You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Distance Learning - IfRS For Telecoms Module OneDocument29 pagesDistance Learning - IfRS For Telecoms Module OneFiras AbsaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- IFRS in Your Pocket 2016 PDFDocument120 pagesIFRS in Your Pocket 2016 PDFPiyush Shah100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- PWC Tiag Perspectives On Ifrs 15Document4 pagesPWC Tiag Perspectives On Ifrs 15Firas AbsaNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Effect Study Ifric13 enDocument21 pagesEffect Study Ifric13 enFiras AbsaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Industry Telecom IFRICDocument16 pagesIndustry Telecom IFRICFiras AbsaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Us Gaap vs. Ifrs: The Basics: TelecommunicationsDocument52 pagesUs Gaap vs. Ifrs: The Basics: TelecommunicationsFiras AbsaNo ratings yet

- The Cost of Complexity For Telecoms: and How Companies Can Reduce ItDocument20 pagesThe Cost of Complexity For Telecoms: and How Companies Can Reduce ItFiras AbsaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Accounting Under IFRS Telecoms O 1001 PDFDocument100 pagesAccounting Under IFRS Telecoms O 1001 PDFnidhikulkarniNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Distance Learning - IfRS For Telecoms Module OneDocument29 pagesDistance Learning - IfRS For Telecoms Module OneFiras AbsaNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Applying Leases Telcos June2016Document17 pagesApplying Leases Telcos June2016Firas AbsaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- FinancialReportingBriefs 01395-171US 30march2017Document11 pagesFinancialReportingBriefs 01395-171US 30march2017Firas AbsaNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Opting In:: How To Win Employee Partners in Mobile Data AnalyticsDocument9 pagesOpting In:: How To Win Employee Partners in Mobile Data AnalyticsFiras AbsaNo ratings yet

- Applying IFRS Revised Revenue Recognition Proposal - Telecoms PDFDocument16 pagesApplying IFRS Revised Revenue Recognition Proposal - Telecoms PDFmymle1No ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Candidate Bulletin: Nformation For PplicantsDocument34 pagesCandidate Bulletin: Nformation For PplicantsFiras AbsaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- State of Nevada Department of Business & Industry Division of Mortgage LendingDocument30 pagesState of Nevada Department of Business & Industry Division of Mortgage LendingFiras AbsaNo ratings yet

- Srec Proj CalcDocument8 pagesSrec Proj CalcFiras AbsaNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Request For Advisory Evaluation 07 14Document4 pagesRequest For Advisory Evaluation 07 14Firas AbsaNo ratings yet

- Tri Solar PDF1Document23 pagesTri Solar PDF1Firas AbsaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- State of Nevada Department of Business & Industry Division of Mortgage LendingDocument30 pagesState of Nevada Department of Business & Industry Division of Mortgage LendingFiras AbsaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Final Annual PV Report Betl Apr09 Mar10Document18 pagesFinal Annual PV Report Betl Apr09 Mar10Firas AbsaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Drywall Feasibility Study 1Document31 pagesDrywall Feasibility Study 1Firas AbsaNo ratings yet

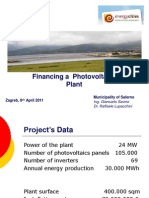

- Financing 24mw-Power-Plant Salerno Savino 2011Document10 pagesFinancing 24mw-Power-Plant Salerno Savino 2011Firas AbsaNo ratings yet

- 314 1011 1 PBDocument11 pages314 1011 1 PBaerosolsynthesisNo ratings yet

- Business Guide Power SunDocument114 pagesBusiness Guide Power SunFiras AbsaNo ratings yet

- Accountancy ImpQ CH04 Admission of A Partner 01Document18 pagesAccountancy ImpQ CH04 Admission of A Partner 01praveentyagiNo ratings yet

- Finance Overview:: Financial Accounting (Fi)Document38 pagesFinance Overview:: Financial Accounting (Fi)Suraj MohapatraNo ratings yet

- Commerce 2004Document50 pagesCommerce 2004shtasneemNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Kieso IFRS4 TB ch02Document67 pagesKieso IFRS4 TB ch023ooobd1234No ratings yet

- Finance - For Non-Finance - ExecutivesDocument4 pagesFinance - For Non-Finance - Executivesabhimani5472No ratings yet

- Management Accounting764 eVyE8h3I7eDocument3 pagesManagement Accounting764 eVyE8h3I7eABHINAV AGRAWALNo ratings yet

- Acca Ethics and Professionalism.Document22 pagesAcca Ethics and Professionalism.abirking50% (2)

- Penerapan PSAK 73 - MaterialDocument77 pagesPenerapan PSAK 73 - Materialni made safitriNo ratings yet

- 4.1-Hortizontal/Trends Analysis: Chapter No # 4Document32 pages4.1-Hortizontal/Trends Analysis: Chapter No # 4Sadi ShahzadiNo ratings yet

- Chapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeDocument9 pagesChapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeAnna TaylorNo ratings yet

- Understanding Accruals R12 05012013Document58 pagesUnderstanding Accruals R12 05012013prasanthbab7128No ratings yet

- DivyanshuJoshi 202221020 BasicsOfAccounting Ch1Document10 pagesDivyanshuJoshi 202221020 BasicsOfAccounting Ch1Divyanshu JoshiNo ratings yet

- Drills - Keep or DropDocument4 pagesDrills - Keep or DropKHAkadsbdhsgNo ratings yet

- Accounting PDFDocument10 pagesAccounting PDFAhmer NaeemNo ratings yet

- Understanding Cash Flows StaDocument30 pagesUnderstanding Cash Flows StaAshraf GeorgeNo ratings yet

- Particulars: Rs. RsDocument7 pagesParticulars: Rs. RsAnmol ChawlaNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- R28 Financial Analysis Techniques IFT Notes PDFDocument23 pagesR28 Financial Analysis Techniques IFT Notes PDFNoor Salman83% (6)

- Nishi Sir's Accounts-NotesDocument34 pagesNishi Sir's Accounts-Notesapi-375803189% (9)

- FORM TP 2017101 Test Code 01239010 MAY/JUNE 2017: Paper 01 - General ProficiencyDocument14 pagesFORM TP 2017101 Test Code 01239010 MAY/JUNE 2017: Paper 01 - General ProficiencyChelsea BynoeNo ratings yet

- BA 2802 - Principles of Finance Solutions To Problems For Recitation #1Document8 pagesBA 2802 - Principles of Finance Solutions To Problems For Recitation #1Eda Nur EvginNo ratings yet

- GST Configuration in SAP FICODocument5 pagesGST Configuration in SAP FICOKingpinNo ratings yet

- Contoh Soal Laporan Arus KasDocument2 pagesContoh Soal Laporan Arus KasRidwanNo ratings yet

- Abebe Kumela Internal AuditDocument19 pagesAbebe Kumela Internal Auditabebe kumelaNo ratings yet

- Deloitte-A Roadmap To Accounting For Income Taxes (Nov2011)Document505 pagesDeloitte-A Roadmap To Accounting For Income Taxes (Nov2011)mistercobalt3511No ratings yet

- Liquidity Ratios - ShyamDocument10 pagesLiquidity Ratios - ShyamYaswanth MaripiNo ratings yet

- CH 3.3 Errors - SDocument10 pagesCH 3.3 Errors - Sসাঈদ আহমদ0% (1)

- Accounting For Provisions and Contingent LiabilitiesDocument8 pagesAccounting For Provisions and Contingent LiabilitiesHenry Lister100% (1)

- Unit 7 Audit of Property Plant and Equipment Handout Final t21516Document10 pagesUnit 7 Audit of Property Plant and Equipment Handout Final t21516Mikaella BengcoNo ratings yet

- CH 04Document25 pagesCH 04Beast aNo ratings yet

- Mas Chap 13Document23 pagesMas Chap 13Raz MahariNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)