You might also like

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Short Book of The Drow LanguageDocument45 pagesShort Book of The Drow LanguageWolf100% (3)

- 06 X Death Undaunted X (2006)Document31 pages06 X Death Undaunted X (2006)WolfNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- SUCCESSIONDocument83 pagesSUCCESSIONJun Bill Cercado100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Suggested Sample Format For Shared Purchase Agreement: Drafted by Legal Help ClubDocument2 pagesSuggested Sample Format For Shared Purchase Agreement: Drafted by Legal Help ClubsushmanjaliNo ratings yet

- Deed of Transfer of Rights - 1Document2 pagesDeed of Transfer of Rights - 1Jane Marian100% (3)

- Notarial LawDocument17 pagesNotarial LawDave Froilan EsperilaNo ratings yet

- 5 6087021866017358188 PDFDocument1,822 pages5 6087021866017358188 PDFAnay MehrotraNo ratings yet

- VALENZUELA v. CA G.R. No. 83122Document3 pagesVALENZUELA v. CA G.R. No. 83122SS100% (1)

- Guest Orientation On House RulesDocument14 pagesGuest Orientation On House Rulesᜃᜓᜊᜒᜈ ᜄ᜔ᜈᜀᜌᜀᜐ100% (2)

- Soul Blazer (U)Document21 pagesSoul Blazer (U)WolfNo ratings yet

- Super Mario All-Stars + Super Mario World (U)Document35 pagesSuper Mario All-Stars + Super Mario World (U)WolfNo ratings yet

- Terranigma (UK)Document21 pagesTerranigma (UK)WolfNo ratings yet

- Legend of Zelda, The - A Link To The Past (U)Document25 pagesLegend of Zelda, The - A Link To The Past (U)WolfNo ratings yet

- Secret of Evermore (U)Document20 pagesSecret of Evermore (U)WolfNo ratings yet

- Secret of Mana (Map) (U)Document2 pagesSecret of Mana (Map) (U)WolfNo ratings yet

- Books in The Series: FR Code TSR Code Title PublishedDocument4 pagesBooks in The Series: FR Code TSR Code Title PublishedWolfNo ratings yet

- Books in The SeriesDocument4 pagesBooks in The SeriesWolfNo ratings yet

- Partnership FirmDocument15 pagesPartnership FirmNavpreet SinghNo ratings yet

- CASE OF HASAN AND CHAUSH v. BULGARIADocument34 pagesCASE OF HASAN AND CHAUSH v. BULGARIATudor IonNo ratings yet

- Policies Mutual AssistanceDocument4 pagesPolicies Mutual AssistanceDonna Fe Patiluna100% (1)

- Legal Memorandum AssignmentDocument2 pagesLegal Memorandum AssignmentValli WilliamsonNo ratings yet

- B-01-Ganesh - M.I.builder V Radhey Shyam SahuDocument4 pagesB-01-Ganesh - M.I.builder V Radhey Shyam SahuGanesh MaliNo ratings yet

- Bianca Juan SoutoDocument3 pagesBianca Juan SoutoBianca Juan SoutoNo ratings yet

- Civil Appeal 95 of 1999Document5 pagesCivil Appeal 95 of 1999vusNo ratings yet

- Lets Crack PCS (J) : With UnacademyDocument59 pagesLets Crack PCS (J) : With UnacademySanjeev kumarNo ratings yet

- Sap Pe Build Master Partner Agreement Sample English v5 2021Document2 pagesSap Pe Build Master Partner Agreement Sample English v5 2021Nick FasciNo ratings yet

- Revised Penal Code Title Four Article 161-176Document4 pagesRevised Penal Code Title Four Article 161-176sherluck siapnoNo ratings yet

- The Lord Is My ShepherdDocument1 pageThe Lord Is My Shepherdbryan cagang gomezNo ratings yet

- The Majority Rule and The MinorityDocument24 pagesThe Majority Rule and The MinorityHina KausarNo ratings yet

- Nemenso, Ariana Necole A. - Acceptance LetterDocument1 pageNemenso, Ariana Necole A. - Acceptance LetterRitchiel MirasolNo ratings yet

- Arise (Y Ou Are Good) : Rhythm ChartDocument4 pagesArise (Y Ou Are Good) : Rhythm ChartJonté MooreNo ratings yet

- Study Material Memorandum of Association PDFDocument3 pagesStudy Material Memorandum of Association PDFSaptarshi DasNo ratings yet

- Full Download Bcom Canadian 1st Edition Lehman Test BankDocument17 pagesFull Download Bcom Canadian 1st Edition Lehman Test Banksmallmanclaude100% (37)

- Perez, Nuguid v. NuguidDocument6 pagesPerez, Nuguid v. NuguidPepper PottsNo ratings yet

- Freshers Induction Moot 2023Document5 pagesFreshers Induction Moot 2023Akash VermaNo ratings yet

- Transfer of PropertyDocument8 pagesTransfer of PropertyHere ThereNo ratings yet

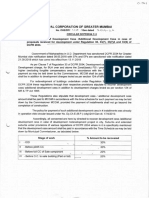

- 30-01-2020 MCGM Circular About Charging of Development Cess Additional Develpment Cess Under Reg. 30, 33 (7), 33 (7) A & 33Document2 pages30-01-2020 MCGM Circular About Charging of Development Cess Additional Develpment Cess Under Reg. 30, 33 (7), 33 (7) A & 33Vidya AdsuleNo ratings yet

- Pension - RR 01-83 Amend - 211118 - 115738Document4 pagesPension - RR 01-83 Amend - 211118 - 115738HADTUGINo ratings yet

- Ebook PDF Contracts in Context From Transaction To Litigation Aspen Casebook PDFDocument40 pagesEbook PDF Contracts in Context From Transaction To Litigation Aspen Casebook PDFflorence.padilla424100% (41)

- The Omega Case Summary and The Principle PDFDocument2 pagesThe Omega Case Summary and The Principle PDFOsca ReignNo ratings yet