You might also like

- I Got A Bar Complaint by Brian TannebaumDocument25 pagesI Got A Bar Complaint by Brian TannebaumBrian Tannebaum100% (2)

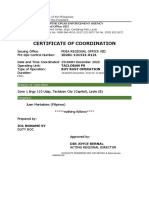

- Certificate of Coordination: Area(s) of OperationDocument3 pagesCertificate of Coordination: Area(s) of OperationervingabralagbonNo ratings yet

- Commissioner of Internal Revenue vs. T. Shuttle Services, Inc.Document6 pagesCommissioner of Internal Revenue vs. T. Shuttle Services, Inc.Carla DomingoNo ratings yet

- RemediesDocument36 pagesRemediesDaryll Gayle AsuncionNo ratings yet

- Commissioner of Internal Revenue vs. First Express Pawnshop G.R. Nos.Document8 pagesCommissioner of Internal Revenue vs. First Express Pawnshop G.R. Nos.4bn77yn8dkNo ratings yet

- Asian Transmission Corp. v. CIR (2022)Document6 pagesAsian Transmission Corp. v. CIR (2022)Lyn Jeen BinuaNo ratings yet

- CIR v. First Express PawnshopDocument14 pagesCIR v. First Express PawnshopMi-young SunNo ratings yet

- CLEOFEDocument5 pagesCLEOFEAustin Viel Lagman MedinaNo ratings yet

- Case Digest TaxationDocument20 pagesCase Digest TaxationGenevive GabionNo ratings yet

- G.R. No. 175097 Allied Banking Corporation, Petitioner, vs. Commissioner of Internal Revenue, Respondent. Del Castillo, J.Document2 pagesG.R. No. 175097 Allied Banking Corporation, Petitioner, vs. Commissioner of Internal Revenue, Respondent. Del Castillo, J.thelionleo1No ratings yet

- Tax Audit G.R. No. 172045-46, June 16, 2009 FANDocument25 pagesTax Audit G.R. No. 172045-46, June 16, 2009 FANQuinciano MorilloNo ratings yet

- Nippon Express (Philippines) Corporation vs. Commissioner of Internal Revenue (March 13, 2013)Document5 pagesNippon Express (Philippines) Corporation vs. Commissioner of Internal Revenue (March 13, 2013)Vince LeidoNo ratings yet

- CIR V T Shuttle Services Inc.Document2 pagesCIR V T Shuttle Services Inc.Gem AusteroNo ratings yet

- Cases To DigestDocument63 pagesCases To DigestPrincess CortezNo ratings yet

- CIR Vs Standard CharteredDocument2 pagesCIR Vs Standard CharteredFatzie MendozaNo ratings yet

- TAX II CasesDocument2 pagesTAX II CasesSir Nino CaganapNo ratings yet

- Facts:: G.R. No. 175723, February 4, 2014 The City of Manila vs. Hon. Caridad H. Grecia-CuerdoDocument5 pagesFacts:: G.R. No. 175723, February 4, 2014 The City of Manila vs. Hon. Caridad H. Grecia-CuerdoShielden B. MoradaNo ratings yet

- Allied Bank v. CIR Case DigestDocument4 pagesAllied Bank v. CIR Case DigestCareenNo ratings yet

- Tax CasesDocument16 pagesTax Casesnicole5anne5ddddddNo ratings yet

- Lascona Land Co. Inc. v. Commissioner of Internal Revenue, G.R. No. 171251, 05 March 2012Document10 pagesLascona Land Co. Inc. v. Commissioner of Internal Revenue, G.R. No. 171251, 05 March 2012Bernadette Luces BeldadNo ratings yet

- 2014 Tax CasesDocument98 pages2014 Tax Casestepi7wepiNo ratings yet

- LIM GAW Vs CIRDocument7 pagesLIM GAW Vs CIRMarion JossetteNo ratings yet

- Cir VS StiDocument6 pagesCir VS StiNaomiJean InotNo ratings yet

- TAX Digests - Prescription of RemediesDocument6 pagesTAX Digests - Prescription of RemediesFrancisCarloL.FlameñoNo ratings yet

- Edison (Bataan) Cogeneration Corporation v. CIR, G.R. No. 210665, 30 August 2017Document2 pagesEdison (Bataan) Cogeneration Corporation v. CIR, G.R. No. 210665, 30 August 2017Jarleine Junio BeringuelNo ratings yet

- G.R. No. 192173 Cir, vs. Standard Chartered Bank,: FactsDocument2 pagesG.R. No. 192173 Cir, vs. Standard Chartered Bank,: FactsGladys Bustria Orlino0% (1)

- Supreme Court: Factual AntecedentsDocument33 pagesSupreme Court: Factual AntecedentsCarmelie CumigadNo ratings yet

- Supreme Court: Factual AntecedentsDocument9 pagesSupreme Court: Factual Antecedentspoloy6200No ratings yet

- 163611-2009-Commissioner of Internal Revenue v. FirstDocument15 pages163611-2009-Commissioner of Internal Revenue v. Firstlouis jansenNo ratings yet

- En Banc Commissioner of Internal Revenue v. Northern Tobacco Redrying Co., Inc.Document11 pagesEn Banc Commissioner of Internal Revenue v. Northern Tobacco Redrying Co., Inc.Vince Lupango (imistervince)No ratings yet

- Case of The DayDocument29 pagesCase of The DayToni Gabrielle Ang EspinaNo ratings yet

- CIR v. T Shuttle ServicesDocument14 pagesCIR v. T Shuttle ServicesArrianne ObiasNo ratings yet

- CIR Vs First Express - Case DigestDocument2 pagesCIR Vs First Express - Case DigestKaren Mae ServanNo ratings yet

- GR 128315Document5 pagesGR 128315thelionleo1No ratings yet

- Banc in CTA EB Case Nos. 591 and 628, Which Set Aside The Amended DecisionDocument7 pagesBanc in CTA EB Case Nos. 591 and 628, Which Set Aside The Amended DecisionJerome CasasNo ratings yet

- CIR v. Metro Star SupremaDocument3 pagesCIR v. Metro Star SupremaNichol Uriel ArcaNo ratings yet

- 10 - CIR v. Yusen Logistics Center, Inc.Document3 pages10 - CIR v. Yusen Logistics Center, Inc.Carlota VillaromanNo ratings yet

- CIR vs. Metro Star Superama, G.R. No. 185371, December 8, 2010Document3 pagesCIR vs. Metro Star Superama, G.R. No. 185371, December 8, 2010Mich LopezNo ratings yet

- Case Digest Atty CabaneiroDocument11 pagesCase Digest Atty CabaneiroChriselle Marie DabaoNo ratings yet

- Case Digest 1-4Document6 pagesCase Digest 1-4Carla DomingoNo ratings yet

- 40 Commissioner of Internal Revenue v. V.y.20210505-11-H3rmb1Document10 pages40 Commissioner of Internal Revenue v. V.y.20210505-11-H3rmb1KempetsNo ratings yet

- Court of Tax Appeal: Chairperson, andDocument19 pagesCourt of Tax Appeal: Chairperson, andJason MergalNo ratings yet

- CIR Vs PAL - ConstructionDocument8 pagesCIR Vs PAL - ConstructionEvan NervezaNo ratings yet

- CIR vs. Yumex Philippines CorporationDocument17 pagesCIR vs. Yumex Philippines CorporationJohn FerarenNo ratings yet

- CIR v. Univation, GR 231581, 10 Apr 2019Document4 pagesCIR v. Univation, GR 231581, 10 Apr 2019Dan Millado100% (2)

- A. 5. C. Commissioner of Internal Revenue vs. Bank of The Philippine IslandsDocument3 pagesA. 5. C. Commissioner of Internal Revenue vs. Bank of The Philippine IslandsasdfghjkattNo ratings yet

- CIR Vs Team PhilippinesDocument4 pagesCIR Vs Team PhilippinesJennylyn Biltz AlbanoNo ratings yet

- CIR Vs First ExpressDocument7 pagesCIR Vs First ExpressGhreighz GalinatoNo ratings yet

- G.R. No. 134062 April 17, 2007 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentDocument21 pagesG.R. No. 134062 April 17, 2007 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentzzzNo ratings yet

- CIR v. Next Mobile IncDocument9 pagesCIR v. Next Mobile IncMeg ReyesNo ratings yet

- AJJJJJJJJJJJJJJJDocument2 pagesAJJJJJJJJJJJJJJJanthony paduaNo ratings yet

- G. R. No. 185568Document26 pagesG. R. No. 185568Rache BaodNo ratings yet

- Cir v. Pascor (309 Scra 402)Document7 pagesCir v. Pascor (309 Scra 402)Karl MinglanaNo ratings yet

- Tax Remedies Digest 62 70Document12 pagesTax Remedies Digest 62 70Christine Angelus MosquedaNo ratings yet

- Cir VS BpiDocument2 pagesCir VS BpiCelinka ChunNo ratings yet

- First Division - MacarioDocument12 pagesFirst Division - MacarioJohn Evan Raymund BesidNo ratings yet

- REmedies Procedure Lecture 1Document5 pagesREmedies Procedure Lecture 1Susannie AcainNo ratings yet

- 22) ASIAN TRANSMISSION Vs CIR - J.BersaminDocument5 pages22) ASIAN TRANSMISSION Vs CIR - J.BersaminStalin LeningradNo ratings yet

- Case Digests On Tax Remedies and JurisdictionsDocument36 pagesCase Digests On Tax Remedies and JurisdictionsNurul-Izza A. Sangcopan100% (2)

- Modern Imaging Solutions Case Tax FRDocument18 pagesModern Imaging Solutions Case Tax FRLykel LavillaNo ratings yet

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersFrom EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNo ratings yet

- Legal & Judicial Ethics & Practical Exercises SyllabusDocument8 pagesLegal & Judicial Ethics & Practical Exercises Syllabuservingabralagbon100% (1)

- Tacloban City Police Station: Hotline - 0998.598.6680Document2 pagesTacloban City Police Station: Hotline - 0998.598.6680ervingabralagbonNo ratings yet

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- Ethics - FINALS - Additional CasesDocument12 pagesEthics - FINALS - Additional CaseservingabralagbonNo ratings yet

- People Vs MarbabiesDocument3 pagesPeople Vs MarbabieservingabralagbonNo ratings yet

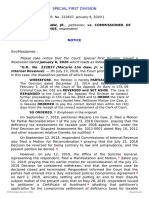

- 46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)Document9 pages46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)ervingabralagbonNo ratings yet

- 35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iDocument11 pages35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iervingabralagbonNo ratings yet

- Petitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueDocument19 pagesPetitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueervingabralagbonNo ratings yet

- 53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfDocument20 pages53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfervingabralagbonNo ratings yet

- 48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedDocument19 pages48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedervingabralagbonNo ratings yet

- M-E-P-C-, AXXX XXX 389 (BIA Sept. 2, 2015)Document6 pagesM-E-P-C-, AXXX XXX 389 (BIA Sept. 2, 2015)Immigrant & Refugee Appellate Center, LLCNo ratings yet

- LONGTIN v. UNITED STATES DEPARTMENT OF JUSTICE Et Al - Document No. 8Document8 pagesLONGTIN v. UNITED STATES DEPARTMENT OF JUSTICE Et Al - Document No. 8Justia.comNo ratings yet

- GAA v. CADocument2 pagesGAA v. CAJoesil Dianne SempronNo ratings yet

- U.S. v. Ney, Et Al DigestDocument1 pageU.S. v. Ney, Et Al DigestYvette MoralesNo ratings yet

- Extinction of Criminal Liability: People vs. Saturnino Dela Cruz G.R. No. 190610 March 25, 2012Document18 pagesExtinction of Criminal Liability: People vs. Saturnino Dela Cruz G.R. No. 190610 March 25, 2012Pauline Eunice Sabareza LobiganNo ratings yet

- Form TM MDocument2 pagesForm TM Mshivasakthi18No ratings yet

- Human Trafficking YouthDocument59 pagesHuman Trafficking YouthJanetGraceDalisayFabreroNo ratings yet

- Gios Samar Vs DOTCDocument38 pagesGios Samar Vs DOTCLady Lyn DinerosNo ratings yet

- Constifulltextcases FreedomofreligionDocument185 pagesConstifulltextcases FreedomofreligionJanine CastroNo ratings yet

- Lecture 4 Test To CompleteDocument3 pagesLecture 4 Test To CompleteІрина МишкаNo ratings yet

- 2 - Republic vs. Coseteng-Magpayo - 13 PDFDocument13 pages2 - Republic vs. Coseteng-Magpayo - 13 PDFFbarrsNo ratings yet

- Interpretation Law AssignmentDocument12 pagesInterpretation Law AssignmentABHISHEK MARORIANo ratings yet

- Intro To Law Reviewer MidtermDocument8 pagesIntro To Law Reviewer MidtermGuazon Jommel C.No ratings yet

- Geeta Saar 44 Manager and Managing DirectorDocument4 pagesGeeta Saar 44 Manager and Managing DirectorSommya KhandelwalNo ratings yet

- Supreme Court Judgement On Non Maintainablity of Case Under Sec 182 IPC Without Following Sec 195 CRPCDocument7 pagesSupreme Court Judgement On Non Maintainablity of Case Under Sec 182 IPC Without Following Sec 195 CRPCLatest Laws Team100% (1)

- Aguirre v. CADocument7 pagesAguirre v. CAMykaNo ratings yet

- Regional Trial Court: September 7Document2 pagesRegional Trial Court: September 7DiorVelasquezNo ratings yet

- Final Respondent MemorialDocument26 pagesFinal Respondent MemorialAshutosh SinghNo ratings yet

- 29 - Sentinel Insurance Co., Inc. vs. Court of Appeals, 182 SCRA 517, 23 February 1990Document2 pages29 - Sentinel Insurance Co., Inc. vs. Court of Appeals, 182 SCRA 517, 23 February 1990ESS PORT OF LEGAZPI CPD-ESSNo ratings yet

- SECTION 167 CRPC FinalDocument12 pagesSECTION 167 CRPC Finaljon snow snowNo ratings yet

- DynaEnergetics Europe v. PerfX Wireless - ComplaintDocument101 pagesDynaEnergetics Europe v. PerfX Wireless - ComplaintSarah BursteinNo ratings yet

- Application For Probation - RA 9262Document2 pagesApplication For Probation - RA 9262Boom ManuelNo ratings yet

- Narrate The History of GST in IndiaDocument6 pagesNarrate The History of GST in IndiaHari KrishnanNo ratings yet

- Krissia Rosibel Paz-Avalos, A200 123 950 (BIA Dec. 6, 2012)Document6 pagesKrissia Rosibel Paz-Avalos, A200 123 950 (BIA Dec. 6, 2012)Immigrant & Refugee Appellate Center, LLCNo ratings yet

- United States v. Shaquan Manson, 4th Cir. (2015)Document5 pagesUnited States v. Shaquan Manson, 4th Cir. (2015)Scribd Government DocsNo ratings yet

- Kellum ChargesDocument5 pagesKellum ChargesTravis MaldonadoNo ratings yet

- Karnataka (Sandur Area) Inams Abolition Act, 1976Document18 pagesKarnataka (Sandur Area) Inams Abolition Act, 1976Latest Laws TeamNo ratings yet

- Nunes Family ComplaintDocument21 pagesNunes Family ComplaintLaw&CrimeNo ratings yet

- Environment ProjectDocument7 pagesEnvironment ProjectvarunNo ratings yet