You might also like

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- I Bet You Thought - Ny FedDocument36 pagesI Bet You Thought - Ny FedK100% (2)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Securitization and Foreclosure by Robert RamersDocument8 pagesSecuritization and Foreclosure by Robert RamersBob Ramers100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Negotiable Instrument Act, 1881Document24 pagesNegotiable Instrument Act, 1881siddharth devnaniNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Ateneo 2007 Commercial LawDocument124 pagesAteneo 2007 Commercial LawJingJing Romero100% (54)

- Non Resident Ordy Rupee Nro AccountDocument5 pagesNon Resident Ordy Rupee Nro AccountAmar SinhaNo ratings yet

- Letter of CreditDocument31 pagesLetter of Creditmariachristina8850% (2)

- JOYDocument33 pagesJOYAnonymous spf4bYDkNo ratings yet

- Retail BankingDocument238 pagesRetail BankingMukesh SainiNo ratings yet

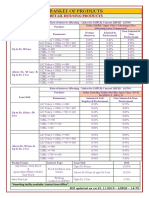

- BASKET OF PRODUCTS As On 21.11.19Document3 pagesBASKET OF PRODUCTS As On 21.11.19Virendra K VermaNo ratings yet

- Money Time Relationships and Equivalence PDFDocument21 pagesMoney Time Relationships and Equivalence PDFTaga Phase 7No ratings yet

- Siliguri Telecom DistrictDocument2 pagesSiliguri Telecom Districtkabita dasNo ratings yet

- Lecture 12-10-2021Document13 pagesLecture 12-10-2021darioNo ratings yet

- Chap 012 BBDocument8 pagesChap 012 BBMyaNo ratings yet

- PDF Principles of Financial Regulation John Armour Ebook Full ChapterDocument53 pagesPDF Principles of Financial Regulation John Armour Ebook Full Chapterarminda.basinski214No ratings yet

- Neo Bank The Future of Retail Banking: IntroductionDocument6 pagesNeo Bank The Future of Retail Banking: IntroductionSai ManoharNo ratings yet

- Analysis of Risk and Its Management in Indian Banks: A Case of SBI BankDocument19 pagesAnalysis of Risk and Its Management in Indian Banks: A Case of SBI BankRITIKANo ratings yet

- UK Neo Banks A Comparative Analysis 1599968163Document15 pagesUK Neo Banks A Comparative Analysis 1599968163Turab DXBNo ratings yet

- Transfer Confirmation EUR 14-Mar-2024 09.20.37Document1 pageTransfer Confirmation EUR 14-Mar-2024 09.20.37klimovnanceNo ratings yet

- Handbook How To Do Business in GC enDocument8 pagesHandbook How To Do Business in GC enСергей МартынецNo ratings yet

- Reserch Final-2Document76 pagesReserch Final-2Kalkidan ZerihunNo ratings yet

- y LP 4 XZKJC LZG 9 BF 9Document6 pagesy LP 4 XZKJC LZG 9 BF 9Korvi NareshNo ratings yet

- The Savings and Loan Crisis DSDocument7 pagesThe Savings and Loan Crisis DSMonsur BolajiNo ratings yet

- Receipt 8585870553 April16Document1 pageReceipt 8585870553 April16Nishikant MeshramNo ratings yet

- 03 Takaful MAYBANK EZYPAY Application Form V1.0 2018Document2 pages03 Takaful MAYBANK EZYPAY Application Form V1.0 2018UstazFaizalAriffinOriginalNo ratings yet

- The Gazette: of IndiaDocument4 pagesThe Gazette: of Indiagurpreet06No ratings yet

- Bankscope Export 14Document1,381 pagesBankscope Export 14yacobo sijabatNo ratings yet

- Payable at Meezan Bank LTD Payable at Meezan Bank LTD Payable at Meezan Bank LTDDocument2 pagesPayable at Meezan Bank LTD Payable at Meezan Bank LTD Payable at Meezan Bank LTDKarim GabolNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument13 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAbhishekNo ratings yet

- Banks Nodal Officer PMMYDocument1 pageBanks Nodal Officer PMMYHarchitvan SinghNo ratings yet

- Santander's Acquisition of Abbey: Banking Across BordersDocument29 pagesSantander's Acquisition of Abbey: Banking Across BordersJawad FarisiNo ratings yet