You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The German Army (1939-45)Document50 pagesThe German Army (1939-45)gottesvieh100% (11)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Unit 3 - Ottoman Empire Case Study (Documents)Document8 pagesUnit 3 - Ottoman Empire Case Study (Documents)Travy PattyNo ratings yet

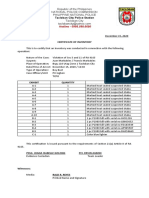

- Certificate of Coordination: Area(s) of OperationDocument3 pagesCertificate of Coordination: Area(s) of OperationervingabralagbonNo ratings yet

- Tacloban City Police Station: Hotline - 0998.598.6680Document2 pagesTacloban City Police Station: Hotline - 0998.598.6680ervingabralagbonNo ratings yet

- Legal & Judicial Ethics & Practical Exercises SyllabusDocument8 pagesLegal & Judicial Ethics & Practical Exercises Syllabuservingabralagbon100% (1)

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- Ethics - FINALS - Additional CasesDocument12 pagesEthics - FINALS - Additional CaseservingabralagbonNo ratings yet

- People Vs MarbabiesDocument3 pagesPeople Vs MarbabieservingabralagbonNo ratings yet

- 36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0Document10 pages36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0ervingabralagbonNo ratings yet

- 46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)Document9 pages46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)ervingabralagbonNo ratings yet

- 35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iDocument11 pages35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iervingabralagbonNo ratings yet

- 48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedDocument19 pages48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedervingabralagbonNo ratings yet

- 53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfDocument20 pages53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfervingabralagbonNo ratings yet

- Petitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueDocument19 pagesPetitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueervingabralagbonNo ratings yet

- Anti Ragging 2019Document1 pageAnti Ragging 2019GANESH KUMAR B eee2018No ratings yet

- FIL3A - DIGEST Rimbunan Hijau Group V Oriental WoodDocument2 pagesFIL3A - DIGEST Rimbunan Hijau Group V Oriental WoodAnjanette MangalindanNo ratings yet

- Consolidated Case Digests 49 To 89Document69 pagesConsolidated Case Digests 49 To 89Bert RoseteNo ratings yet

- Exo FanficsDocument4 pagesExo FanficsIoana AdelinaNo ratings yet

- Statutory Cases Case Title: G.R. No. L-19650 (September 29, 1966)Document82 pagesStatutory Cases Case Title: G.R. No. L-19650 (September 29, 1966)Nong Mitra100% (6)

- P.poblete and I.medinaDocument27 pagesP.poblete and I.medinascribidyNo ratings yet

- Mla Worksheet-220Document3 pagesMla Worksheet-220api-289656014100% (1)

- Income and Asset Certificate For EWS September 2019Document5 pagesIncome and Asset Certificate For EWS September 2019inderpreetNo ratings yet

- Thesis Statement For Research Paper On William ShakespeareDocument5 pagesThesis Statement For Research Paper On William ShakespearehxmchprhfNo ratings yet

- Senate Hearings: Department of Defense AppropriationsDocument697 pagesSenate Hearings: Department of Defense AppropriationsScribd Government DocsNo ratings yet

- Primicias Vs Fugoso 80 Phil 71 G.R. No. L-1800Document19 pagesPrimicias Vs Fugoso 80 Phil 71 G.R. No. L-1800Trebx Sanchez de GuzmanNo ratings yet

- BARANGAY ResolutionDocument2 pagesBARANGAY ResolutionCarol Cabadsan Fabrao100% (1)

- Ingjug-Tiro v. CasalsDocument6 pagesIngjug-Tiro v. CasalsniñoNo ratings yet

- The Ladrones Islands Is Presently Known As The Marianas Islands. These Islands Are Located South-Southeast of Japan, West-Southwest of Hawaii, North of New Guinea, and East of Philippines. TenDocument10 pagesThe Ladrones Islands Is Presently Known As The Marianas Islands. These Islands Are Located South-Southeast of Japan, West-Southwest of Hawaii, North of New Guinea, and East of Philippines. TenAngel Al-agNo ratings yet

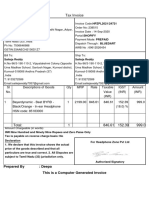

- Invoice of EarphonesDocument1 pageInvoice of EarphonesSai TejaNo ratings yet

- Gec 102 Activity 6 The Cry of Pugad LawinDocument5 pagesGec 102 Activity 6 The Cry of Pugad LawinDaylan Lindo MontefalcoNo ratings yet

- The First Station Jesus Is Condemned To DeathDocument42 pagesThe First Station Jesus Is Condemned To DeathRamchandra MurthyNo ratings yet

- Republic of The Philippines Vs CAGUIOADocument14 pagesRepublic of The Philippines Vs CAGUIOAAnonymous NWnRYIWNo ratings yet

- ADR - RTC DecisionDocument13 pagesADR - RTC DecisionJemaineNo ratings yet

- 2016 05 USA CB SAT-Practice-Test-05Document142 pages2016 05 USA CB SAT-Practice-Test-05Tulong ZhuNo ratings yet

- Kinds of PleadingsDocument2 pagesKinds of PleadingsSircanit BentayoNo ratings yet

- ESIC To Membership Agreement TemplateDocument7 pagesESIC To Membership Agreement TemplateHertz UnitNo ratings yet

- Cultural Diplomacy and Pakistan-India RelationsDocument14 pagesCultural Diplomacy and Pakistan-India RelationsYaqoob BangashNo ratings yet

- Actual Mock Test 9.45Document4 pagesActual Mock Test 9.45Nam Nguyễn HảiNo ratings yet

- Current Scenarion of Caste in IndiaDocument18 pagesCurrent Scenarion of Caste in IndiaAvinashNo ratings yet

- Oral Comm PTDocument2 pagesOral Comm PTmyoui minaNo ratings yet

- DSPC Training MondayDocument5 pagesDSPC Training MondayVerlin Amarante EntenaNo ratings yet

- United States Court of Appeals Fourth CircuitDocument7 pagesUnited States Court of Appeals Fourth CircuitScribd Government DocsNo ratings yet