You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Raisul Sultan Fazal Illahi FLAT-304 Sharjah Main City United Arab EmiratesDocument1 pageRaisul Sultan Fazal Illahi FLAT-304 Sharjah Main City United Arab Emiratesrais sultanNo ratings yet

- Private Sector Development Task Force Final Report and Way ForwardDocument11 pagesPrivate Sector Development Task Force Final Report and Way ForwardSobia AhmedNo ratings yet

- Calculation of Custom ValueDocument22 pagesCalculation of Custom ValueTanzila SiddiquiNo ratings yet

- A. P. (DIR. Series) Circular No. 12, Dated July 31, 2012Document3 pagesA. P. (DIR. Series) Circular No. 12, Dated July 31, 2012Anurag ShuklaNo ratings yet

- Indian Economy 2nd SemDocument4 pagesIndian Economy 2nd SemPooja SanwalNo ratings yet

- BCRP Summer Course - International Macroeconomics: Philippe Bacchetta (University of Lausanne) January 23-27 2012Document2 pagesBCRP Summer Course - International Macroeconomics: Philippe Bacchetta (University of Lausanne) January 23-27 2012Eduardo Sanchez RoselloNo ratings yet

- Indian Real Estate ReportDocument1 pageIndian Real Estate Reportved2549101No ratings yet

- Pension Pay Drawn 06 03 2022 14 01Document2 pagesPension Pay Drawn 06 03 2022 14 01pavithrNo ratings yet

- Two Wheeler MarketDocument14 pagesTwo Wheeler MarketNikitha SreekanthaNo ratings yet

- MBAC 2021 - MBAC505-MBAC2021 - 2021 - 4 - Approved - PaperDocument2 pagesMBAC 2021 - MBAC505-MBAC2021 - 2021 - 4 - Approved - PaperdilupaNo ratings yet

- Consultation Workshop With Stakeholders in The Agriculture and Fishery Sector in Bohol Province Agency: LGU DimiaoDocument4 pagesConsultation Workshop With Stakeholders in The Agriculture and Fishery Sector in Bohol Province Agency: LGU DimiaoTarzan BoyNo ratings yet

- MncsDocument7 pagesMncssonal jainNo ratings yet

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruAmit SharmaNo ratings yet

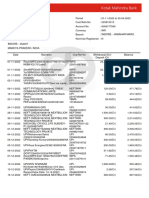

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument62 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSarath KumarNo ratings yet

- Agriculture of PKDocument8 pagesAgriculture of PKUniversity of Punjab LahoreNo ratings yet

- Banking MCQ AwarnessDocument7 pagesBanking MCQ AwarnessJYOTIRMOY GHOSHNo ratings yet

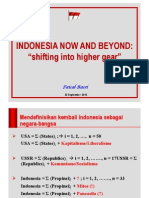

- Faisal Basri - Indonesia Now and Beyond PDFDocument20 pagesFaisal Basri - Indonesia Now and Beyond PDFAmalia AyuningtyasNo ratings yet

- Fake Bank StamentDocument7 pagesFake Bank StamentGovind DhiwarNo ratings yet

- How To Do Your Best-EssayDocument11 pagesHow To Do Your Best-EssayMandar SuryawanshiNo ratings yet

- Presston Engineering Corporation: System Generated Payslip, No Seal and Signature RequiredDocument1 pagePresston Engineering Corporation: System Generated Payslip, No Seal and Signature RequiredRohith GsNo ratings yet

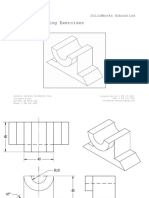

- Detailed Drawing Exercises: Solidworks EducationDocument51 pagesDetailed Drawing Exercises: Solidworks EducationtotoNo ratings yet

- Regional Economic IntegrationDocument50 pagesRegional Economic IntegrationIskandar Zulkarnain KamalluddinNo ratings yet

- Effect of Monetary Policy On Foreign Trade in IndiaDocument8 pagesEffect of Monetary Policy On Foreign Trade in Indiarohan mohapatraNo ratings yet

- Percukaian (Taxation) 2022Document15 pagesPercukaian (Taxation) 2022Faiz IskandarNo ratings yet

- 20220606125603-Banking Sector - Q1-22 enDocument9 pages20220606125603-Banking Sector - Q1-22 enHadeel NoorNo ratings yet

- SidbiDocument3 pagesSidbiPaavni SharmaNo ratings yet

- Topic: Shinhan: Financial GroupDocument13 pagesTopic: Shinhan: Financial GroupSabitkhattakNo ratings yet

- E Passbook 2022 11 02 14 02 45 PMDocument3 pagesE Passbook 2022 11 02 14 02 45 PMSambath KumarNo ratings yet

- Bretton Wood CaseDocument11 pagesBretton Wood CaseMaham WasimNo ratings yet

- TRAIN Tax Law: Primer, Guide & BIR Sample ComputationsDocument4 pagesTRAIN Tax Law: Primer, Guide & BIR Sample ComputationsSymuelly Oliva PoyosNo ratings yet