You might also like

- Futures Trading Strategies: Enter and Exit the Market Like a Pro with Proven and Powerful Techniques For ProfitsFrom EverandFutures Trading Strategies: Enter and Exit the Market Like a Pro with Proven and Powerful Techniques For ProfitsRating: 1 out of 5 stars1/5 (1)

- Task-1 Market ResearchDocument2 pagesTask-1 Market ResearchDevyanshi HadaNo ratings yet

- ACCT3203 Week 5 Tutorial Questions Customer Profitability Analysis & Quality S2 2022Document12 pagesACCT3203 Week 5 Tutorial Questions Customer Profitability Analysis & Quality S2 2022Jingwen YangNo ratings yet

- Meaning of DerivDocument21 pagesMeaning of DerivNikhil Mukhi100% (1)

- Answer: 1. Stock ExchangeDocument4 pagesAnswer: 1. Stock Exchangeshayn delapenaNo ratings yet

- FINANCIAL MARKET REPORTING (Autosaved)Document36 pagesFINANCIAL MARKET REPORTING (Autosaved)Villanueva, Jane G.No ratings yet

- Derivatives Note SeminarDocument7 pagesDerivatives Note SeminarCA Vikas NevatiaNo ratings yet

- Understanding Derivatives in 40 CharactersDocument10 pagesUnderstanding Derivatives in 40 CharactersSanjai SivañanthamNo ratings yet

- DerivativesDocument8 pagesDerivativescatprep2023No ratings yet

- Derivatives Market IntroductionDocument4 pagesDerivatives Market IntroductionNg Jian LongNo ratings yet

- Lecture Notes Week 02Document4 pagesLecture Notes Week 02Mariana garcia perezNo ratings yet

- What Is A Derivative?Document65 pagesWhat Is A Derivative?devNo ratings yet

- Unit - 2Document39 pagesUnit - 2DivyanshuNo ratings yet

- Financial Market ReportingDocument36 pagesFinancial Market ReportingVillanueva, Jane G.No ratings yet

- Derivative MarketsDocument8 pagesDerivative Marketsvijay_vmrNo ratings yet

- What Are DerivativesDocument7 pagesWhat Are DerivativesMohit ModiNo ratings yet

- Derivatives Analysis and Valuation: Learning OutcomesDocument62 pagesDerivatives Analysis and Valuation: Learning OutcomesAshutosh ModiNo ratings yet

- Presentation On Underlying Market: BY:-DHAIRYA (03) KANIKA (47) DARSHANDocument30 pagesPresentation On Underlying Market: BY:-DHAIRYA (03) KANIKA (47) DARSHANDhairyaa BhardwajNo ratings yet

- What is a derivativeDocument36 pagesWhat is a derivativeMahesh ShahNo ratings yet

- Understanding Derivatives MarketsDocument30 pagesUnderstanding Derivatives MarketsDhairyaa BhardwajNo ratings yet

- Derivatives 1 2021Document71 pagesDerivatives 1 2021Gragnor Pride100% (1)

- Project On Futures and OptionsDocument19 pagesProject On Futures and Optionsaanu1234No ratings yet

- FDM (Unit I-V)Document27 pagesFDM (Unit I-V)KathiravanNo ratings yet

- Risk Management with DerivativesDocument7 pagesRisk Management with DerivativesYogesh GovindNo ratings yet

- Understanding the Derivatives MarketDocument39 pagesUnderstanding the Derivatives MarketVillanueva, Jane G.No ratings yet

- Introduction To Cash & Derivative Market-AnDocument63 pagesIntroduction To Cash & Derivative Market-AnDrashti ShahNo ratings yet

- Market For Currency FuturesDocument35 pagesMarket For Currency Futuresvidhya priyaNo ratings yet

- F D Unit 2Document9 pagesF D Unit 2Diksha KumariNo ratings yet

- Derivative TradingDocument134 pagesDerivative TradingVinod PapuNo ratings yet

- Derivatives Analysis and Valuation: Learning OutcomesDocument64 pagesDerivatives Analysis and Valuation: Learning OutcomesPravesh PangeniNo ratings yet

- The Definitions, Mechanisms and Trading of Futures ContractsDocument20 pagesThe Definitions, Mechanisms and Trading of Futures Contractsnipul_agrawalNo ratings yet

- DarivativesDocument75 pagesDarivativesapi-316719777No ratings yet

- Techniques and Tools of Risk Management Unit III-DBM,OU (Forwards & FuturesDocument99 pagesTechniques and Tools of Risk Management Unit III-DBM,OU (Forwards & FuturesChham Chha Virak VccNo ratings yet

- Derivatives Learning ResourcesDocument13 pagesDerivatives Learning ResourcesPrasadNo ratings yet

- WORK SHEET - Financial Derivatives: Q1) Enumerate The Basic Differences Between Forward and Futures ContractsDocument5 pagesWORK SHEET - Financial Derivatives: Q1) Enumerate The Basic Differences Between Forward and Futures ContractsBhavesh RathiNo ratings yet

- Types of Financial DerivativesDocument14 pagesTypes of Financial DerivativesSolange TannouryNo ratings yet

- OTC Derivatives ModuleDocument7 pagesOTC Derivatives ModulehareshNo ratings yet

- Icici Securities Project ReportDocument22 pagesIcici Securities Project ReportbruhNo ratings yet

- Unit 2 FDDocument39 pagesUnit 2 FDraj kumarNo ratings yet

- DerivativesDocument14 pagesDerivativessb_rathi27feb2239No ratings yet

- Introduction to Derivatives Risk ManagementDocument25 pagesIntroduction to Derivatives Risk ManagementVrutika ShahNo ratings yet

- Futures - Meaning, Types, Mechanism, SEBI GuidelinesDocument49 pagesFutures - Meaning, Types, Mechanism, SEBI GuidelinesKARISHMAAT67% (6)

- FD Unit 1 Q&A (1-23)Document18 pagesFD Unit 1 Q&A (1-23)Vasugi KumarNo ratings yet

- Research and EducationDocument7 pagesResearch and Educationnlpatel22No ratings yet

- Derivatives and Risk Management: What Does Forward Contract MeanDocument9 pagesDerivatives and Risk Management: What Does Forward Contract MeanMd Hafizul HaqueNo ratings yet

- Forex Derivatives in India Its Implications - Currency Futures and Its Implications in Forex TradingDocument23 pagesForex Derivatives in India Its Implications - Currency Futures and Its Implications in Forex TradingamansinghaniaiipmNo ratings yet

- Risk MGMT (Module-II - Chapter 1 & 2)Document10 pagesRisk MGMT (Module-II - Chapter 1 & 2)Kelvin SavaliyaNo ratings yet

- How are futures traded?: Họ và tên: Phạm Ngọc Dung Lớp: A2-Kế toán SBD: 05 Môn: Esp IiDocument4 pagesHow are futures traded?: Họ và tên: Phạm Ngọc Dung Lớp: A2-Kế toán SBD: 05 Môn: Esp Iingoinha89No ratings yet

- Derivative Markets and Instruments: Criticisms of DerivativesDocument10 pagesDerivative Markets and Instruments: Criticisms of DerivativesMayura KatariaNo ratings yet

- Derivatives SYBBI - PPTX FinalDocument70 pagesDerivatives SYBBI - PPTX Finalsmit mestryNo ratings yet

- Trading in Financial MarketsDocument42 pagesTrading in Financial MarketsthandiveNo ratings yet

- Traders in Derivative Market - There Are 3 Types of Traders in The DerivativesDocument6 pagesTraders in Derivative Market - There Are 3 Types of Traders in The DerivativesShahbazHasanNo ratings yet

- Prepared by K.Logasakthi MBA (PH.D) Assist.. Professor VSA School of Management, SalemDocument37 pagesPrepared by K.Logasakthi MBA (PH.D) Assist.. Professor VSA School of Management, SalemRohit OberoiNo ratings yet

- CH 8 Derivatives Analysis & Valuation PDFDocument44 pagesCH 8 Derivatives Analysis & Valuation PDFrbmjainNo ratings yet

- FMO Module 5Document15 pagesFMO Module 5Sonia Dann KuruvillaNo ratings yet

- Classification and Functions of Financial MarketsDocument18 pagesClassification and Functions of Financial MarketsKongskieRicNo ratings yet

- Financial DerivativesDocument10 pagesFinancial DerivativesNitin ChoudharyNo ratings yet

- SampleDocument6 pagesSampleTimy WongNo ratings yet

- Submitted To Submitted By:-Mr. Amit Kumar Neha Deepak Harish Mohit KrishanDocument9 pagesSubmitted To Submitted By:-Mr. Amit Kumar Neha Deepak Harish Mohit KrishanrajatNo ratings yet

- WLH Finance CompilationDocument58 pagesWLH Finance CompilationSandhya S 17240No ratings yet

- Basics of DerivativesDocument27 pagesBasics of DerivativesSweety PawarNo ratings yet

- Chapter 3: Hedging Strategies Using FuturesDocument14 pagesChapter 3: Hedging Strategies Using FuturesDimithri De MeraalNo ratings yet

- Chapter 2: Mechanics of Futures MarketsDocument10 pagesChapter 2: Mechanics of Futures MarketsDimithri De MeraalNo ratings yet

- Homework 4 AnswersDocument3 pagesHomework 4 AnswersDimithri De MeraalNo ratings yet

- HomeWork 3 AnswersDocument2 pagesHomeWork 3 AnswersDimithri De MeraalNo ratings yet

- Homework 5 AnswersDocument4 pagesHomework 5 AnswersDimithri De MeraalNo ratings yet

- Homework 2 AnswersDocument4 pagesHomework 2 AnswersDimithri De MeraalNo ratings yet

- HomeWork 1 AnwersDocument7 pagesHomeWork 1 AnwersDimithri De MeraalNo ratings yet

- Jollisavers Meals TV Ad DeconstructedDocument4 pagesJollisavers Meals TV Ad DeconstructedMa. Rhona Faye MedesNo ratings yet

- Homeroom Guidance: Siyahan Nga Bahin - Modyul 2: An Akon GintikanganDocument10 pagesHomeroom Guidance: Siyahan Nga Bahin - Modyul 2: An Akon GintikangansaraiNo ratings yet

- The Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasDocument24 pagesThe Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasTitan HerdiantoNo ratings yet

- P7112bgm-Catalogueb2010 0811 en A4 FullDocument810 pagesP7112bgm-Catalogueb2010 0811 en A4 FullShri ShriNo ratings yet

- Jurnal Penelitian Dosen Fikom (UNDA) Vol.10 No.2, November 2019, ISSNDocument8 pagesJurnal Penelitian Dosen Fikom (UNDA) Vol.10 No.2, November 2019, ISSNkiki rifkiNo ratings yet

- Urban MarketplaceDocument20 pagesUrban MarketplaceMae LafortezaNo ratings yet

- TS16949 Training OverviewDocument23 pagesTS16949 Training OverviewPraveen CoolNo ratings yet

- Assignment Model Typical QuestionDocument17 pagesAssignment Model Typical Questionjagritiprakash00100No ratings yet

- Assignment 1 Complete The Assignment and Submit It On Moodle. Marks Weightage - 20%Document12 pagesAssignment 1 Complete The Assignment and Submit It On Moodle. Marks Weightage - 20%Shivam SharmaNo ratings yet

- Faculty Handbook MGT FinalDocument48 pagesFaculty Handbook MGT FinalTiwanka MadurangaNo ratings yet

- Factory Accounting RulesDocument61 pagesFactory Accounting RulesMitthu KumarNo ratings yet

- Session 12-Balance of PaymentsDocument19 pagesSession 12-Balance of PaymentsJai GaneshNo ratings yet

- LAW 200 - FINAL PROJECT - Section 8Document6 pagesLAW 200 - FINAL PROJECT - Section 8drive.sami.mym.101No ratings yet

- CRT 3rd Year NewDocument232 pagesCRT 3rd Year NewAkshat agrawalNo ratings yet

- Equity CrowdfundingDocument13 pagesEquity CrowdfundingantonyNo ratings yet

- Borrowing Costs: DefinitionsDocument23 pagesBorrowing Costs: DefinitionsAbdul Sami100% (1)

- Deloitte - ChinaCast EducationDocument75 pagesDeloitte - ChinaCast EducationcorruptioncurrentsNo ratings yet

- INTERVIEW GUIDE For BMADocument6 pagesINTERVIEW GUIDE For BMAJale Ann A. EspañolNo ratings yet

- Pelangi 2019 PDFDocument194 pagesPelangi 2019 PDFTharshanraaj RaajNo ratings yet

- Contracts II AssignmentDocument16 pagesContracts II AssignmentIsha PuthettuNo ratings yet

- Kajaria Ceramics: Production and Consumption Trend of Ceramic Tiles in WorldDocument10 pagesKajaria Ceramics: Production and Consumption Trend of Ceramic Tiles in Worldapi-556903190No ratings yet

- Motion To Reduce BondDocument4 pagesMotion To Reduce Bonderika barbaronaNo ratings yet

- CARGO Establishment ListDocument3 pagesCARGO Establishment ListRanjith PNo ratings yet

- GE Nine-Cell Planning Grid TechniqueDocument10 pagesGE Nine-Cell Planning Grid Techniquevarun rajNo ratings yet

- Financial Literacy Levels of Small Businesses Owners and It Correlation With Firms' Operating PerformanceDocument72 pagesFinancial Literacy Levels of Small Businesses Owners and It Correlation With Firms' Operating PerformanceRod SisonNo ratings yet

- SHEQ Monthly Report SummaryDocument17 pagesSHEQ Monthly Report SummaryArif NugrohoNo ratings yet

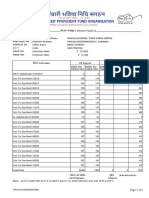

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Sales Receipt: Company Name 123 Main Street Hamilton, OH 44416 (321) 456-7890 Email AddressDocument1 pageSales Receipt: Company Name 123 Main Street Hamilton, OH 44416 (321) 456-7890 Email AddressParas ShardaNo ratings yet