You might also like

- Cdpe Advanced 2-2Document7 pagesCdpe Advanced 2-2api-241184916No ratings yet

- How to Win the Property War in Your Bankruptcy: Winning at Law, #4From EverandHow to Win the Property War in Your Bankruptcy: Winning at Law, #4No ratings yet

- 4 Accounting For Legal Liqudation PresentationDocument40 pages4 Accounting For Legal Liqudation PresentationMeselech Girma100% (1)

- Bankruptcy Guide OverviewDocument5 pagesBankruptcy Guide OverviewMisaki AyuzawaNo ratings yet

- MN499 CH6 Problem Loan ManagementDocument21 pagesMN499 CH6 Problem Loan ManagementStudent Sokha ChanchesdaNo ratings yet

- The Essential Guide to Understanding the Short Sale ProcessDocument16 pagesThe Essential Guide to Understanding the Short Sale ProcessnymodificationNo ratings yet

- Collections and Repayments PDFDocument54 pagesCollections and Repayments PDFJimuel FaigaoNo ratings yet

- Source of Finance For BusinessDocument26 pagesSource of Finance For BusinessJooooooooNo ratings yet

- Debt RestructuringDocument16 pagesDebt RestructuringtorreshectorNo ratings yet

- 2.1.2 As External FinanceDocument49 pages2.1.2 As External FinanceEhtesham UmerNo ratings yet

- Module 7 Exit Outcomes and Firm Value BankruptcyDocument6 pagesModule 7 Exit Outcomes and Firm Value BankruptcyTanisha MukherjeeNo ratings yet

- MANAGMENTDocument35 pagesMANAGMENTHammad LiaqatNo ratings yet

- Financial Distress: Group 5 ACT 4611 Seminar in AccountingsDocument38 pagesFinancial Distress: Group 5 ACT 4611 Seminar in AccountingsPj SornNo ratings yet

- Wilson Lumber Case Group 5Document10 pagesWilson Lumber Case Group 5Falah HindNo ratings yet

- MN2615 T5 Session 2- Small Business FinanceDocument59 pagesMN2615 T5 Session 2- Small Business FinanceHaseeb DarNo ratings yet

- Pros and Cons of Equity Shares and DebenturesDocument21 pagesPros and Cons of Equity Shares and Debenturesmithil_tannaNo ratings yet

- Evaluate Creditworthiness TechniquesDocument19 pagesEvaluate Creditworthiness TechniquesAbhijeet JadhavNo ratings yet

- Venture Debt OverviewDocument23 pagesVenture Debt OverviewKent WhiteNo ratings yet

- Ed Sources of FinanceDocument28 pagesEd Sources of FinanceShubham SaraogiNo ratings yet

- MBA 832 Chapter 3Document36 pagesMBA 832 Chapter 3shammahmuzNo ratings yet

- Unit 5: Financial Information and Decisions: 5.1 Business Finance: Needs and SourcesDocument41 pagesUnit 5: Financial Information and Decisions: 5.1 Business Finance: Needs and SourcesSaritha SajeshNo ratings yet

- Entrepreneurship: Succession Planning and Strategies For Harvesting and Ending The VentureDocument24 pagesEntrepreneurship: Succession Planning and Strategies For Harvesting and Ending The VentureAfaq GhaniNo ratings yet

- Chapter 5 - Using CreditDocument48 pagesChapter 5 - Using CreditALEXIA TANG DAI XIANNo ratings yet

- Stop ForeclosureDocument7 pagesStop ForeclosureRicharnellia-RichieRichBattiest-Collins0% (1)

- Functions of the financial systemDocument8 pagesFunctions of the financial systemDRIP HARDLYNo ratings yet

- Short Sale Seminar Bakersfield, CADocument22 pagesShort Sale Seminar Bakersfield, CAMiguel GarciaNo ratings yet

- Company Financing: Other Sources of Finance For A Limited CompanyDocument20 pagesCompany Financing: Other Sources of Finance For A Limited CompanyNokutenda K GumbieNo ratings yet

- R8-M1 Bankruptcy Part 1 ExplainedDocument12 pagesR8-M1 Bankruptcy Part 1 ExplainednishuNo ratings yet

- Innovation As An Entrepreneur and Different Types of Enterprises and CompaniesDocument51 pagesInnovation As An Entrepreneur and Different Types of Enterprises and Companiespaulkhor74No ratings yet

- Ch4 Credit ManagementDocument9 pagesCh4 Credit ManagementWilsonNo ratings yet

- Et ZC414 13Document20 pagesEt ZC414 13rajpd28No ratings yet

- Foreclosure Alternatives ReportDocument3 pagesForeclosure Alternatives ReportCindy GrecoNo ratings yet

- 06 MoneyDocument4 pages06 Moneywhwei91No ratings yet

- Debt Financing or Equity FinancingDocument10 pagesDebt Financing or Equity Financingimran hossain ruman100% (1)

- Chapter 3 - Forms of Small Business OwnershipDocument13 pagesChapter 3 - Forms of Small Business OwnershipKristina ChernitskayaNo ratings yet

- 3.1 Sources of FinanceDocument29 pages3.1 Sources of FinanceDanae Illia GamarraNo ratings yet

- Week 9, Financial Information and Financial DecisionsDocument47 pagesWeek 9, Financial Information and Financial DecisionsGloria Boatemaa KWAKYENo ratings yet

- When Should Revenue Be Recognized 2. How Much Revenue Should BeDocument25 pagesWhen Should Revenue Be Recognized 2. How Much Revenue Should BeKen AdamsNo ratings yet

- Financial DistresDocument8 pagesFinancial Distres27 Md. Rakibul IslamNo ratings yet

- Comprehensive Credit Repair 10-18-07Document64 pagesComprehensive Credit Repair 10-18-07Carol100% (1)

- Week 10 - Lecture 2 - Sources of FinanceDocument39 pagesWeek 10 - Lecture 2 - Sources of Financebeni benoNo ratings yet

- Mortgage Foreclosure in SCDocument3 pagesMortgage Foreclosure in SCSC AppleseedNo ratings yet

- Debt Vs EquityDocument4 pagesDebt Vs EquityNooraghaNo ratings yet

- Equity and Debt: First Some RevisionDocument44 pagesEquity and Debt: First Some RevisionHay JirenyaaNo ratings yet

- Finance PPT 2Document40 pagesFinance PPT 2api-679810879No ratings yet

- Sources of FinanceDocument7 pagesSources of FinanceJay KoliNo ratings yet

- Coursebook Answers: Answers To Test Yourself QuestionsDocument5 pagesCoursebook Answers: Answers To Test Yourself QuestionsDoris Yee50% (2)

- Chapters 4 and 5Document15 pagesChapters 4 and 5Estee FongNo ratings yet

- Self Service Loan Mod 1stDocument13 pagesSelf Service Loan Mod 1stGary SilvermanNo ratings yet

- Business Incorporation UsDocument21 pagesBusiness Incorporation UsMARIANA CRISTINA ANAYA QUINTERONo ratings yet

- Ten Axioms, Principles in FinanceDocument14 pagesTen Axioms, Principles in FinancePierreNo ratings yet

- Bessemer Guide To Venture DebtDocument14 pagesBessemer Guide To Venture Debtarnoldlee1No ratings yet

- C7-Types of Business Ownership-FDocument27 pagesC7-Types of Business Ownership-FMaria Evelyn WonNo ratings yet

- DistressDocument49 pagesDistressОксана Пелипец100% (1)

- Capital Structure Choices Trade-offsDocument39 pagesCapital Structure Choices Trade-offsSatish TayalNo ratings yet

- #5. DIY Credit Repair: Doable, Time-IntensiveDocument5 pages#5. DIY Credit Repair: Doable, Time-IntensiveCarolNo ratings yet

- SmallbusinessDocument14 pagesSmallbusinessDaniel PintoNo ratings yet

- 1 Formsofbusinessorganization 110902153402 Phpapp01Document31 pages1 Formsofbusinessorganization 110902153402 Phpapp01Von QuiozonNo ratings yet

- Journal Entries ExplainedDocument10 pagesJournal Entries ExplainedMuhammad MansoorNo ratings yet

- Smart Factories For Small To Medium Manufacturers How To Get From Here To ThereDocument11 pagesSmart Factories For Small To Medium Manufacturers How To Get From Here To Theresanjay chamoliNo ratings yet

- 8 Rules of Success in New Markets CorrectedDocument1 page8 Rules of Success in New Markets CorrectedBright SamuelNo ratings yet

- Erase Economic Uncertainty For SmallDocument17 pagesErase Economic Uncertainty For SmallBright SamuelNo ratings yet

- Warehousing & DistributionDocument2 pagesWarehousing & DistributionBright SamuelNo ratings yet

- 21 Employee Engagement Activities that WorkDocument5 pages21 Employee Engagement Activities that WorkBright SamuelNo ratings yet

- Apprenticeship Employer Event Unlocking Tomorrow's Talent Tickets, Wed 8 Feb 2023 at 18 00 EventbriteDocument6 pagesApprenticeship Employer Event Unlocking Tomorrow's Talent Tickets, Wed 8 Feb 2023 at 18 00 EventbriteBright SamuelNo ratings yet

- Cost-Effectiveness of JobsDocument43 pagesCost-Effectiveness of JobsBright SamuelNo ratings yet

- Better Food For AllDocument141 pagesBetter Food For AllBright SamuelNo ratings yet

- Swartland Crop Rotation Main Document Final June2015Document32 pagesSwartland Crop Rotation Main Document Final June2015Bright SamuelNo ratings yet

- 6 Steps To Vet The Quality Standards of Third-Party Medical Device ManufacturersDocument3 pages6 Steps To Vet The Quality Standards of Third-Party Medical Device ManufacturersBright SamuelNo ratings yet

- Swartland Crop Rotation Annexure A Final June2015Document28 pagesSwartland Crop Rotation Annexure A Final June2015Bright SamuelNo ratings yet

- 0 BrexitDocument7 pages0 BrexitBright SamuelNo ratings yet

- AD-House Security BookstoreDocument1 pageAD-House Security BookstoreBright SamuelNo ratings yet

- How Do You Lead by ExampleDocument9 pagesHow Do You Lead by ExampleBright SamuelNo ratings yet

- Research Project Summary - Ostrich - 2012 - 2013 - ContentDocument40 pagesResearch Project Summary - Ostrich - 2012 - 2013 - ContentBright SamuelNo ratings yet

- 21 Employee Engagement Activities that WorkDocument5 pages21 Employee Engagement Activities that WorkBright SamuelNo ratings yet

- Research Project Summary Smallstock 2012 2013 ContentDocument44 pagesResearch Project Summary Smallstock 2012 2013 ContentBright SamuelNo ratings yet

- Research Data in The Digital AgeDocument3 pagesResearch Data in The Digital AgeBright SamuelNo ratings yet

- Document The 7 Deadly Sins of ManagersDocument4 pagesDocument The 7 Deadly Sins of ManagersBright SamuelNo ratings yet

- Research Project Summary Smallstock 2012 2013 ContentDocument44 pagesResearch Project Summary Smallstock 2012 2013 ContentBright SamuelNo ratings yet

- Awakening Africa's Sleeping Giant? The Potentials and The PitfallsDocument7 pagesAwakening Africa's Sleeping Giant? The Potentials and The PitfallsBright SamuelNo ratings yet

- Historical/Significant Sites in Azumini, Ndoki: UminiDocument16 pagesHistorical/Significant Sites in Azumini, Ndoki: UminiBright SamuelNo ratings yet

- Citrus: World Markets and Trade: Orange Production Springs Higher in Brazil and Mexico in 2020/21Document13 pagesCitrus: World Markets and Trade: Orange Production Springs Higher in Brazil and Mexico in 2020/21Bright SamuelNo ratings yet

- Document How To Sound Like A LeaderDocument5 pagesDocument How To Sound Like A LeaderBright SamuelNo ratings yet

- 10 Proven Ways To DelegateDocument2 pages10 Proven Ways To DelegateBright SamuelNo ratings yet

- Job DescriptionUPDATEDLMDocument7 pagesJob DescriptionUPDATEDLMrobinrubinaNo ratings yet

- Citrus: World Markets and Trade: Orange Production Springs Higher in Brazil and Mexico in 2020/21Document13 pagesCitrus: World Markets and Trade: Orange Production Springs Higher in Brazil and Mexico in 2020/21Bright SamuelNo ratings yet

- LinuxTrainingAcademy.com Find Command Cheat SheetDocument6 pagesLinuxTrainingAcademy.com Find Command Cheat SheetBright SamuelNo ratings yet

- Most Misused and Abused WordsDocument10 pagesMost Misused and Abused WordsGabor KovacsNo ratings yet

- Memorials of The RespondentDocument25 pagesMemorials of The RespondentBhavesh BhattNo ratings yet

- Fauquier Supervisors May 14, 2020, AgendaDocument3 pagesFauquier Supervisors May 14, 2020, AgendaFauquier NowNo ratings yet

- New Oct Manual PDFDocument352 pagesNew Oct Manual PDFkoss kossNo ratings yet

- RRL For Men and Women in The FamilyDocument12 pagesRRL For Men and Women in The FamilyIvan LuzuriagaNo ratings yet

- Financial Statements and Ratio Analysis: All Rights ReservedDocument55 pagesFinancial Statements and Ratio Analysis: All Rights ReservedZidan ZaifNo ratings yet

- Esys Vs NtanDocument3 pagesEsys Vs Ntantonmoy619No ratings yet

- Business Plan Chapter 1Document33 pagesBusiness Plan Chapter 1Ravi NagarathanamNo ratings yet

- Pki (Sran15.1 02)Document129 pagesPki (Sran15.1 02)VVL1959No ratings yet

- PNB Vs CA (83 SCRA 237)Document1 pagePNB Vs CA (83 SCRA 237)sherrylmelgarNo ratings yet

- People vs. GodinezDocument7 pagesPeople vs. GodinezAustine CamposNo ratings yet

- GARVICH, Javier. El Caracter Chicha en La Cultura Peruana ContemporaneaDocument10 pagesGARVICH, Javier. El Caracter Chicha en La Cultura Peruana ContemporaneaDarloxNo ratings yet

- Patrick Caronan Vs Richard CaronanDocument8 pagesPatrick Caronan Vs Richard CaronanJosh CabreraNo ratings yet

- CIMB Savings StatementDocument2 pagesCIMB Savings StatementNoriza GhazaliNo ratings yet

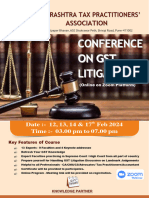

- Conference On GST Litigation-2024Document6 pagesConference On GST Litigation-2024tsdhameliya1No ratings yet

- CF-Chap 02-Analysis of Financial StatementDocument58 pagesCF-Chap 02-Analysis of Financial StatementM7No ratings yet

- WWVP Identity Requirements - Access CanberraDocument2 pagesWWVP Identity Requirements - Access CanberraMaría CalderónNo ratings yet

- Barangay Samara: Office of The Sangguniang Barangay Series of 2018Document1 pageBarangay Samara: Office of The Sangguniang Barangay Series of 2018Maria RinaNo ratings yet

- Maqasid Al SyariahDocument18 pagesMaqasid Al SyariahNaugi AvrilioNo ratings yet

- RW2011-15 Toc 183749110917062932Document6 pagesRW2011-15 Toc 183749110917062932Dwi AgungNo ratings yet

- Janssenville ES Year-End SOSADocument6 pagesJanssenville ES Year-End SOSARomnick ArenasNo ratings yet

- SB 737 53 1125 03Document39 pagesSB 737 53 1125 03Fernando CarmonaNo ratings yet

- Your English Pal ESL Lesson Plan Press Freedom Student v3Document4 pagesYour English Pal ESL Lesson Plan Press Freedom Student v3999 MTHNo ratings yet

- A guide to Malaysian payroll basicsDocument43 pagesA guide to Malaysian payroll basicsmelanieNo ratings yet

- The Color of OrangeDocument3 pagesThe Color of Orangeben_faganNo ratings yet

- T B L J: HE Anking AW OurnalDocument9 pagesT B L J: HE Anking AW OurnalsamrajcseNo ratings yet

- The American Dream in The Great Gatsby, The Bluest Eye and The Book of DanielDocument7 pagesThe American Dream in The Great Gatsby, The Bluest Eye and The Book of DanielJuliana Koch de MendonçaNo ratings yet

- Timeline of Philippine HistoryDocument6 pagesTimeline of Philippine HistoryCarlos Baul DavidNo ratings yet

- 1971 1999 PDFDocument74 pages1971 1999 PDFSheraz UmarNo ratings yet

- Social Movements and Human Rights in IndiaDocument15 pagesSocial Movements and Human Rights in IndiaChirantan KashyapNo ratings yet

- Dulalia vs. CruzDocument6 pagesDulalia vs. CruzAdrianne BenignoNo ratings yet