You might also like

- HsieDocument2 pagesHsiejed loverNo ratings yet

- Hang Seng Index: FeaturesDocument2 pagesHang Seng Index: FeaturesAng SHNo ratings yet

- Bse LTD (Bse) : Endow in Pioneering ExchangeDocument26 pagesBse LTD (Bse) : Endow in Pioneering Exchangeshark123No ratings yet

- HSBC Asian Local Bond Index (ALBI)Document17 pagesHSBC Asian Local Bond Index (ALBI)Areeys SyaheeraNo ratings yet

- Vietnam Future Contract and ConclusionDocument4 pagesVietnam Future Contract and ConclusionThu NguyenNo ratings yet

- NSE Annual Report 2021Document444 pagesNSE Annual Report 2021manas choudhuryNo ratings yet

- Viva Voce Presentation (Data Analysis)Document51 pagesViva Voce Presentation (Data Analysis)Abhijeet BirariNo ratings yet

- Nikhil Overview of Indian Stock MarketDocument17 pagesNikhil Overview of Indian Stock MarketPurvesh TaheliyaniNo ratings yet

- Analysis of Indian Stock Market 2009-10Document65 pagesAnalysis of Indian Stock Market 2009-10s_sannit2k9No ratings yet

- KPMG China HK Ipo 2020 Review and OutlookDocument28 pagesKPMG China HK Ipo 2020 Review and Outlookreload2No ratings yet

- NSE Market PulseDocument13 pagesNSE Market PulseArindam ChatterjeeNo ratings yet

- Icici Prudential S P Bse 500 Etf Fof PPT (Investor Version)Document15 pagesIcici Prudential S P Bse 500 Etf Fof PPT (Investor Version)AdityaNarayanSinghNo ratings yet

- Business ResearchDocument38 pagesBusiness ResearchAkanksha SinghNo ratings yet

- Finance ActivityDocument35 pagesFinance Activityayushi mishraNo ratings yet

- Structure of Capital Market: Dr. Deepa Soni Assistant Professor Department of Economics Mlsu (Ucssh) UdaipurDocument5 pagesStructure of Capital Market: Dr. Deepa Soni Assistant Professor Department of Economics Mlsu (Ucssh) UdaipurAnonymous 1ClGHbiT0J0% (1)

- Investor Presentation Q2FY19 VFDocument47 pagesInvestor Presentation Q2FY19 VFNesNosssNo ratings yet

- Financial ServicesDocument10 pagesFinancial ServicesRahul DawarNo ratings yet

- Stock and Commodity Market - Unit II NotesDocument22 pagesStock and Commodity Market - Unit II NotesUtkarsh Tripathi72No ratings yet

- Vanguard Total China Index ETF (HKD: 3169 / RMB: 83169 / USD: 9169)Document2 pagesVanguard Total China Index ETF (HKD: 3169 / RMB: 83169 / USD: 9169)Juan Manuel FigueroaNo ratings yet

- Fundamental and Technical Analysis at Kotak Mahindra Mba Project ReportDocument108 pagesFundamental and Technical Analysis at Kotak Mahindra Mba Project ReportBabasab Patil (Karrisatte)67% (6)

- Stock Exchange in India: Business StatisticsDocument16 pagesStock Exchange in India: Business StatisticsVasu Singal100% (1)

- June 2016 1466427695 126Document3 pagesJune 2016 1466427695 126Shaikh SuhailNo ratings yet

- SR - No Topics 1. 2.: Listing AgreemtsDocument69 pagesSR - No Topics 1. 2.: Listing AgreemtsChandrakanta pandaNo ratings yet

- Vanguard FTSE Developed Europe Index ETF (HKD: 3101 / RMB: 83101 / USD: 9101)Document2 pagesVanguard FTSE Developed Europe Index ETF (HKD: 3101 / RMB: 83101 / USD: 9101)Juan Manuel FigueroaNo ratings yet

- EQUITY ANALYSIS WITH REPECT TO Automobile SectorDocument83 pagesEQUITY ANALYSIS WITH REPECT TO Automobile SectorSuraj DubeyNo ratings yet

- Bse & Nse IndicesDocument19 pagesBse & Nse IndicesAjit RunwalNo ratings yet

- Free Float IndexDocument8 pagesFree Float IndexJaishalNo ratings yet

- 1.1. Industry ProfileDocument104 pages1.1. Industry ProfilebibinmeNo ratings yet

- Rieview of Literature For Derivatives ProjectDocument42 pagesRieview of Literature For Derivatives Projectcozycap82% (22)

- Project Work Subject-Business Studies Topic-Stock Exchange: FlowDocument22 pagesProject Work Subject-Business Studies Topic-Stock Exchange: FlowSnehil ChundawatNo ratings yet

- A Report OnDocument17 pagesA Report OnsachinktNo ratings yet

- Bombay Stock ExchangeDocument19 pagesBombay Stock ExchangenarendramoreNo ratings yet

- 1 305pm - 9.P.WilliamRobert-11.6.16Document6 pages1 305pm - 9.P.WilliamRobert-11.6.16Andy KNo ratings yet

- Intangible Asset Market Value Study: Ocean TomoDocument4 pagesIntangible Asset Market Value Study: Ocean TomoValter FariaNo ratings yet

- Presentation On: Hang SengDocument8 pagesPresentation On: Hang SengRahul ShakyaNo ratings yet

- MBA Project On Fundamental and Technical Analysis of Kotak BankDocument109 pagesMBA Project On Fundamental and Technical Analysis of Kotak BankSneha MaskaraNo ratings yet

- IndexDocument1 pageIndexSonal GrewalNo ratings yet

- FTSE Emerging Markets China A Inclusion IndexesDocument5 pagesFTSE Emerging Markets China A Inclusion IndexesajNo ratings yet

- Investor Presentation Q3FY19 VFDocument49 pagesInvestor Presentation Q3FY19 VFNesNosssNo ratings yet

- Bombay Stock ExchangeDocument16 pagesBombay Stock ExchangeabhasaNo ratings yet

- Sumanth Interim ReportDocument19 pagesSumanth Interim ReportVinod Kumar EmmadiNo ratings yet

- How The Sensex Is CalculatedDocument2 pagesHow The Sensex Is CalculatedPratik KapadiaNo ratings yet

- How The Sensex Is CalculatedDocument3 pagesHow The Sensex Is CalculatedMv BarathNo ratings yet

- Capital Markets Secondary MarketsDocument32 pagesCapital Markets Secondary Marketsmedha_mehtaNo ratings yet

- Regional Focus Report: India Focused FundsDocument5 pagesRegional Focus Report: India Focused FundsHumerahhNo ratings yet

- List of Tables: Sr. No Page NoDocument49 pagesList of Tables: Sr. No Page Nosatyamyes01No ratings yet

- Index CalculationDocument3 pagesIndex CalculationArpit RamsinghaniNo ratings yet

- A Study On Equity Analysis With Reference To It & BanksDocument67 pagesA Study On Equity Analysis With Reference To It & BanksjassubharathiNo ratings yet

- Annual Report: Stock Code: 388Document232 pagesAnnual Report: Stock Code: 388GINYNo ratings yet

- National Stock ExchangeDocument7 pagesNational Stock ExchangeTuba HamidNo ratings yet

- National Stock ExchangeDocument7 pagesNational Stock ExchangeTuba HamidNo ratings yet

- What Is SENSEX?: Company Name (Industry)Document3 pagesWhat Is SENSEX?: Company Name (Industry)Inza NsaNo ratings yet

- An Analysis of Impact of FDI On Indian Stock Market: With Special Reference To Bse-Sensex and Nse-Cnx NiftyDocument6 pagesAn Analysis of Impact of FDI On Indian Stock Market: With Special Reference To Bse-Sensex and Nse-Cnx NiftyRiyaz AliNo ratings yet

- Presented By: Ankit JainDocument17 pagesPresented By: Ankit Jainakki00009No ratings yet

- Indian Capital MarketDocument19 pagesIndian Capital MarketdollieNo ratings yet

- $mmer Project-Sharekhan1 (Repaired) ALL PAGESDocument123 pages$mmer Project-Sharekhan1 (Repaired) ALL PAGESHarshil BadaniNo ratings yet

- A Comparative Study of Bombay Stock Exchange (BSE) and National Stock Exchange (NSE)Document6 pagesA Comparative Study of Bombay Stock Exchange (BSE) and National Stock Exchange (NSE)Nitesh TripathyNo ratings yet

- Stock Market Income Genesis: Internet Business Genesis Series, #8From EverandStock Market Income Genesis: Internet Business Genesis Series, #8No ratings yet

- Distributing (S) Shares Explained: Blackrock Global Funds (BGF)Document2 pagesDistributing (S) Shares Explained: Blackrock Global Funds (BGF)Edwin ChanNo ratings yet

- First Product Tracking Hang Seng China Enterprises Smart Index Debuts On Shenzhen Stock ExchangeDocument4 pagesFirst Product Tracking Hang Seng China Enterprises Smart Index Debuts On Shenzhen Stock ExchangeEdwin ChanNo ratings yet

- Technical Notice: Distribution in Specie of The Issued Shares of Wharf REICDocument3 pagesTechnical Notice: Distribution in Specie of The Issued Shares of Wharf REICEdwin ChanNo ratings yet

- Reducing Risk in International PortfoliosDocument4 pagesReducing Risk in International PortfoliosEdwin ChanNo ratings yet

- 2017 Investor Pulse: Hong KongDocument24 pages2017 Investor Pulse: Hong KongEdwin ChanNo ratings yet

- Bii Global Investment Outlook q4 2017 AxjDocument12 pagesBii Global Investment Outlook q4 2017 AxjEdwin ChanNo ratings yet

- Kosdaq 150 Methodology Guide: November 2020Document13 pagesKosdaq 150 Methodology Guide: November 2020Edwin ChanNo ratings yet

- Bloomberg Barclays Methodology1Document126 pagesBloomberg Barclays Methodology1Edwin ChanNo ratings yet

- Bloomberg: US Equity Corporate Action MethodologyDocument32 pagesBloomberg: US Equity Corporate Action MethodologyEdwin ChanNo ratings yet

- 1 1+Basic+Methodology+for+KRX+Indices (2011)Document8 pages1 1+Basic+Methodology+for+KRX+Indices (2011)Edwin ChanNo ratings yet

- Kospi 200 Index Methodology Guide: November 2020Document16 pagesKospi 200 Index Methodology Guide: November 2020Edwin ChanNo ratings yet

- S&P/KRX Exchanges Index: MethodologyDocument15 pagesS&P/KRX Exchanges Index: MethodologyEdwin ChanNo ratings yet

- AWORLDS QUARTERLY-DAILYData-EUR StocksWeight 20201231Document17 pagesAWORLDS QUARTERLY-DAILYData-EUR StocksWeight 20201231Edwin ChanNo ratings yet

- F-Kosdaq 150 Methodology Guide: June 2016Document5 pagesF-Kosdaq 150 Methodology Guide: June 2016Edwin ChanNo ratings yet

- Index Reconstitution Calendar 2021: About Asia Index Private LimitedDocument2 pagesIndex Reconstitution Calendar 2021: About Asia Index Private LimitedEdwin ChanNo ratings yet

- CDSL-Foreign Investment Monitoring-List of Companies-05022021Document65 pagesCDSL-Foreign Investment Monitoring-List of Companies-05022021Edwin ChanNo ratings yet

- Methodology SP Bse IndicesDocument57 pagesMethodology SP Bse IndicesEdwin ChanNo ratings yet

- SAP FICO Course Content by Archon Tech SolutionsDocument4 pagesSAP FICO Course Content by Archon Tech SolutionsCorpsalesNo ratings yet

- PetrofinDocument30 pagesPetrofinergonblognewsNo ratings yet

- PLI Wise Unit Wise CLCSS Data As On September 30 2014Document1,089 pagesPLI Wise Unit Wise CLCSS Data As On September 30 2014Neeraj AgarwalNo ratings yet

- June 15, 2009 - Morning CallDocument3 pagesJune 15, 2009 - Morning Callkkeenan5008475No ratings yet

- ACCTG1 Chapter 5Document6 pagesACCTG1 Chapter 5Mark Kevin JavierNo ratings yet

- Managerial Accounting Tools For Business Canadian 3rd Edition Weygandt Test BankDocument54 pagesManagerial Accounting Tools For Business Canadian 3rd Edition Weygandt Test Bankodileguinevereqgpc5d100% (24)

- Case 3 - Group 5, Section 2Document8 pagesCase 3 - Group 5, Section 2sd_tataNo ratings yet

- Notes - Cash Flow Statement and ProblemsDocument4 pagesNotes - Cash Flow Statement and ProblemsDhruv MalhotraNo ratings yet

- Datatreasury Corporation v. Wells Fargo & Company Et Al - Document No. 351Document12 pagesDatatreasury Corporation v. Wells Fargo & Company Et Al - Document No. 351Justia.comNo ratings yet

- Credit MGT TraineesDocument20 pagesCredit MGT TraineesTewodros2014No ratings yet

- 1557126657969Document10 pages1557126657969Pankaj AkadkarNo ratings yet

- 1 - Introduction of Islamic FinanceDocument21 pages1 - Introduction of Islamic FinanceShoaibNo ratings yet

- Cross Currency Basis - RBS PDFDocument7 pagesCross Currency Basis - RBS PDFJaz MNo ratings yet

- CFA L1 2023 FSA Corporate Issuers Fintree JuiceNotesDocument92 pagesCFA L1 2023 FSA Corporate Issuers Fintree JuiceNotesThanh Nguyễn100% (3)

- BFM Module A in Very BriefDocument15 pagesBFM Module A in Very BriefMOHAMED FAROOKNo ratings yet

- Assets Liabilities Statments F 349 For GuarantorDocument9 pagesAssets Liabilities Statments F 349 For GuarantorPrakash JNo ratings yet

- Ca BK Xo JKjqi L4 H V8Document3 pagesCa BK Xo JKjqi L4 H V8Parag SarodeNo ratings yet

- Investment Banking in IndiaDocument62 pagesInvestment Banking in IndiaRajesh Mejari100% (9)

- Log 20220919Document23 pagesLog 20220919lutfi sipatrickNo ratings yet

- Topical Depreciation Q 2014-2019Document48 pagesTopical Depreciation Q 2014-2019ibbbi shkhNo ratings yet

- Yes Bank Account Application DetailsDocument2 pagesYes Bank Account Application DetailsManohar NMNo ratings yet

- Pfrs 16 LeasesDocument4 pagesPfrs 16 LeasesR.A.No ratings yet

- Chapter 3 - Problem SetDocument14 pagesChapter 3 - Problem SetNetflix 0001No ratings yet

- FINANCIAL MANAGEMENT Chapter 2Document37 pagesFINANCIAL MANAGEMENT Chapter 2JackNo ratings yet

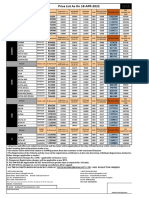

- Price List As On 18-APR-2022: VariantDocument1 pagePrice List As On 18-APR-2022: VariantKolkata Jyote MotorsNo ratings yet

- Prasad Bank StatementDocument7 pagesPrasad Bank StatementPrasad ChallagollaNo ratings yet

- History of Canara BankDocument8 pagesHistory of Canara BankVikas Tirmale100% (1)

- Intrinsic Value Spreadsheet 1Document12 pagesIntrinsic Value Spreadsheet 1Soham AherNo ratings yet

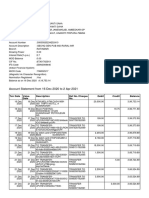

- Account Statement From 16 Dec 2020 To 2 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 16 Dec 2020 To 2 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSuhan SahaNo ratings yet

- Chapetr On Borrowing Cost - TP GhoshDocument15 pagesChapetr On Borrowing Cost - TP GhoshGeorgeNo ratings yet