You might also like

- Submitted in Partial Fulfillment For The Award of Degree Of: Submitted By:-Submitted ToDocument36 pagesSubmitted in Partial Fulfillment For The Award of Degree Of: Submitted By:-Submitted ToMegha AgarawalNo ratings yet

- T Reliance Life InsuranceDocument54 pagesT Reliance Life Insurancenikhil kumarNo ratings yet

- List of Contents:: S No. Chapters Page NoDocument54 pagesList of Contents:: S No. Chapters Page NoChirag JainNo ratings yet

- 1 of Insurance in IndiaDocument30 pages1 of Insurance in Indiaanunaykumar7847No ratings yet

- 09 Chapter 1Document25 pages09 Chapter 1NishobithaNo ratings yet

- Indian Insurance Industry AnalysisDocument90 pagesIndian Insurance Industry Analysismansidube138680% (10)

- Project Topic IRDA and Insurance Administration in IndiaDocument18 pagesProject Topic IRDA and Insurance Administration in IndiaSneha SharmaNo ratings yet

- Objectives:CDocument8 pagesObjectives:CKeerthi AachuNo ratings yet

- Contain: Comparative Study Ofs Customer Preference For Life Insurance Scheme of LIC & Birla Sun LifeDocument143 pagesContain: Comparative Study Ofs Customer Preference For Life Insurance Scheme of LIC & Birla Sun LifeGogol GhoshNo ratings yet

- Index: Executive Summary I Chapter-1 1Document29 pagesIndex: Executive Summary I Chapter-1 1VaibhavRanjankarNo ratings yet

- Index: Student Declaration I Certificate From Guide II Acknowledgement III Executive Summary IVDocument37 pagesIndex: Student Declaration I Certificate From Guide II Acknowledgement III Executive Summary IVJaime ButlerNo ratings yet

- The Insurance Industry in IndiaDocument86 pagesThe Insurance Industry in IndiadfinemeNo ratings yet

- Tata AiaDocument132 pagesTata AiaHimanshu Jadon100% (1)

- Final PagesDocument88 pagesFinal Pagesamitmalik1989No ratings yet

- In Company Training ReportDocument75 pagesIn Company Training ReportVankishKhoslaNo ratings yet

- Insurance in India - WikipediaDocument4 pagesInsurance in India - WikipediaRakesh HaldarNo ratings yet

- Insurance As A Investment Tool at Icici Bank Project Report Mba FinanceDocument73 pagesInsurance As A Investment Tool at Icici Bank Project Report Mba FinanceBabasab Patil (Karrisatte)No ratings yet

- V V V VDocument8 pagesV V V VSahil PurswaniNo ratings yet

- Insurance in India: HistoryDocument6 pagesInsurance in India: HistoryRahul MandalNo ratings yet

- Comparison Between Pension Plans of Lic and IciciDocument103 pagesComparison Between Pension Plans of Lic and IciciNaMan SeThiNo ratings yet

- Comparative Analysis of HDFC SLIC With Other Insurance CompanyDocument76 pagesComparative Analysis of HDFC SLIC With Other Insurance Companysshane kumarNo ratings yet

- Insurance Sector in IndiaDocument5 pagesInsurance Sector in Indiamukesh_khana962No ratings yet

- WipDocument38 pagesWipsujata_patil11214405No ratings yet

- Bachelor of Commerce (Hons.) : Trinity Institute of Professional StudiesDocument39 pagesBachelor of Commerce (Hons.) : Trinity Institute of Professional Studiesanon_941457122No ratings yet

- FA SonalDocument15 pagesFA SonalPrakash BhanushaliNo ratings yet

- Brief History of Insurance SectorDocument14 pagesBrief History of Insurance SectorhundjNo ratings yet

- Role of Actuary in Insurance PDFDocument90 pagesRole of Actuary in Insurance PDFArmanNo ratings yet

- Role of LIC in Indian InsuranceDocument61 pagesRole of LIC in Indian Insurancenikita950100% (2)

- 2.1. HISTORY OF Insurance in India: Chapter Ii: Profile of The CompanyDocument14 pages2.1. HISTORY OF Insurance in India: Chapter Ii: Profile of The Companyjaideep SandisNo ratings yet

- History of Insurance in IndiaDocument33 pagesHistory of Insurance in IndiaRitika BhasinNo ratings yet

- 1.1 Executive SummaryDocument4 pages1.1 Executive SummaryDeepali MestryNo ratings yet

- Devika A V InsuranceDocument19 pagesDevika A V InsuranceSasi KumarNo ratings yet

- Chapter 2Document8 pagesChapter 2sguldekar123No ratings yet

- Chapter 1Document57 pagesChapter 1Rita PalNo ratings yet

- Awareness of Insurance in India - 83921053Document49 pagesAwareness of Insurance in India - 83921053santosh shettyNo ratings yet

- Comparative Analysis of Life Insurance Products Report FinalDocument55 pagesComparative Analysis of Life Insurance Products Report Finalprabux55314No ratings yet

- Insurance in IndiaDocument3 pagesInsurance in IndiapattikankamrajeshwarNo ratings yet

- Recruitment and Selection at Reliance LICDocument66 pagesRecruitment and Selection at Reliance LICRohit KashyapNo ratings yet

- Manusmrithi), Yagnavalkya (Dharmasastra) and Kautilya (Arthasastra) - The Writings Talk inDocument4 pagesManusmrithi), Yagnavalkya (Dharmasastra) and Kautilya (Arthasastra) - The Writings Talk inPawan MishraNo ratings yet

- Evolution of Insurance - IRDAIDocument3 pagesEvolution of Insurance - IRDAIAshish SinghNo ratings yet

- Insurance Industry Analysis ReportDocument58 pagesInsurance Industry Analysis ReportE.GOPINADH92% (13)

- Reforms and Regulations in Insurance Sector in India: Chapter - 5Document15 pagesReforms and Regulations in Insurance Sector in India: Chapter - 5Khushi LakhaniNo ratings yet

- SbiDocument55 pagesSbiJaiHanumankiNo ratings yet

- Project 1doc.Document60 pagesProject 1doc.Shubhanker MeruNo ratings yet

- Insurance in IndiaDocument4 pagesInsurance in IndiaHussainAttarwalaNo ratings yet

- SBI Life InsuranceDocument73 pagesSBI Life Insuranceiloveyoujaan50% (6)

- Insurance Sector in IndiaDocument17 pagesInsurance Sector in IndiaAjaySainNo ratings yet

- SBI Life Insurance Ulips Plan ADocument76 pagesSBI Life Insurance Ulips Plan AMohit kolliNo ratings yet

- Business Success in India: A Complete Guide to Build a Successful Business Knot with Indian FirmsFrom EverandBusiness Success in India: A Complete Guide to Build a Successful Business Knot with Indian FirmsNo ratings yet

- A Guide to Trade Credit InsuranceFrom EverandA Guide to Trade Credit InsuranceNo ratings yet

- Insurance, regulations and loss prevention :Basic Rules for the industry Insurance: Business strategy books, #5From EverandInsurance, regulations and loss prevention :Basic Rules for the industry Insurance: Business strategy books, #5No ratings yet

- W S Service TaxDocument10 pagesW S Service TaxJai GaneshNo ratings yet

- Reference For BlackbookDocument1 pageReference For BlackbookJai GaneshNo ratings yet

- R. K. Palvi Vidyamandir & Junior College: Passed and Promoted To Std. - XIIDocument11 pagesR. K. Palvi Vidyamandir & Junior College: Passed and Promoted To Std. - XIIJai GaneshNo ratings yet

- R. K. Palvi Vidyamandir & Junior College: Passed & Promoted To STD: - XDocument23 pagesR. K. Palvi Vidyamandir & Junior College: Passed & Promoted To STD: - XJai GaneshNo ratings yet

- R. K. Palvi Vidyamandir & Junior College: Passed and Promoted To Std. - XDocument22 pagesR. K. Palvi Vidyamandir & Junior College: Passed and Promoted To Std. - XJai GaneshNo ratings yet

- Wardboy ListDocument2 pagesWardboy ListJai GaneshNo ratings yet

- Eee 1Document3 pagesEee 1Jai GaneshNo ratings yet

- Logo For Black BookDocument5 pagesLogo For Black BookJai GaneshNo ratings yet

- SS Bakers Adivali - 7507606455: Half KGDocument19 pagesSS Bakers Adivali - 7507606455: Half KGJai GaneshNo ratings yet

- Bagrao Raviraj Kashinath: A Project Synopsis FOR Life Insurance Submitted byDocument26 pagesBagrao Raviraj Kashinath: A Project Synopsis FOR Life Insurance Submitted byJai GaneshNo ratings yet

- Hedge Fund Final OutletDocument116 pagesHedge Fund Final OutletJai GaneshNo ratings yet

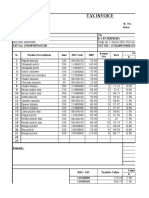

- Tax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyDocument4 pagesTax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyJai GaneshNo ratings yet

- By: Yuvraj Kokare: Resonance IAS Mob.: 7448047047Document24 pagesBy: Yuvraj Kokare: Resonance IAS Mob.: 7448047047Jai GaneshNo ratings yet

- Ajay Shinde: J.S.S.P College, Goveli - TYBMSDocument1 pageAjay Shinde: J.S.S.P College, Goveli - TYBMSJai GaneshNo ratings yet

- Kuldeep1 Initial PagesDocument5 pagesKuldeep1 Initial PagesJai GaneshNo ratings yet

- JAYSHREEDocument1 pageJAYSHREEJai GaneshNo ratings yet

- 3OF2oYPTSypaSRBEBWA7 - ###EBOOK RRB ASM Psychological TestsDocument13 pages3OF2oYPTSypaSRBEBWA7 - ###EBOOK RRB ASM Psychological TestsJai GaneshNo ratings yet

- ICT-4th assessment-GRADE 3Document6 pagesICT-4th assessment-GRADE 3Jai GaneshNo ratings yet

- Resume Personal Information:-NAME:-Miss.: ObjectiveDocument5 pagesResume Personal Information:-NAME:-Miss.: ObjectiveJai GaneshNo ratings yet

- IV Assessment GR 3 QPDocument15 pagesIV Assessment GR 3 QPJai GaneshNo ratings yet

- Scanned by CamscannerDocument6 pagesScanned by CamscannerJai GaneshNo ratings yet

- Government of Transport Department MaharashtraDocument1 pageGovernment of Transport Department MaharashtraJai GaneshNo ratings yet

- Shree Chintamani Developers, Kadakpada (R4)Document4 pagesShree Chintamani Developers, Kadakpada (R4)Jai GaneshNo ratings yet

- Payment Voucher: Sagar Marble GarnitesDocument1 pagePayment Voucher: Sagar Marble GarnitesJai GaneshNo ratings yet

- Government of Transport Department Maharashtra: Reference No:MH05 /0003011/2022 License Type:LLDocument1 pageGovernment of Transport Department Maharashtra: Reference No:MH05 /0003011/2022 License Type:LLJai GaneshNo ratings yet

- Certificate For COVID-19 Vaccination: Beneficiary DetailsDocument1 pageCertificate For COVID-19 Vaccination: Beneficiary DetailsJai GaneshNo ratings yet

- Sakshi 2022Document79 pagesSakshi 2022Jai GaneshNo ratings yet

- Lokseva Test 1 Answer KeyDocument1 pageLokseva Test 1 Answer KeyJai GaneshNo ratings yet

- KKK New Scholarship From 2022Document7 pagesKKK New Scholarship From 2022Jai GaneshNo ratings yet

- Digital InvoiceDocument1 pageDigital InvoiceJai GaneshNo ratings yet

- Chapter 12 Segment Reporting and Decentralization: True/False QuestionsDocument62 pagesChapter 12 Segment Reporting and Decentralization: True/False QuestionsAndrei Anne Palomar0% (1)

- THOUFIQ Resume MbaDocument3 pagesTHOUFIQ Resume MbanaveenNo ratings yet

- Ia04E01 - International Accounting - Elective Course Semester IV Credit - 3 - 1Document11 pagesIa04E01 - International Accounting - Elective Course Semester IV Credit - 3 - 1mohanraokp2279No ratings yet

- Taxguru - In-Schedule II of Companies Act 2013 Depreciation and Practical ImplicationDocument5 pagesTaxguru - In-Schedule II of Companies Act 2013 Depreciation and Practical ImplicationRavi SharmaNo ratings yet

- Audit ReportsDocument31 pagesAudit ReportsAid BolanioNo ratings yet

- Microfridge 1for DTNDocument2 pagesMicrofridge 1for DTNNimmi PandeyNo ratings yet

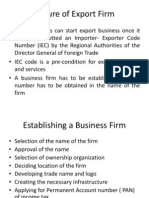

- Formalities of Registration and Export DocumentationDocument10 pagesFormalities of Registration and Export DocumentationAyush GargNo ratings yet

- Cost Management 2nd Edition Eldenburg Test BankDocument40 pagesCost Management 2nd Edition Eldenburg Test Bankaperez1105No ratings yet

- ISB Hyderabad 2011Document15 pagesISB Hyderabad 2011Shantanu ShekharNo ratings yet

- The Rise and Rise of The B2B Brand: Rick Wise and Jana ZednickovaDocument10 pagesThe Rise and Rise of The B2B Brand: Rick Wise and Jana Zednickovasobti_mailmeNo ratings yet

- Bill of Material (BOM)Document2 pagesBill of Material (BOM)Patel BhavinikumariNo ratings yet

- REO - Auditing 1st Preboard May 2022Document15 pagesREO - Auditing 1st Preboard May 2022Marielle GonzalvoNo ratings yet

- Chap 003Document43 pagesChap 003sarakhan0622No ratings yet

- Global Marketing and R&DDocument43 pagesGlobal Marketing and R&Djosiah9_5100% (1)

- IRAC Question Assessment Task 2 - Sem 1 2022Document1 pageIRAC Question Assessment Task 2 - Sem 1 2022Lương Nguyễn Khánh Bảo100% (1)

- Performance Health CheckDocument2 pagesPerformance Health CheckRavi Theja SolletiNo ratings yet

- Techno Mid1Document16 pagesTechno Mid1Graceann GocalinNo ratings yet

- Acceptable and Unacceptable AssetDocument3 pagesAcceptable and Unacceptable AssetDenicelle BucoyNo ratings yet

- Soneri Bank Internship ReportDocument24 pagesSoneri Bank Internship ReportOvaIs MoInNo ratings yet

- Overview of GSTDocument74 pagesOverview of GSTsunil patelNo ratings yet

- Innovation: Innovated by Professor Vijay Govindarajan, Tuck School of Business, Dartmouth CollegeDocument13 pagesInnovation: Innovated by Professor Vijay Govindarajan, Tuck School of Business, Dartmouth CollegeManikandan SuriyanarayananNo ratings yet

- QUESTION BANK For Banking and Insurance MBA Sem IV-FinanceDocument2 pagesQUESTION BANK For Banking and Insurance MBA Sem IV-FinanceAgnya PatelNo ratings yet

- Professional Development Portfolio GuidanceDocument10 pagesProfessional Development Portfolio GuidancehoheinheimNo ratings yet

- Algorithmic Trading Directory 2010Document100 pagesAlgorithmic Trading Directory 201017524100% (4)

- Exposure Management 2.0 - SAP BlogsDocument8 pagesExposure Management 2.0 - SAP Blogsapostolos thomasNo ratings yet

- Finance WikiDocument101 pagesFinance WikiJenő TompiNo ratings yet

- 2nd Phase TestDocument6 pages2nd Phase TestFaiza OmarNo ratings yet

- Business Finance Module 1Document7 pagesBusiness Finance Module 1Kanton FernandezNo ratings yet

- Suggested Solution To Week 5 Tutorial Questions 3.1Document3 pagesSuggested Solution To Week 5 Tutorial Questions 3.1A RNo ratings yet