You might also like

- ASSIGNMENTS Part2 Module 3Document5 pagesASSIGNMENTS Part2 Module 3Lorifel Antonette Laoreno TejeroNo ratings yet

- 2.ast - Hoba Part 1Document12 pages2.ast - Hoba Part 1ElaineJrV-IgotNo ratings yet

- Working Paper Part 2Document3 pagesWorking Paper Part 2KEITH JEROME VIERNESNo ratings yet

- Accounts Unadjusted Trial Balance AdjustmentsDocument9 pagesAccounts Unadjusted Trial Balance AdjustmentsEiza LaxaNo ratings yet

- Jawaban TugasDocument23 pagesJawaban TugasRusnawati Nur AminahNo ratings yet

- Final Worksheet Trial BalanceDocument2 pagesFinal Worksheet Trial BalanceLhara GallendoNo ratings yet

- Accounting 3 4 Module 3aDocument2 pagesAccounting 3 4 Module 3aMnriMinaNo ratings yet

- General Journal Page Number 01 Descriptions PR Debit CreditDocument12 pagesGeneral Journal Page Number 01 Descriptions PR Debit CreditKurt SoriaoNo ratings yet

- Investments in Financial Instruments CompleteDocument34 pagesInvestments in Financial Instruments CompleteDenise CruzNo ratings yet

- Practice Problem SolutionDocument15 pagesPractice Problem SolutionTherese Noelle R. ARMADA100% (1)

- FABMDocument4 pagesFABMDwyth Anne MonterasNo ratings yet

- Problem 14Document2 pagesProblem 14Nepal Bishal ShresthaNo ratings yet

- Form Kosong-1Document12 pagesForm Kosong-1Toold 75No ratings yet

- Chapter 11,12,13Document20 pagesChapter 11,12,13Nikki GarciaNo ratings yet

- BA 205 AnswerDocument5 pagesBA 205 AnswerAnhar Polo CanacanNo ratings yet

- Quijonez Fashionables Comprehensive Prob Merchandising Solution - XLSX Direct Extension MethodDocument4 pagesQuijonez Fashionables Comprehensive Prob Merchandising Solution - XLSX Direct Extension MethodzairahNo ratings yet

- Prob 2 - Corporation ActDocument6 pagesProb 2 - Corporation ActDenise Jane DesoyNo ratings yet

- MC Problems and Financial Statements from AE 112 MidtermsDocument3 pagesMC Problems and Financial Statements from AE 112 MidtermseveNo ratings yet

- 4BSA2 GROUP2 GroupActivityNo.1Document4 pages4BSA2 GROUP2 GroupActivityNo.1Lizerie Joy Kristine CristobalNo ratings yet

- Drew SicatDocument1 pageDrew SicatShaine Cabualan SeroyNo ratings yet

- Problem I - SolutionsDocument10 pagesProblem I - SolutionsDing CostaNo ratings yet

- Gross Profit: Income Statement For The Year Ended December 31Document3 pagesGross Profit: Income Statement For The Year Ended December 31Jane VillanuevaNo ratings yet

- ENCANTADIA Company Worksheet For Year Ended Dec. 31, 2018Document8 pagesENCANTADIA Company Worksheet For Year Ended Dec. 31, 2018kent starkNo ratings yet

- Christine Sousa BagsDocument8 pagesChristine Sousa BagsKaila Clarisse Cortez100% (5)

- Consolidate Peanut and Snoopy FinancialsDocument4 pagesConsolidate Peanut and Snoopy FinancialsYandra Febriyanti0% (1)

- LabChapt P3-34 P3-35Document5 pagesLabChapt P3-34 P3-35Meisya VianqaNo ratings yet

- Date Adjusting Entries Dec.31Document18 pagesDate Adjusting Entries Dec.31Cheska Anne Mikka RoxasNo ratings yet

- Practice Set OwnDocument26 pagesPractice Set OwnCass MadriagaNo ratings yet

- 4.ast - Consignment & InstallmentDocument17 pages4.ast - Consignment & InstallmentElaineJrV-IgotNo ratings yet

- LabChapt 4 Meisya Vianqa ADocument7 pagesLabChapt 4 Meisya Vianqa AMeisya VianqaNo ratings yet

- Contingent Consideration AccountingDocument25 pagesContingent Consideration AccountingAEDRIAN LEE DERECHONo ratings yet

- Assignment 3Document14 pagesAssignment 3Jiaxi WNo ratings yet

- Hoba Icare Answer KeysDocument15 pagesHoba Icare Answer KeysMark Gelo WinchesterNo ratings yet

- Abusama 1st Assignment UpdatedDocument5 pagesAbusama 1st Assignment UpdatedDonna Mae SingsonNo ratings yet

- Chapter 17 Answer Key-1Document4 pagesChapter 17 Answer Key-1NCTNo ratings yet

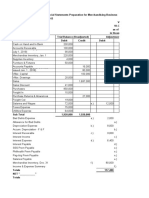

- DB6 - Worksheet & FS Prep For Merchandising BusinessDocument4 pagesDB6 - Worksheet & FS Prep For Merchandising BusinessArrianeNo ratings yet

- ABC MIDTERMS PROJECT Sene Di Pa TaposDocument11 pagesABC MIDTERMS PROJECT Sene Di Pa TaposJanesene SolNo ratings yet

- Accbp100 3rd Exam AnswersDocument8 pagesAccbp100 3rd Exam AnswersAlthea Marie OrtizNo ratings yet

- Lets Try This 4Document2 pagesLets Try This 4syramaebillones26No ratings yet

- Partnership - Dissolution Upon Ownership Changes: Problem 2-1Document22 pagesPartnership - Dissolution Upon Ownership Changes: Problem 2-1marieieiemNo ratings yet

- Problem 1: Show Your CalculationsDocument14 pagesProblem 1: Show Your CalculationsMaria Christy WoworNo ratings yet

- Analyzing Business Transactions Using ExcelDocument30 pagesAnalyzing Business Transactions Using ExcelPhaelyn YambaoNo ratings yet

- X201 Midterm Exam Worksheet 2021Document1 pageX201 Midterm Exam Worksheet 2021Kharen PadlanNo ratings yet

- Poa Mock Exam 2020Document13 pagesPoa Mock Exam 2020DanNo ratings yet

- Adjusting Entries and Financial StatementsDocument8 pagesAdjusting Entries and Financial StatementsRene Dacua PalabricaNo ratings yet

- Ass FS AnsDocument4 pagesAss FS AnsJhay Sy LynNo ratings yet

- Problem 6 - 3: Chapter 6 - AA2 (2014 Edition)Document4 pagesProblem 6 - 3: Chapter 6 - AA2 (2014 Edition)Izzy BNo ratings yet

- Assignment Branch AccountingDocument2 pagesAssignment Branch AccountingHeartwell Bernabe Licayan100% (1)

- Exercise 6 22 Acctba1Document11 pagesExercise 6 22 Acctba1Sophia Santos50% (2)

- Cristobal Store Problem 8-4 Accounts Adjusted Trial BalanceDocument3 pagesCristobal Store Problem 8-4 Accounts Adjusted Trial BalanceFakerPlaymakerNo ratings yet

- Allan & WallyDocument10 pagesAllan & WallyLaura OliviaNo ratings yet

- TRADING, PROFIT AND LOSS ACCOUNT AND BALANCE SHEETDocument37 pagesTRADING, PROFIT AND LOSS ACCOUNT AND BALANCE SHEETsarojdawadiNo ratings yet

- Celp Fabm Trial-BalanceDocument2 pagesCelp Fabm Trial-BalanceCherrykylie CorporalNo ratings yet

- Compute Controlling and Non-Controlling Interest SharesDocument6 pagesCompute Controlling and Non-Controlling Interest SharesNat SukiNo ratings yet

- Comprehensive Review SolutionsDocument20 pagesComprehensive Review SolutionsJane Ruby JennieferNo ratings yet

- PPE Acquisition and Borrowing CostDocument3 pagesPPE Acquisition and Borrowing Cost夜晨曦No ratings yet

- JM Mini Pizza Worksheet For The Year Ended 2021 Trial Balance Adjustment Adjusted Trial Balance Income Statement Balance SheetDocument4 pagesJM Mini Pizza Worksheet For The Year Ended 2021 Trial Balance Adjustment Adjusted Trial Balance Income Statement Balance SheetAbegail PanangNo ratings yet

- AccountingDocument14 pagesAccountingRizwana MehwishNo ratings yet

- Karen Moving Co. WorksheetDocument9 pagesKaren Moving Co. WorksheetDanica OnteNo ratings yet

- FreewillDocument2 pagesFreewillmarieieiemNo ratings yet

- HypothesisDocument4 pagesHypothesismarieieiemNo ratings yet

- If I Will Become A Literary GenreDocument1 pageIf I Will Become A Literary GenremarieieiemNo ratings yet

- Behrouze Garcia Phoebe Cuntapay ST - Leo The GreatDocument2 pagesBehrouze Garcia Phoebe Cuntapay ST - Leo The GreatmarieieiemNo ratings yet

- Guided QuestionnaireDocument1 pageGuided QuestionnairemarieieiemNo ratings yet

- GGGDocument6 pagesGGGmarieieiemNo ratings yet

- Concept Paper: Three Ways in Explaining A ConceptDocument6 pagesConcept Paper: Three Ways in Explaining A ConceptmarieieiemNo ratings yet

- Establishing A Business Is Not EasyDocument1 pageEstablishing A Business Is Not EasymarieieiemNo ratings yet

- Mission "Cagelco 1 Serves As A Catalyst For SocioDocument7 pagesMission "Cagelco 1 Serves As A Catalyst For SociomarieieiemNo ratings yet

- Entrepreneurship Amplifies Economic Activities of Different Sectors of SocietyDocument4 pagesEntrepreneurship Amplifies Economic Activities of Different Sectors of SocietymarieieiemNo ratings yet

- Creating Effective PresentationsDocument13 pagesCreating Effective PresentationsmarieieiemNo ratings yet

- How Do We Feel About TrafficDocument1 pageHow Do We Feel About TrafficmarieieiemNo ratings yet

- Aug 16Document7 pagesAug 16marieieiemNo ratings yet

- Basic Documents and Transactions Related TO: Bank DepositsDocument19 pagesBasic Documents and Transactions Related TO: Bank DepositsRizza MacanangNo ratings yet

- Bank ReconciliationDocument14 pagesBank ReconciliationKim Ternura100% (1)

- Beauty. Concept Paper. - AncesDocument2 pagesBeauty. Concept Paper. - AncesmarieieiemNo ratings yet

- Piko: Laro NG LahiDocument4 pagesPiko: Laro NG LahimarieieiemNo ratings yet

- Barr Ier: Think of An Object That You Consider A BarrierDocument9 pagesBarr Ier: Think of An Object That You Consider A BarriermarieieiemNo ratings yet

- Bazaar ResultDocument1 pageBazaar ResultmarieieiemNo ratings yet

- Product Design and Video Presentation Proposal: I. Basic InformationDocument5 pagesProduct Design and Video Presentation Proposal: I. Basic InformationmarieieiemNo ratings yet

- Advanced Word Processing SkillsDocument5 pagesAdvanced Word Processing SkillsmarieieiemNo ratings yet

- Chapter 1: IntroductionDocument143 pagesChapter 1: IntroductionmarieieiemNo ratings yet

- Biuag and MalanaDocument2 pagesBiuag and MalanahanselNo ratings yet

- Jamel P. Mateo, Mos, LPTDocument7 pagesJamel P. Mateo, Mos, LPTmarieieiemNo ratings yet

- Strategic Management Competitive Advantage Chapter 1Document21 pagesStrategic Management Competitive Advantage Chapter 1marieieiemNo ratings yet

- Norms and Values Status and Roles Conformity Copy 2Document37 pagesNorms and Values Status and Roles Conformity Copy 2marieieiem100% (1)

- Book 1Document3 pagesBook 1marieieiemNo ratings yet

- Work Experience Sheet: Instructions: 1. Include Only The Work Experiences Relevant To The Position Being Applied ToDocument1 pageWork Experience Sheet: Instructions: 1. Include Only The Work Experiences Relevant To The Position Being Applied TomarieieiemNo ratings yet

- DocxDocument15 pagesDocxmarieieiemNo ratings yet

- DocxDocument15 pagesDocxmarieieiemNo ratings yet

- Mastering of DepreciationDocument13 pagesMastering of DepreciationdieuvubinhNo ratings yet

- PT Matahari Department Store TBK Dan Entitas Anak/And Subsidiaries Laporan Keuangan KonsolidasianDocument103 pagesPT Matahari Department Store TBK Dan Entitas Anak/And Subsidiaries Laporan Keuangan KonsolidasianStevi MujonoNo ratings yet

- Session 9 - Accounting For Fixed AssetsDocument37 pagesSession 9 - Accounting For Fixed AssetsKashish Manish JariwalaNo ratings yet

- Club Income & Expenditure Report 1899Document4 pagesClub Income & Expenditure Report 1899fauda babuNo ratings yet

- Variable Costing and The Measurement of ESG and Quality CostsDocument53 pagesVariable Costing and The Measurement of ESG and Quality CostsVân Hải100% (2)

- Common Size Analysis and Financial RatiosDocument4 pagesCommon Size Analysis and Financial RatiosLina Levvenia RatanamNo ratings yet

- Team PRTC May 2023 1st PBDocument46 pagesTeam PRTC May 2023 1st PBEpfie SanchesNo ratings yet

- Chapter 9 Audit Procedures and Obtaining EvidenceDocument4 pagesChapter 9 Audit Procedures and Obtaining Evidencekevin digumberNo ratings yet

- LCCI L3 Certificate in Accounting ASE20104 July 2017Document16 pagesLCCI L3 Certificate in Accounting ASE20104 July 2017Aung Zaw HtweNo ratings yet

- Review Questions For Test 1 ACC110Document6 pagesReview Questions For Test 1 ACC110FOREVER FREENo ratings yet

- Navjeet Singh SobtiDocument18 pagesNavjeet Singh SobtiShreyans GirathNo ratings yet

- DepreciationDocument2 pagesDepreciationAMIN BUHARI ABDUL KHADERNo ratings yet

- Chapter 8 Adjusting Entries 2 SHSDocument81 pagesChapter 8 Adjusting Entries 2 SHSTep TepNo ratings yet

- Caso 3 y 4 PDFDocument9 pagesCaso 3 y 4 PDFJanetCrucesNo ratings yet

- Liquid Ratios GuideDocument12 pagesLiquid Ratios GuideMAHI LADNo ratings yet

- CHAPTER - 1-WPS - Office (1) (Repaired)Document27 pagesCHAPTER - 1-WPS - Office (1) (Repaired)Akash Pawaskar100% (1)

- 2019 PFRS For Se - Jack Margie Farm Inc For PrintingDocument16 pages2019 PFRS For Se - Jack Margie Farm Inc For PrintingJenver BuenaventuraNo ratings yet

- Conceptual FrameworkDocument125 pagesConceptual FrameworkJonah Marie Therese Burlaza50% (4)

- Problem 3-5B Adjusted Trial Balance SolutionDocument4 pagesProblem 3-5B Adjusted Trial Balance SolutionAlba LunaNo ratings yet

- Real Estate Finance Midterm SolutionsDocument7 pagesReal Estate Finance Midterm SolutionsJiayu JinNo ratings yet

- Analysis of Anuual Report of Tata Consultancy Services (TCS) 2019Document17 pagesAnalysis of Anuual Report of Tata Consultancy Services (TCS) 2019AparnaNo ratings yet

- Audit of Cash and Cash EquivalentsDocument9 pagesAudit of Cash and Cash Equivalentspatricia100% (1)

- MODULE 2 - BUSINESS ACCOUNTING RevisedDocument16 pagesMODULE 2 - BUSINESS ACCOUNTING RevisedArchill YapparconNo ratings yet

- CF TTR Quiz-1 SolutionDocument5 pagesCF TTR Quiz-1 SolutionNitesh BurnwalNo ratings yet

- Suggested Answer CAP II December 2016Document88 pagesSuggested Answer CAP II December 2016Nirmal ShresthaNo ratings yet

- Trial Balance and Financial StatementsDocument18 pagesTrial Balance and Financial StatementsJasmine Merthel Masmila ObstaculoNo ratings yet

- Also Hy2023 en VIDocument21 pagesAlso Hy2023 en VImihirbhojani603No ratings yet

- Chapter 21 - Investment PropertyDocument3 pagesChapter 21 - Investment PropertyXiena67% (3)

- What Is Value Investing?Document10 pagesWhat Is Value Investing?Navaraj BaniyaNo ratings yet

- Advanced Accounting: Chapter 4: Consolidated Financial Statements After AcquisitionDocument24 pagesAdvanced Accounting: Chapter 4: Consolidated Financial Statements After AcquisitionuseptrianiNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)