You might also like

- Black BookDocument77 pagesBlack BookKanya Nagure100% (2)

- Union Budget of IndiaDocument4 pagesUnion Budget of IndiaPratik .BNo ratings yet

- Session 6 - PPTDocument35 pagesSession 6 - PPTsamal.arabinda25No ratings yet

- CHAPTER 6 Public FinanceDocument19 pagesCHAPTER 6 Public FinanceSonam JainNo ratings yet

- Government Budgeting Indian Budget For BeginnersDocument4 pagesGovernment Budgeting Indian Budget For BeginnersBankatesh ChoudharyNo ratings yet

- The Key Elements of Union Budget Document and Its Formation ProcessesDocument9 pagesThe Key Elements of Union Budget Document and Its Formation Processesposhita8singlaNo ratings yet

- Union Budget 2010Document30 pagesUnion Budget 2010Ashwin SusarlaNo ratings yet

- 3 Fiscal Policy Reddy SirDocument37 pages3 Fiscal Policy Reddy SirTanay BansalNo ratings yet

- Union Budget 2010-11Document23 pagesUnion Budget 2010-11soumyoooNo ratings yet

- 2012-13 Budget Presentation As of 1-4-12 JugunuDocument24 pages2012-13 Budget Presentation As of 1-4-12 JugunuAhsan DileepNo ratings yet

- Fiscal FederalismDocument3 pagesFiscal Federalismanushkajaiswal2002No ratings yet

- Budget 2014Document71 pagesBudget 2014Aswin KumarNo ratings yet

- Fiscal Defecit and Its Trends in India: IntroductionDocument7 pagesFiscal Defecit and Its Trends in India: IntroductionAyushi PatelNo ratings yet

- Economics Project - Government Budget: Meaning of Govt BudgetDocument5 pagesEconomics Project - Government Budget: Meaning of Govt BudgetsanthoshNo ratings yet

- Crux of Union Budget 2023-24 (Upscmaterial)Document21 pagesCrux of Union Budget 2023-24 (Upscmaterial)Sharath VaddiparthiNo ratings yet

- The Budget Making ProcessDocument4 pagesThe Budget Making Processdevilananya2828No ratings yet

- VisionIAS Union Budget February 2024 Summary of Union Interim Budget 2024-25Document13 pagesVisionIAS Union Budget February 2024 Summary of Union Interim Budget 2024-25me15b042No ratings yet

- Manmohan Singh: The Man Who Saved The Indian Economy in 1991Document22 pagesManmohan Singh: The Man Who Saved The Indian Economy in 1991Anonymous wqqSt0No ratings yet

- Banking AwarenessDocument32 pagesBanking AwarenessArnab panditNo ratings yet

- Du MaterialDocument7 pagesDu Materialanimesh singhNo ratings yet

- 1 RM - Budget - RevDocument20 pages1 RM - Budget - RevTwitter OnlyNo ratings yet

- Union Budget & Highlights of Union Budget 2019-20: Educare 247Document9 pagesUnion Budget & Highlights of Union Budget 2019-20: Educare 247Dushyant MudgalNo ratings yet

- Union Budget & Highlights of Union Budget 2019-20: Educare 247Document9 pagesUnion Budget & Highlights of Union Budget 2019-20: Educare 247abhianand123No ratings yet

- Government Budget Need, Types and Impact of BudgetDocument39 pagesGovernment Budget Need, Types and Impact of BudgetBhanu UpadhyayNo ratings yet

- Decoding Indias Union BudgetDocument9 pagesDecoding Indias Union BudgetVanshika GaurNo ratings yet

- The Two Sides of The BudgetDocument8 pagesThe Two Sides of The BudgetritusahrawatNo ratings yet

- 04, Feb 2024, Final - CompressedDocument37 pages04, Feb 2024, Final - Compressedqkhppndjn5No ratings yet

- Budget Taxation 14Document20 pagesBudget Taxation 14Biplab TuduNo ratings yet

- Economics (Q) 2Document15 pagesEconomics (Q) 2जलन्धरNo ratings yet

- Budget PPT PresentationDocument6 pagesBudget PPT PresentationSan DeepNo ratings yet

- Budget 2021 and 2022: A Critical Analysis (Summary)Document5 pagesBudget 2021 and 2022: A Critical Analysis (Summary)Ayushman SinghNo ratings yet

- SEC Assignment Final Semester IIIDocument5 pagesSEC Assignment Final Semester IIITushi TalwarNo ratings yet

- Union Budget of IndiaDocument2 pagesUnion Budget of IndiaRukmani GuptaNo ratings yet

- Interim Budget 2024Document13 pagesInterim Budget 2024praneelalgot4No ratings yet

- Pfcce - Aditya MishraDocument19 pagesPfcce - Aditya MishraMRS.NAMRATA KISHNANI BSSSNo ratings yet

- Budget: Union Finance Minister's Speech:-Finance Minister's Speech Gives A Broad OverviewDocument7 pagesBudget: Union Finance Minister's Speech:-Finance Minister's Speech Gives A Broad OverviewAmbalika SmitiNo ratings yet

- Union Budget of India and Its Analysis: Sem Ii Ce-IDocument34 pagesUnion Budget of India and Its Analysis: Sem Ii Ce-IsuryaliNo ratings yet

- Union Budget 2021-22 IBMDocument9 pagesUnion Budget 2021-22 IBMKUMAR SIMHADHRI HU21CSEN0101917No ratings yet

- Budget 2024Document5 pagesBudget 2024radhaupadhyay150No ratings yet

- Government Budget and Its ComponentsDocument36 pagesGovernment Budget and Its ComponentsAditi Mahale84% (32)

- Évé) (Éjééå Béeé ºéæéêfé (Ié (Ééê®Sé É: Key To The Budget DocumentsDocument9 pagesÉvé) (Éjééå Béeé ºéæéêfé (Ié (Ééê®Sé É: Key To The Budget DocumentsDeepak KumarNo ratings yet

- IASbaba's March Monthly Magazine PDFDocument203 pagesIASbaba's March Monthly Magazine PDFsmilealways20No ratings yet

- Budget and Fiscal Policy - EnglishDocument12 pagesBudget and Fiscal Policy - EnglishMegha guptaNo ratings yet

- Charged ExpenditureDocument7 pagesCharged ExpendituremanojhunkNo ratings yet

- Business and GovernmentDocument81 pagesBusiness and Governmentbiswarup deyNo ratings yet

- Macro Economics ProjectDocument7 pagesMacro Economics ProjectAyushi PatelNo ratings yet

- Budgetary Process 2014 EnglishDocument8 pagesBudgetary Process 2014 EnglishAmber GuptaNo ratings yet

- Union Budget 2023 2024 22f6a9beDocument9 pagesUnion Budget 2023 2024 22f6a9benariesh997No ratings yet

- Vision IAS Union Budget 2024Document13 pagesVision IAS Union Budget 2024GEETA DANDOTINo ratings yet

- Unit - 5Document22 pagesUnit - 5Arun ANNo ratings yet

- 40ekl 15099 BSG Dr. Peter MangiDocument16 pages40ekl 15099 BSG Dr. Peter MangiAllan JoelNo ratings yet

- Government Budget Is An Annual StatementDocument10 pagesGovernment Budget Is An Annual StatementYashika AsraniNo ratings yet

- BUDGET 2020 2021 EnglishDocument193 pagesBUDGET 2020 2021 EnglishAbhishek RajNo ratings yet

- Money, How Money Work, Indian Government Budget, How Indian Government Gain Money FromDocument2 pagesMoney, How Money Work, Indian Government Budget, How Indian Government Gain Money FromAnkit RanjanNo ratings yet

- Analysis of Interim Budget 2019-20 - An Economic PerspectiveDocument5 pagesAnalysis of Interim Budget 2019-20 - An Economic Perspectiveniranjan krishnaNo ratings yet

- Budget Making ProcessDocument8 pagesBudget Making ProcessHarsh AgarwalNo ratings yet

- Government Budget and Its ComponentsDocument38 pagesGovernment Budget and Its ComponentsAditi Mahale50% (4)

- UntitledDocument11 pagesUntitledRohan JaiswalNo ratings yet

- Govt BDocument12 pagesGovt BYasshita GuptaaNo ratings yet

- Dynamic Data Protection: DR M Rajasekhara BabuDocument27 pagesDynamic Data Protection: DR M Rajasekhara BabuRenuSharmaNo ratings yet

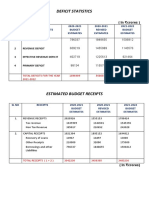

- Deficit StatisticsDocument2 pagesDeficit StatisticsRenuSharmaNo ratings yet

- WINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 28-Apr-2021 KohonenSOMDocument41 pagesWINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 28-Apr-2021 KohonenSOMRenuSharmaNo ratings yet

- WINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material II 19-May-2021 Random ForestDocument22 pagesWINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material II 19-May-2021 Random ForestRenuSharmaNo ratings yet

- WINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 17-May-2021 Ensemble Classifier IntroDocument28 pagesWINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 17-May-2021 Ensemble Classifier IntroRenuSharmaNo ratings yet

- WINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 19-May-2021 BoostingDocument30 pagesWINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 19-May-2021 BoostingRenuSharmaNo ratings yet

- WINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 12-May-2021 5.5 Expectation MaximizationDocument28 pagesWINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 12-May-2021 5.5 Expectation MaximizationRenuSharmaNo ratings yet

- Steps Involved in The PCA: Step 6: Transform The Original MatrixDocument4 pagesSteps Involved in The PCA: Step 6: Transform The Original MatrixRenuSharmaNo ratings yet

- WINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 26-Apr-2021 ClusteringDocument43 pagesWINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 26-Apr-2021 ClusteringRenuSharmaNo ratings yet

- WINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 02-Jun-2021 Principal Component AnalysisDocument28 pagesWINSEM2020-21 CSE4020 ETH VL2020210504996 Reference Material I 02-Jun-2021 Principal Component AnalysisRenuSharmaNo ratings yet

- Multivariate AnalysisDocument57 pagesMultivariate Analysisshishirk12No ratings yet

- Accounting ReviewDocument14 pagesAccounting ReviewMelessa Pescador100% (1)

- Virgen, Era Jane F. BSA 101 Exercise 4 (FBT)Document3 pagesVirgen, Era Jane F. BSA 101 Exercise 4 (FBT)Era Jane VirgenNo ratings yet

- Which of The Followin Level IVDocument2 pagesWhich of The Followin Level IVGuddataa Dheekkamaa100% (2)

- Presentation and Preparation of FS FINALDocument86 pagesPresentation and Preparation of FS FINALJoen SinamagNo ratings yet

- Annex B-1 Guide, Instructions and Blank Copy: (Several Income Payors)Document4 pagesAnnex B-1 Guide, Instructions and Blank Copy: (Several Income Payors)Kristel Anne LiwagNo ratings yet

- Tax Saving InstrumentsDocument4 pagesTax Saving InstrumentsDinesh CNo ratings yet

- Salaryslip Nov. 2022Document1 pageSalaryslip Nov. 2022Raj DelhiNo ratings yet

- Chapter Two NotesDocument18 pagesChapter Two NotesTakudzwa GwemeNo ratings yet

- Financial Planning Tools and Concepts pt.1: Learning ModuleDocument33 pagesFinancial Planning Tools and Concepts pt.1: Learning Moduledaphne ramosNo ratings yet

- CH 3 Accounting For Merchandisng BusinessDocument73 pagesCH 3 Accounting For Merchandisng BusinessYohanna SisayNo ratings yet

- Cashflow Analsis: Tony Deepa PankajDocument20 pagesCashflow Analsis: Tony Deepa PankajDeepaNo ratings yet

- Cash Flow Statement PDFDocument18 pagesCash Flow Statement PDFPrithikaNo ratings yet

- Question 67 (5 Minutes) (Chapter 14)Document59 pagesQuestion 67 (5 Minutes) (Chapter 14)Vu Khanh LeNo ratings yet

- Sample 4Document7 pagesSample 4Snehashis SahaNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

- Quizzer For QE 3BSA Management ServicesDocument15 pagesQuizzer For QE 3BSA Management ServicesSara ChanNo ratings yet

- EPFLAcforFinance17 5Document67 pagesEPFLAcforFinance17 5ddd huangNo ratings yet

- Partnership Taxation OutlineDocument36 pagesPartnership Taxation OutlineYojanny Reyes De la RosaNo ratings yet

- WEWAXX RRLDocument23 pagesWEWAXX RRLMERCY LEOLIGAONo ratings yet

- Chapter 5. Income Statement, Balance Sheet - AppleDocument2 pagesChapter 5. Income Statement, Balance Sheet - AppleJodie NguyễnNo ratings yet

- Basic Oncepts of Income Tax: - Dr. P. Sree Sudha, Associate Professor, DsnluDocument47 pagesBasic Oncepts of Income Tax: - Dr. P. Sree Sudha, Associate Professor, Dsnluleela naga janaki rajitha attiliNo ratings yet

- Dia Mae A. Generoso - Learning Activity 3Document10 pagesDia Mae A. Generoso - Learning Activity 3Dia Mae Ablao GenerosoNo ratings yet

- Module 9 - Donor - S TaxDocument16 pagesModule 9 - Donor - S TaxJohn Russel PacunNo ratings yet

- Bustax Chap9 Theory and ProblemsDocument4 pagesBustax Chap9 Theory and ProblemsPineda, Paula MarieNo ratings yet

- FM RTP Merge FileDocument311 pagesFM RTP Merge FileAritra BanerjeeNo ratings yet

- Parents FormDocument11 pagesParents Formrico saundersNo ratings yet

- 1 Corporate Income Taxation - IntroductionDocument7 pages1 Corporate Income Taxation - IntroductionIvy ObligadoNo ratings yet

- STUDENT Copy Chapter 1 Review of The Accounting CycleDocument28 pagesSTUDENT Copy Chapter 1 Review of The Accounting CycleKurt Latrell AlcantaraNo ratings yet

- Hospital Industry IIIDocument6 pagesHospital Industry IIIIra Grace De Castro100% (1)

- Ch.5 Cash Flow StatementsDocument18 pagesCh.5 Cash Flow StatementsCA INTERNo ratings yet