You might also like

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- Office of The Court Administrator v. TormisDocument20 pagesOffice of The Court Administrator v. TormiservingabralagbonNo ratings yet

- Ethics - FINALS - Additional CasesDocument12 pagesEthics - FINALS - Additional CaseservingabralagbonNo ratings yet

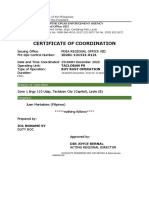

- Certificate of Coordination: Area(s) of OperationDocument3 pagesCertificate of Coordination: Area(s) of OperationervingabralagbonNo ratings yet

- Legal & Judicial Ethics & Practical Exercises SyllabusDocument8 pagesLegal & Judicial Ethics & Practical Exercises Syllabuservingabralagbon100% (1)

- Last Will TestamentDocument3 pagesLast Will TestamentIELTS75% (4)

- Certificate of Inventory Tacloban CityDocument2 pagesCertificate of Inventory Tacloban CityervingabralagbonNo ratings yet

- People Vs MarbabiesDocument3 pagesPeople Vs MarbabieservingabralagbonNo ratings yet

- Office of The Court Administrator V.Document21 pagesOffice of The Court Administrator V.ervingabralagbonNo ratings yet

- A. Plumptre v. RiveraDocument6 pagesA. Plumptre v. RiveraervingabralagbonNo ratings yet

- Caronan v. CaronanDocument8 pagesCaronan v. Caronancarla_cariaga_2No ratings yet

- D. Villahermosa v. Caracol, A.C. No. 7325, Jan. 21, 2015Document6 pagesD. Villahermosa v. Caracol, A.C. No. 7325, Jan. 21, 2015TrudgeOnNo ratings yet

- Aguirre vs. Rana PDFDocument7 pagesAguirre vs. Rana PDFCazzandhra BullecerNo ratings yet

- 2015 Yu - Kimteng - v. - Young20190320 5466 1y9r6ix PDFDocument13 pages2015 Yu - Kimteng - v. - Young20190320 5466 1y9r6ix PDFShiurabelle ApuraNo ratings yet

- 02-13. Catimbuhan V CruzDocument5 pages02-13. Catimbuhan V CruzOdette JumaoasNo ratings yet

- 8 Zafra III V PagatpatanDocument5 pages8 Zafra III V PagatpatanJinnelyn LiNo ratings yet

- Complainants vs. vs. Respondents: Second DivisionDocument6 pagesComplainants vs. vs. Respondents: Second DivisionervingabralagbonNo ratings yet

- Court Suspends Lawyer for 5 Years and Imposes Fine for Repeated Disobedience of Court OrdersDocument4 pagesCourt Suspends Lawyer for 5 Years and Imposes Fine for Repeated Disobedience of Court OrderservingabralagbonNo ratings yet

- in - Re - Order - Dated - October - 27 - 2016 - Issued - By20201127-9-123x8ouDocument5 pagesin - Re - Order - Dated - October - 27 - 2016 - Issued - By20201127-9-123x8ouervingabralagbonNo ratings yet

- Attorney Disbarred for Deceiving and Impregnating Young WomanDocument8 pagesAttorney Disbarred for Deceiving and Impregnating Young WomanDuffy DuffyNo ratings yet

- In Re Benjamin DacanayDocument4 pagesIn Re Benjamin Dacanayjeesup9No ratings yet

- AA - Total - Learning - Center - For - Young - Achievers20200916-9-1hx1arfDocument8 pagesAA - Total - Learning - Center - For - Young - Achievers20200916-9-1hx1arfervingabralagbonNo ratings yet

- 46 Gaw Jr. v. Commissioner of Internal Revenue20210428-11-1x0n8q5Document16 pages46 Gaw Jr. v. Commissioner of Internal Revenue20210428-11-1x0n8q5ervingabralagbonNo ratings yet

- 45 Commissioner of Internal Revenue v. La Flor20210505-11-RpbhzrDocument11 pages45 Commissioner of Internal Revenue v. La Flor20210505-11-RpbhzrervingabralagbonNo ratings yet

- 46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)Document9 pages46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)ervingabralagbonNo ratings yet

- 157 Adelfa - Properties - Inc. - v. - MendozaDocument7 pages157 Adelfa - Properties - Inc. - v. - MendozaKevin DegamoNo ratings yet

- Third Division: Notice NoticeDocument3 pagesThird Division: Notice NoticeervingabralagbonNo ratings yet

- 42 Allied Banking Corporation v. Commissioner Of20210505-12-Fno6kpDocument10 pages42 Allied Banking Corporation v. Commissioner Of20210505-12-Fno6kpervingabralagbonNo ratings yet

- 44 Commissioner - of - Internal - Revenue - v. - Univation20210505-11-1a1tm6xDocument10 pages44 Commissioner - of - Internal - Revenue - v. - Univation20210505-11-1a1tm6xervingabralagbonNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Fee Challan 10 Nov 2021Document1 pageFee Challan 10 Nov 2021Choudary UmerNo ratings yet

- Vaibhav 2023 NewDocument71 pagesVaibhav 2023 NewNeo MatrixNo ratings yet

- Calculate Income Tax and Break Even AnalysisDocument3 pagesCalculate Income Tax and Break Even AnalysisAbrar Ahmed KhanNo ratings yet

- USA VERIZON Iphone12 64GB BLUEDocument3 pagesUSA VERIZON Iphone12 64GB BLUEAnna DEGNER100% (1)

- WALC JSC's CIT liability for year ended 31 Dec 2020Document3 pagesWALC JSC's CIT liability for year ended 31 Dec 2020Ngọc MinhNo ratings yet

- Fai1. DISBURSEMENT VOUCHER 3 COPIESDocument56 pagesFai1. DISBURSEMENT VOUCHER 3 COPIESagong lodgeNo ratings yet

- Benitez, Allan Christian C. Doctrine: Bill of Exchange (Definition & Concept)Document5 pagesBenitez, Allan Christian C. Doctrine: Bill of Exchange (Definition & Concept)Arrianne ObiasNo ratings yet

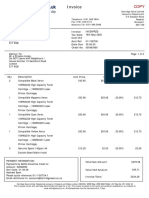

- InvoiceDocument1 pageInvoiceAbhijeet KumarNo ratings yet

- Fixedline and broadband bill detailsDocument3 pagesFixedline and broadband bill detailsTony JanualNo ratings yet

- GST Registration Procedure and FAQsDocument21 pagesGST Registration Procedure and FAQsSahil KumarNo ratings yet

- TD Beyond Checking: Account SummaryDocument4 pagesTD Beyond Checking: Account SummaryJohn BeanNo ratings yet

- Bhupendra Ratilal Mali Pay SlipsDocument3 pagesBhupendra Ratilal Mali Pay SlipsDevenNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument8 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceMishra SanjayNo ratings yet

- e-StatementBRImo 433801009403539 Oct2023 20231105 022505Document22 pagese-StatementBRImo 433801009403539 Oct2023 20231105 022505Dede Jua KurniasariNo ratings yet

- InvoiceDocument1 pageInvoicesyed aamiriNo ratings yet

- Share Price List: Cost BasisDocument13 pagesShare Price List: Cost BasisChristian Baldonado AngelesNo ratings yet

- E Payment I.T On Salary Mo April-19Document12 pagesE Payment I.T On Salary Mo April-19HussainMohammadUmarNo ratings yet

- Dahab Tower Apartments Payment PlanDocument3 pagesDahab Tower Apartments Payment PlanLexico InternationalNo ratings yet

- Soal Uas Praktikum Akun TambahanDocument20 pagesSoal Uas Praktikum Akun TambahanAl VengerNo ratings yet

- Christopher Driskell - MATH 12 (10.1) the US Tax SystemDocument3 pagesChristopher Driskell - MATH 12 (10.1) the US Tax SystemdriskelltopherNo ratings yet

- Taxation Theory QuestionsDocument7 pagesTaxation Theory QuestionsPrince kumarNo ratings yet

- Invoice: Invoice Tax Date Cust Ord Acct Ref Date Due Order No. 005463400 Invoice ToDocument2 pagesInvoice: Invoice Tax Date Cust Ord Acct Ref Date Due Order No. 005463400 Invoice ToA PirzadaNo ratings yet

- Account Statement: NSDL Payments BankDocument3 pagesAccount Statement: NSDL Payments BankSantosh Kumar GuptaNo ratings yet

- Proof of Cash MQM ComDocument5 pagesProof of Cash MQM ComCJ alandyNo ratings yet

- Chapter 6 Bank Recon Practice QHDocument3 pagesChapter 6 Bank Recon Practice QHSuy Yanghear100% (1)

- Tax On Individuals Part 2Document10 pagesTax On Individuals Part 2Tet AleraNo ratings yet

- Maxime Carriere (Done Rite Fire Protection Inc)Document1 pageMaxime Carriere (Done Rite Fire Protection Inc)Floyd McDermottNo ratings yet

- TDON1Document2 pagesTDON1Fevzi OzdemirNo ratings yet

- Mobile Services: Your Account Summary This Month'S ChargesDocument2 pagesMobile Services: Your Account Summary This Month'S ChargesJATIN GOYAL100% (1)

- Tax Return ScribdDocument5 pagesTax Return ScribdYvonne TanNo ratings yet