You might also like

- ADB International Investment Agreement Tool Kit: A Comparative AnalysisFrom EverandADB International Investment Agreement Tool Kit: A Comparative AnalysisNo ratings yet

- 02 - Audit of Property, Plant and EquipmentDocument8 pages02 - Audit of Property, Plant and EquipmentAlarich CatayocNo ratings yet

- SPOILER LAW ON NEGOTIABLE INSTRUMENTS Prelims NCBADocument10 pagesSPOILER LAW ON NEGOTIABLE INSTRUMENTS Prelims NCBAJerome CatalinoNo ratings yet

- Answer/Solution Case: The BRICs: Vanguard of The RevolutionDocument3 pagesAnswer/Solution Case: The BRICs: Vanguard of The RevolutionEvan Octviamen67% (6)

- Saddul v. Losloso DIGESTDocument1 pageSaddul v. Losloso DIGESTLayaNo ratings yet

- Debt Swaps For Development: Creative Solution or Smoke Screen? EURODAD Report Marta Ruiz October 2007Document31 pagesDebt Swaps For Development: Creative Solution or Smoke Screen? EURODAD Report Marta Ruiz October 2007Anna Maria Franzo'100% (1)

- Shareholder Loan AgreementDocument3 pagesShareholder Loan AgreementMatt Warren82% (11)

- Ast Ans KeyDocument189 pagesAst Ans KeySofia SerranoNo ratings yet

- Perspective On TNCDocument11 pagesPerspective On TNCWei TangNo ratings yet

- Ricardian Equivalnce: What Does It Mean?Document4 pagesRicardian Equivalnce: What Does It Mean?sakshi sharmaNo ratings yet

- Ricardian Equivalence: What Does It Mean?Document3 pagesRicardian Equivalence: What Does It Mean?sakshi sharmaNo ratings yet

- IMF StatisticalDeftPublicSectorDebtDocument21 pagesIMF StatisticalDeftPublicSectorDebtligia.ourivesNo ratings yet

- Policy Research Paper World BankDocument8 pagesPolicy Research Paper World Bankczozyxakf100% (1)

- This Content Downloaded From 62.22.68.43 On Thu, 17 Feb 2022 10:11:15 UTCDocument43 pagesThis Content Downloaded From 62.22.68.43 On Thu, 17 Feb 2022 10:11:15 UTCnicodelrioNo ratings yet

- Blackburn 2012Document11 pagesBlackburn 2012suminiNo ratings yet

- Coffee Industries of IndiaDocument24 pagesCoffee Industries of IndiaDebarshiDuttaNo ratings yet

- External Debt Burden and Its Determinants in NigeriaDocument7 pagesExternal Debt Burden and Its Determinants in NigeriaNhi NguyễnNo ratings yet

- Fiscal Multiplier PDFDocument16 pagesFiscal Multiplier PDFeljosetobarNo ratings yet

- Why Dont We Follow The Rules Drivers of Compliance With Fiscal Policy Rules in Latin America andDocument34 pagesWhy Dont We Follow The Rules Drivers of Compliance With Fiscal Policy Rules in Latin America andgabriel4441No ratings yet

- Determinants of Public DebtDocument28 pagesDeterminants of Public DebtNhi NguyễnNo ratings yet

- Rafi and Augistine Paper (Public Debt)Document8 pagesRafi and Augistine Paper (Public Debt)kartikNo ratings yet

- Mashup Indices of Development World Bank Research Paper No. 5432Document5 pagesMashup Indices of Development World Bank Research Paper No. 5432fyswvx5bNo ratings yet

- Troubling Tradeoffs in The Human Development Index: Policy Research Working Paper 5484Document32 pagesTroubling Tradeoffs in The Human Development Index: Policy Research Working Paper 5484Grace JiangNo ratings yet

- Sovereign Debt in The AmericasDocument41 pagesSovereign Debt in The AmericasmontagesNo ratings yet

- Financial Development, Financial Inclusion, and Informality: New International EvidenceDocument36 pagesFinancial Development, Financial Inclusion, and Informality: New International EvidencececaNo ratings yet

- Dependency 3Document86 pagesDependency 3Timothy SikambaleNo ratings yet

- MPRA - Paper Pakistans Financial DependencyDocument41 pagesMPRA - Paper Pakistans Financial DependencyAnsharah AhmedNo ratings yet

- Econ 157 - Homework II. 11Document6 pagesEcon 157 - Homework II. 11BrimerNo ratings yet

- An Evaluation of The Challenges and Prospects of Micro and Small Scale Enterprises Development in NigeriaDocument39 pagesAn Evaluation of The Challenges and Prospects of Micro and Small Scale Enterprises Development in NigeriaSomtoo UmeadiNo ratings yet

- Journal of International Economics: Dennis Reinhardt, Luca Antonio Ricci, Thierry TresselDocument17 pagesJournal of International Economics: Dennis Reinhardt, Luca Antonio Ricci, Thierry TresselmusaNo ratings yet

- Integrated Financial Management in Least Developed CountriesDocument151 pagesIntegrated Financial Management in Least Developed CountriesAteeq Ur RehmanNo ratings yet

- 1 PBDocument9 pages1 PBhamzaNo ratings yet

- WBWP FiscalDocument67 pagesWBWP FiscalAndrew MayedaNo ratings yet

- Multiple EquilibriaDocument16 pagesMultiple EquilibriaSabahat ZafarNo ratings yet

- ED PPT Chapter 1Document22 pagesED PPT Chapter 1FuadNo ratings yet

- Public Debt Management: Munich Personal Repec ArchiveDocument33 pagesPublic Debt Management: Munich Personal Repec Archivenssd2kNo ratings yet

- PPEA2020005Document27 pagesPPEA2020005Muknerd DhakaNo ratings yet

- Unfin 1Document35 pagesUnfin 1Patatri SarkarNo ratings yet

- MPRA Paper 88440Document15 pagesMPRA Paper 88440rifat sauqyNo ratings yet

- International Business: Prof: Viju NavareDocument17 pagesInternational Business: Prof: Viju NavareNimisha BurdeNo ratings yet

- 3 Lec 1 of Chapter 2Document25 pages3 Lec 1 of Chapter 2OKUBO SELESTINE OPIYONo ratings yet

- Cecchetti, Mohanty and Zampolli 2011Document39 pagesCecchetti, Mohanty and Zampolli 2011DanielaNo ratings yet

- GDP Linked Sukuk - RevisedDocument16 pagesGDP Linked Sukuk - RevisedrizaunNo ratings yet

- Private Sector Consumption and Government Consumption and Debt in Advanced Economies: An Empirical StudyDocument28 pagesPrivate Sector Consumption and Government Consumption and Debt in Advanced Economies: An Empirical StudyArsalan TahirNo ratings yet

- Literature Review On Public DebtDocument8 pagesLiterature Review On Public Debtpxihigrif100% (1)

- D F A H ?: Simeon Djankov, Jose G. Montalvo, and Marta Reynal-QuerolDocument28 pagesD F A H ?: Simeon Djankov, Jose G. Montalvo, and Marta Reynal-QuerolKorkemNo ratings yet

- Artikel Internasional 1Document18 pagesArtikel Internasional 1Josse andreNo ratings yet

- lED PPT Chapter 4Document33 pageslED PPT Chapter 4FuadNo ratings yet

- Who Gets The Credit? and Does It Matter?: P R W P 4661Document41 pagesWho Gets The Credit? and Does It Matter?: P R W P 4661Prashant KothariNo ratings yet

- Thesis Global Multi Asset FundDocument8 pagesThesis Global Multi Asset FundKarla Adamson100% (2)

- LKJH4A33C7AFFDocument12 pagesLKJH4A33C7AFFRao TvaraNo ratings yet

- Chapter 1 - Financial Reporting and Accounting Standards - Intermediate Accounting - IFRS Edition, 2nd EditionDocument41 pagesChapter 1 - Financial Reporting and Accounting Standards - Intermediate Accounting - IFRS Edition, 2nd EditionWihl Mathew ZalatarNo ratings yet

- An Empirical Examination of Why Mobile Money Schemes Ignite in SoDocument53 pagesAn Empirical Examination of Why Mobile Money Schemes Ignite in SoWayne GonsalvesNo ratings yet

- When Is Debt Sustainable 2006Document35 pagesWhen Is Debt Sustainable 2006Kerine HeronNo ratings yet

- Are Less Developed Countries More Exposed - lhz002Document20 pagesAre Less Developed Countries More Exposed - lhz002mutia.wNo ratings yet

- Involving The Private Sector and Ppps in Financing Public Investments: Some Opportunities and ChallengesDocument37 pagesInvolving The Private Sector and Ppps in Financing Public Investments: Some Opportunities and Challengestahirawan82No ratings yet

- PPEA2021022Document15 pagesPPEA2021022Ivan LessiaNo ratings yet

- Diplomacy, Trade and Aid: Searching For "Synergies": C.D. HoweDocument32 pagesDiplomacy, Trade and Aid: Searching For "Synergies": C.D. Howeapi-241513002No ratings yet

- And Public Policy. Rodrik Praises The Report As A Turning Point in The Discourse of DevelopmentDocument3 pagesAnd Public Policy. Rodrik Praises The Report As A Turning Point in The Discourse of DevelopmentSandeep HanumanNo ratings yet

- Prices or Knowledge? What Drives Demand For Financial Services in Emerging Markets?Document35 pagesPrices or Knowledge? What Drives Demand For Financial Services in Emerging Markets?ira putri zulfaNo ratings yet

- 5Document24 pages5Nhi NguyễnNo ratings yet

- Ecta 200623Document36 pagesEcta 200623Malek BlrNo ratings yet

- Fiscal Sustainability: The Impact of Real Exchange Rate Shocks On Debt Valuation, Interest Rates and GDP GrowthDocument22 pagesFiscal Sustainability: The Impact of Real Exchange Rate Shocks On Debt Valuation, Interest Rates and GDP GrowthlarasatiayuNo ratings yet

- BRISKResources Andre Proite Asset Liability Managementin Developing Countries ABalance Sheet ApproachDocument36 pagesBRISKResources Andre Proite Asset Liability Managementin Developing Countries ABalance Sheet ApproachZainab ShahidNo ratings yet

- FM Assignment AnanduDocument23 pagesFM Assignment AnanduAmrutha P RNo ratings yet

- Statement of Realization and LiquidationDocument2 pagesStatement of Realization and LiquidationSherilyn BunagNo ratings yet

- Nature and Scope of Investment ManagementDocument5 pagesNature and Scope of Investment ManagementRavi GuptaNo ratings yet

- Term Paper Final - SanjoyDocument25 pagesTerm Paper Final - SanjoyChoton AminNo ratings yet

- Arjun BS 15-16Document1 pageArjun BS 15-16Girish VijiNo ratings yet

- FAR05-2.2 - Accounts ReceivableDocument4 pagesFAR05-2.2 - Accounts ReceivableJayNo ratings yet

- Adjusting Journal Entry Activity QuizDocument2 pagesAdjusting Journal Entry Activity Quizaceboyyyyyy20No ratings yet

- Economic Sustainability For Islamic Nanofinance Through Waqf - Sukuk Linkage Program: Case Study in IndonesiaDocument23 pagesEconomic Sustainability For Islamic Nanofinance Through Waqf - Sukuk Linkage Program: Case Study in IndonesiaRifaldy MajidNo ratings yet

- Extinguishment of SaleDocument10 pagesExtinguishment of SaleJeanNo ratings yet

- Heirs of Eduardo Manlapat vs. Court of AppealsDocument31 pagesHeirs of Eduardo Manlapat vs. Court of AppealsUfbNo ratings yet

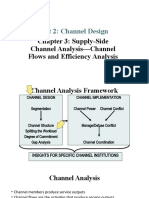

- Chapter 3 Channel FlowsDocument17 pagesChapter 3 Channel FlowsAhmed ButtNo ratings yet

- Cholamandalam Auction Sale Notice Rakeshkumar Gautamchand Dugar 12.04.2021Document5 pagesCholamandalam Auction Sale Notice Rakeshkumar Gautamchand Dugar 12.04.2021Surender SarswatNo ratings yet

- TRM G3 Tut3 BidvDocument28 pagesTRM G3 Tut3 Bidvtrung luuchiNo ratings yet

- Wa0047.Document2 pagesWa0047.daniellparisNo ratings yet

- Ac 114 Pratice Final Exam QuestionsDocument200 pagesAc 114 Pratice Final Exam QuestionsChad Vincent B. BollosaNo ratings yet

- Arnerich V DHC Assets LTD (2021) NZSC 121Document9 pagesArnerich V DHC Assets LTD (2021) NZSC 121PNo ratings yet

- Bes F1Document33 pagesBes F1Pro NdebeleNo ratings yet

- Module 1 4 BUSCOMDocument40 pagesModule 1 4 BUSCOMNoeme LansangNo ratings yet

- With Owners of The Business, Such As Share Issues and Dividends. The Statement Making The LinkDocument7 pagesWith Owners of The Business, Such As Share Issues and Dividends. The Statement Making The LinkHikmət RüstəmovNo ratings yet

- Asset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolDocument26 pagesAsset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolBlake SheltonNo ratings yet

- Team 08 LTD.: ChanakyaDocument2 pagesTeam 08 LTD.: ChanakyaPeyush NeneNo ratings yet

- Fair Practices Code: ObjectiveDocument16 pagesFair Practices Code: ObjectiveBADRI VENKATESHNo ratings yet

- 1 - Ledger Group TallyDocument3 pages1 - Ledger Group TallyAmit Joshi100% (2)

- Chapter-2: The Accounting Cycle: Accounting For A Service Enterprise 2.1Document19 pagesChapter-2: The Accounting Cycle: Accounting For A Service Enterprise 2.1Nigussie BerhanuNo ratings yet

- Midterm Exam - Financial Accounting 3 With AnswersDocument11 pagesMidterm Exam - Financial Accounting 3 With Answersjanus lopezNo ratings yet