You might also like

- Bai Type Code GuideDocument31 pagesBai Type Code Guideswathipotla100% (1)

- How To Pay by Western Union Quick Pay?Document1 pageHow To Pay by Western Union Quick Pay?NabilAbNo ratings yet

- David Jennings: Debit Account Transactions Date Description Type Amount Available Matthew SteversonDocument4 pagesDavid Jennings: Debit Account Transactions Date Description Type Amount Available Matthew Steversondolapo BalogunNo ratings yet

- Free Virtual Debit Card - NO Fees - OpenbankDocument4 pagesFree Virtual Debit Card - NO Fees - OpenbankJelo BagzNo ratings yet

- Payments BankDocument33 pagesPayments BankAdnan patelNo ratings yet

- Sending and Receiving Wire Transfers - CIBCDocument3 pagesSending and Receiving Wire Transfers - CIBCGopi NathNo ratings yet

- SEMINAR CryptocurrencyDocument20 pagesSEMINAR CryptocurrencyKAMAKYA SINGHNo ratings yet

- New Paypal Customer Welcome KitDocument6 pagesNew Paypal Customer Welcome KitSharvin RajNo ratings yet

- StatementDocument5 pagesStatementanikaNo ratings yet

- #1210 Nilson ReportDocument18 pages#1210 Nilson ReportChristian Javier VillafuerteNo ratings yet

- Doing Business in The Kingdom of Saudi Arabia: A Tax and Legal GuideDocument26 pagesDoing Business in The Kingdom of Saudi Arabia: A Tax and Legal GuideDiwakar RoyNo ratings yet

- OpTransactionHistory23 03 2020 PDFDocument5 pagesOpTransactionHistory23 03 2020 PDFRINKU KATHURIYANo ratings yet

- Your Adv Plus Banking: Account SummaryDocument8 pagesYour Adv Plus Banking: Account SummaryFrancy MartinezNo ratings yet

- Omni Fintech Digital Payments and Banking A Digital RevolutionDocument11 pagesOmni Fintech Digital Payments and Banking A Digital RevolutionvicgreerNo ratings yet

- Payermax: Cross Border Payment SolutionDocument14 pagesPayermax: Cross Border Payment SolutionCharit SharmaNo ratings yet

- Setting Up Payment Gateway in IndiaDocument16 pagesSetting Up Payment Gateway in Indiaps100% (1)

- payerStatementsByDate PDFDocument5 pagespayerStatementsByDate PDFд. ЭркаNo ratings yet

- Making India A Global Fintech HubDocument36 pagesMaking India A Global Fintech Hubunknown4080No ratings yet

- Statement of Accounts: Today's StatementsDocument1 pageStatement of Accounts: Today's Statementsхуивпи дрилоNo ratings yet

- Rek Koran PT HAI Mandiri 2022Document115 pagesRek Koran PT HAI Mandiri 2022wahyu suhartono100% (1)

- Fintech Mondaq GuideDocument10 pagesFintech Mondaq GuideAmira DhawanNo ratings yet

- The Financial Technology Law Review - The Law ReviewsDocument8 pagesThe Financial Technology Law Review - The Law ReviewsAmira DhawanNo ratings yet

- ITLaw 1642Document7 pagesITLaw 1642Liya FathimaNo ratings yet

- Payment Banks: Digital Revolution in Indian Banking SystemDocument7 pagesPayment Banks: Digital Revolution in Indian Banking SystemResearch SolutionsNo ratings yet

- FINTECHSDocument3 pagesFINTECHSMahima SharmaNo ratings yet

- Presentation For Viva: Sagar Srinivas Mandal HPGD/JL17/2564Document61 pagesPresentation For Viva: Sagar Srinivas Mandal HPGD/JL17/2564Mandal SagarNo ratings yet

- DIGITALLENDINGDocument151 pagesDIGITALLENDINGDirector Bal JyotiNo ratings yet

- Fintech ScopeDocument5 pagesFintech Scopearpit85No ratings yet

- Fin TechDocument7 pagesFin TechHarsh ChaudharyNo ratings yet

- Legal Updates For The Month of December, 2023Document6 pagesLegal Updates For The Month of December, 2023Parina TyagiNo ratings yet

- HDFC Bank Literature ReviewDocument8 pagesHDFC Bank Literature Reviewc5e83cmh100% (1)

- Payments BankDocument14 pagesPayments BankDurjoy BhattacharjeeNo ratings yet

- Payment and Settlement SystemDocument16 pagesPayment and Settlement Systemchitra_shresthaNo ratings yet

- Discussion Paper On Aadhaar Based Financial InclusionDocument24 pagesDiscussion Paper On Aadhaar Based Financial Inclusionreddy1151No ratings yet

- Fintech Report 2016Document38 pagesFintech Report 2016CrowdfundInsiderNo ratings yet

- Discussion Paper On Aadhaar Based Financial InclusionDocument26 pagesDiscussion Paper On Aadhaar Based Financial Inclusionharry04hNo ratings yet

- Financial Inclusion-Role of Payment Banks in India: IRA-International Journal of Management & Social SciencesDocument6 pagesFinancial Inclusion-Role of Payment Banks in India: IRA-International Journal of Management & Social Sciencesmonica niroliaNo ratings yet

- Banking & Economy PDF - August 2021 by AffairsCloud 1Document124 pagesBanking & Economy PDF - August 2021 by AffairsCloud 1premNo ratings yet

- AIFinanceBanking Report WQ PDFDocument41 pagesAIFinanceBanking Report WQ PDFTrishala PandeyNo ratings yet

- Assignment 1 Development in Banking Sector From 2010 Till 2023Document5 pagesAssignment 1 Development in Banking Sector From 2010 Till 2023Komal RautNo ratings yet

- Role of Payments BankDocument16 pagesRole of Payments BankAstik TripathiNo ratings yet

- Fintech For The UnderservedDocument36 pagesFintech For The UnderservedDaboNo ratings yet

- Payment Bank - A Need of Digital India: Abhinav National Monthly Refereed Journal of Research inDocument5 pagesPayment Bank - A Need of Digital India: Abhinav National Monthly Refereed Journal of Research inmonica niroliaNo ratings yet

- BS Adfree 19.05.2019Document9 pagesBS Adfree 19.05.2019Battula Surender SudhamaNo ratings yet

- MRAA-Assignment 2Document23 pagesMRAA-Assignment 2NAMAN AGARWALNo ratings yet

- Icici Bank LTDDocument11 pagesIcici Bank LTDIndu yadavNo ratings yet

- BANk CIA1.2 1720253Document14 pagesBANk CIA1.2 1720253Aashish mishraNo ratings yet

- Banking Awareness: What Are The Reasons That Lead To Nationalisation of Banks ?Document5 pagesBanking Awareness: What Are The Reasons That Lead To Nationalisation of Banks ?Furin KatoNo ratings yet

- Key Asks by The Payments IndustryDocument8 pagesKey Asks by The Payments IndustrySarthakNo ratings yet

- Impact of Payment Banks in Indian Financial SystemDocument6 pagesImpact of Payment Banks in Indian Financial SystemNithin JoseNo ratings yet

- Impact of Technological Changes On Customer: Experience in Banking Sector-A Study of Select Banks in Madhya PradeshDocument12 pagesImpact of Technological Changes On Customer: Experience in Banking Sector-A Study of Select Banks in Madhya PradeshSiddharthJainNo ratings yet

- Ezetap Caselet Case Study PDFDocument12 pagesEzetap Caselet Case Study PDFSaurabh KumarNo ratings yet

- Content For Axis Bank and FreechargeDocument3 pagesContent For Axis Bank and FreechargeAryanSinghNo ratings yet

- Beepedia Weekly Current Affairs (Beepedia) 1st-8th June 2023Document47 pagesBeepedia Weekly Current Affairs (Beepedia) 1st-8th June 2023Sahil KalerNo ratings yet

- Aadhaar in The Financial World 06032014Document14 pagesAadhaar in The Financial World 06032014ykbharti101No ratings yet

- In The Partial Fulfillment of The Requirement For The Award of Degree inDocument17 pagesIn The Partial Fulfillment of The Requirement For The Award of Degree inMohmmedKhayyumNo ratings yet

- FinTech in IndiaDocument6 pagesFinTech in IndiaMARPU RAVITEJANo ratings yet

- Payment and Settlements in India-ExamPundit FinalDocument8 pagesPayment and Settlements in India-ExamPundit FinalUjjwal MishraNo ratings yet

- Ledex Final SudhaDocument28 pagesLedex Final SudhaVijay Srinivas KukkalaNo ratings yet

- Transaction ProcessingDocument25 pagesTransaction ProcessingAmeerul HasanNo ratings yet

- Chapter - 3 Theoretical FrameworkDocument9 pagesChapter - 3 Theoretical FrameworkSalim ShaNo ratings yet

- HDFC Chapter 1 and 3Document66 pagesHDFC Chapter 1 and 3sudhakar kethanaNo ratings yet

- Digital Banks - A Proposal For Licensing and Regulatory Regime For IndiaDocument50 pagesDigital Banks - A Proposal For Licensing and Regulatory Regime For IndiaVignesh PalaniNo ratings yet

- ARTICLEDocument4 pagesARTICLEAmit MaliNo ratings yet

- Banking & Insurance LawDocument21 pagesBanking & Insurance LawDevansh SinghNo ratings yet

- Capital Leases vs. Operating Leases - What's The Difference? Which One Should I Use?Document32 pagesCapital Leases vs. Operating Leases - What's The Difference? Which One Should I Use?nethrahjNo ratings yet

- Opportunities and Challenges of FintechDocument7 pagesOpportunities and Challenges of FintechMayuri RawatNo ratings yet

- Opportunities and Challenges of FinTech PDFDocument7 pagesOpportunities and Challenges of FinTech PDFviadjbvdNo ratings yet

- Final Black BookDocument27 pagesFinal Black Bookruanonlineservices2023No ratings yet

- The Changing Face of Financial Services Growth of Fintech in India v2Document54 pagesThe Changing Face of Financial Services Growth of Fintech in India v2priyxna07No ratings yet

- Mb206409lidiask - PDF 1.5Document81 pagesMb206409lidiask - PDF 1.5bharath reddyNo ratings yet

- Dissertation On Banking Law in IndiaDocument6 pagesDissertation On Banking Law in IndiaWriteMyApaPaperSingapore100% (1)

- An Ecommerce Association of India InitiativeDocument20 pagesAn Ecommerce Association of India InitiativeVipul SharmaNo ratings yet

- Tybaf - Dhruvil Jain - 038Document5 pagesTybaf - Dhruvil Jain - 038DhruviNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Billing Statement: Yosa Perdana PutraDocument2 pagesBilling Statement: Yosa Perdana PutraJAGABUINo ratings yet

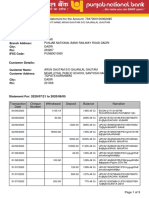

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument11 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceavnish sharmaNo ratings yet

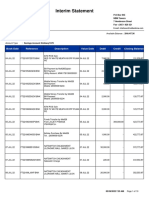

- Interim Statement: Book Date Debit Credit Reference Description Value Date Closing BalanceDocument10 pagesInterim Statement: Book Date Debit Credit Reference Description Value Date Closing BalanceEstherNo ratings yet

- Start Path and CB Insights 2019 TrendsDocument5 pagesStart Path and CB Insights 2019 TrendsSiddhant AggarwalNo ratings yet

- 01 Apr 2022 - 02 Sep 2022Document27 pages01 Apr 2022 - 02 Sep 2022Akash chaudhariNo ratings yet

- Ebill Jul2023 1.75816821Document8 pagesEbill Jul2023 1.75816821Koh Pei CheeNo ratings yet

- A Study On Consumer Satisfaction Towards Google Pay in Madurai CityDocument5 pagesA Study On Consumer Satisfaction Towards Google Pay in Madurai CityKamali ValliNo ratings yet

- Invoice: Law Society of KenyaDocument1 pageInvoice: Law Society of Kenyamotego 1No ratings yet

- Arun Gautam PDFDocument3 pagesArun Gautam PDFRohit kumarNo ratings yet

- LoadCentral Payment SolutionsDocument5 pagesLoadCentral Payment SolutionsJacques Andre Collantes BeaNo ratings yet

- WebTicket Indemnity FormDocument1 pageWebTicket Indemnity FormTaif KhanNo ratings yet

- PCI CP v1 1 ROC Reporting Template Logical FormDocument78 pagesPCI CP v1 1 ROC Reporting Template Logical FormVasanth KumarNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument50 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceavnish sharmaNo ratings yet

- Cyber Security Intelligence and Ethereum Blockchain Technology For E-CommerceDocument6 pagesCyber Security Intelligence and Ethereum Blockchain Technology For E-CommerceWARSE JournalsNo ratings yet