You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

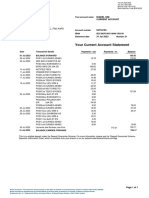

- Statement of Account: Juanima Porter 102 Bonita CT SUMMERVILLE SC 29485-0000Document5 pagesStatement of Account: Juanima Porter 102 Bonita CT SUMMERVILLE SC 29485-0000Kelley73% (15)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Your Business Advantage Checking Bus Platinum Privileges: Account SummaryDocument6 pagesYour Business Advantage Checking Bus Platinum Privileges: Account SummaryN N100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Bank of Ireland 1 PDF 1Document2 pagesBank of Ireland 1 PDF 1ART RAYMOND100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2016 LiBN Who's Who in Women in Professional ServicesDocument36 pages2016 LiBN Who's Who in Women in Professional ServicesMichael DuntzNo ratings yet

- Community - Rural - Bank - of - Guimba - N. - E. - Inc.20180409-1159-V92chb PDFDocument11 pagesCommunity - Rural - Bank - of - Guimba - N. - E. - Inc.20180409-1159-V92chb PDFitsmestephNo ratings yet

- 4.dimatulac v. VillonDocument25 pages4.dimatulac v. VillonitsmestephNo ratings yet

- ADMIN ReviewerDocument57 pagesADMIN RevieweritsmestephNo ratings yet

- People V TuazonDocument3 pagesPeople V TuazonitsmestephNo ratings yet

- Corona - v. - Court - of - AppealsDocument12 pagesCorona - v. - Court - of - AppealsitsmestephNo ratings yet

- (DE GUZMAN v. SANDIGANBAYAN) (Serapio) C2021Document1 page(DE GUZMAN v. SANDIGANBAYAN) (Serapio) C2021itsmestephNo ratings yet

- SNB-4Q-2023-Investor-PresentationDocument49 pagesSNB-4Q-2023-Investor-Presentationpmecahella10No ratings yet

- Harmeet Kaur@pimt InfoDocument7 pagesHarmeet Kaur@pimt InfosanzitNo ratings yet

- Reforms in Banking SectorDocument18 pagesReforms in Banking SectorPrabhjotkaur650% (2)

- Afdb Financial Report 2018 - EnglishDocument172 pagesAfdb Financial Report 2018 - EnglishFoloh RamsesNo ratings yet

- Profits and Gains of Business and ProfessionDocument41 pagesProfits and Gains of Business and ProfessionEsha BafnaNo ratings yet

- ABA 6867 v1C CAMAC Discussion Paper CSRDocument27 pagesABA 6867 v1C CAMAC Discussion Paper CSRsumitmhamunkarNo ratings yet

- Working Capital Managment in Textile IndDocument48 pagesWorking Capital Managment in Textile IndPeter Thomas0% (2)

- Universal BankingDocument10 pagesUniversal BankingRahulTikooNo ratings yet

- X-Social ScienceDocument81 pagesX-Social Scienceshanzathekkoth7No ratings yet

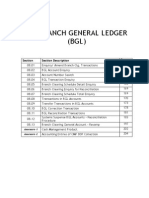

- 01 08-BGLDocument40 pages01 08-BGLmevrick_guy100% (2)

- Chapter 2: AUDIT OF CASH (Receipts and Disbursements) Audit of Cash and Cash Chapter 2 Equivalents Chapter OverviewDocument20 pagesChapter 2: AUDIT OF CASH (Receipts and Disbursements) Audit of Cash and Cash Chapter 2 Equivalents Chapter OverviewAngel RosalesNo ratings yet

- Job Description and Person SpecificationDocument3 pagesJob Description and Person SpecificationFun Toosh345No ratings yet

- Shriram Group PresentationDocument36 pagesShriram Group Presentationchoudharyankush731No ratings yet

- Executive Summary DHFLDocument3 pagesExecutive Summary DHFLSai Dinesh BilleNo ratings yet

- Bank Ownership Reform and Bank Performance in China: Xiaochi Lin, Yi ZhangDocument10 pagesBank Ownership Reform and Bank Performance in China: Xiaochi Lin, Yi ZhangdeaNo ratings yet

- Corporate Governance - Practices and Challenges in AfricaDocument9 pagesCorporate Governance - Practices and Challenges in AfricaLionel Itai MuzondoNo ratings yet

- Credit Transaction QuizDocument5 pagesCredit Transaction QuizMelrick LuceroNo ratings yet

- Lolc Holdings PLC - Annual Report 2020/21Document406 pagesLolc Holdings PLC - Annual Report 2020/21RajithWNNo ratings yet

- Capital Adequacy SolutionsDocument4 pagesCapital Adequacy Solutionsshuvo dasNo ratings yet

- RBI Grade B Exam PatternDocument9 pagesRBI Grade B Exam PatternNikee NeogNo ratings yet

- LLM Part 1-2nd SemDocument26 pagesLLM Part 1-2nd SemUkhad Para State PresidentNo ratings yet

- Bank ReconciliationDocument2 pagesBank Reconciliationapi-3727562No ratings yet

- Auto Debit Arrangement - 20190628 - 174248 PDFDocument3 pagesAuto Debit Arrangement - 20190628 - 174248 PDFellaine mirandaNo ratings yet

- Mairaj Muhib CV (Financial Controller)Document4 pagesMairaj Muhib CV (Financial Controller)muhibmairajNo ratings yet

- Chapter 5 FIMDocument13 pagesChapter 5 FIMMintayto TebekaNo ratings yet

- Trikuta Degree College: Employees'S Job Satisfaction in Ellaquai Dehati BankDocument64 pagesTrikuta Degree College: Employees'S Job Satisfaction in Ellaquai Dehati BankSwyam DuggalNo ratings yet