document128 pagesLegal Ethics Cases Week 1CJ MelNo ratings yet

- Eg Gypsam - Final11.7Document22 pagesEg Gypsam - Final11.7সুন্দর মনNo ratings yet

- HSL Techno Edge: Retail ResearchDocument3 pagesHSL Techno Edge: Retail ResearchDinesh ChoudharyNo ratings yet

- Bilderberg Report 1955Document12 pagesBilderberg Report 1955xlastexitNo ratings yet

- Response To Child Support Modification and Retroactive Pay.Document7 pagesResponse To Child Support Modification and Retroactive Pay.Lindsay OlahNo ratings yet

- GDPR data breach notification guidelinesDocument32 pagesGDPR data breach notification guidelinesraulxNo ratings yet

- Trade AgreementDocument6 pagesTrade AgreementFRANCIS EDWIN MOJADONo ratings yet

- Shrimp Farming in Pakistan Urdu GuideDocument17 pagesShrimp Farming in Pakistan Urdu GuidesohailauhNo ratings yet

- Self-Asse Ssment QuestionnaireDocument3 pagesSelf-Asse Ssment QuestionnaireTam Le MinhNo ratings yet

- Zudio Marketing PlanDocument2 pagesZudio Marketing PlanAmir KhanNo ratings yet

- Swot of AbinbevDocument3 pagesSwot of AbinbevSanjeev Kumar SharmaNo ratings yet

- Ap8501, Ap8502, Ap8503 Audit of ShareholdersDocument21 pagesAp8501, Ap8502, Ap8503 Audit of ShareholdersRits Monte100% (1)

- Digitalgyanweb20 Blogspot Com PDFDocument8 pagesDigitalgyanweb20 Blogspot Com PDFNirmaan SinghNo ratings yet

- Ifr-Apc 311Document8 pagesIfr-Apc 311hkndarshanaNo ratings yet

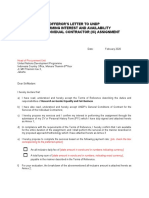

- Offeror'S Letter To Undp Confirming Interest and Availability For The Individual Contractor (Ic) AssignmentDocument4 pagesOfferor'S Letter To Undp Confirming Interest and Availability For The Individual Contractor (Ic) Assignmentori hasmantoNo ratings yet

- E Waste Management and Recycling Mechanism in Japan Sugimoto San PDFDocument17 pagesE Waste Management and Recycling Mechanism in Japan Sugimoto San PDFRizwan ShaikhNo ratings yet

- Adani Ports Financial RatiosDocument2 pagesAdani Ports Financial RatiosTaksh DhamiNo ratings yet

- Swifts Cable TrayDocument148 pagesSwifts Cable TrayMichael Bou KarimNo ratings yet