You might also like

- Financial Markets Integration in India: Asia-Pacific Development Journal Vol. 12, No. 2, December 2005Document18 pagesFinancial Markets Integration in India: Asia-Pacific Development Journal Vol. 12, No. 2, December 2005anon-392261No ratings yet

- The Impact of Capital Market On Economic Growth: A Malaysian OutlookDocument7 pagesThe Impact of Capital Market On Economic Growth: A Malaysian OutlookMuhammad SalehNo ratings yet

- Asian Development Review: Volume 29, Number 2, 2012From EverandAsian Development Review: Volume 29, Number 2, 2012No ratings yet

- Integration of Financial Markets in India: An Empirical AnalysisDocument24 pagesIntegration of Financial Markets in India: An Empirical AnalysisashvinesharmaNo ratings yet

- Indian Stock Market and Investors StrategyFrom EverandIndian Stock Market and Investors StrategyRating: 3.5 out of 5 stars3.5/5 (3)

- Indian Financial System Project 3sem (Priyank)Document35 pagesIndian Financial System Project 3sem (Priyank)priyank chourasiyaNo ratings yet

- Stock Market in A Liberalised Economy - Indian ExperiencesDocument8 pagesStock Market in A Liberalised Economy - Indian ExperiencesAnkit KumarNo ratings yet

- Evolution of Financial Service Sector in IndiaDocument47 pagesEvolution of Financial Service Sector in IndiaGauravSingh0% (1)

- Economic and Political Weekly Economic and Political WeeklyDocument8 pagesEconomic and Political Weekly Economic and Political WeeklyBCNo ratings yet

- Role of Money Market in Context To GrowtDocument13 pagesRole of Money Market in Context To Growtjayaprakash1021No ratings yet

- Equity and Corporate Debt Market: I. Equity Market Role of The Stock Market in Financing Economic GrowthDocument27 pagesEquity and Corporate Debt Market: I. Equity Market Role of The Stock Market in Financing Economic GrowthmrinalthakkarNo ratings yet

- 1.1) Introduction To Indian Financial SystemDocument34 pages1.1) Introduction To Indian Financial SystemrssishereNo ratings yet

- Management of Financial InstitutionDocument172 pagesManagement of Financial InstitutionNeo Nageshwar Das50% (2)

- Rakesh Mohan On Indian Financial MarketsDocument23 pagesRakesh Mohan On Indian Financial MarketsRosie_89No ratings yet

- Sebi Intro PDFDocument111 pagesSebi Intro PDFKashish Pandia100% (1)

- 13 - Chapter 3 PDFDocument5 pages13 - Chapter 3 PDFNowfalNo ratings yet

- Co-Movement and Integration Among Stock Markets: A Study of 10 CountriesDocument16 pagesCo-Movement and Integration Among Stock Markets: A Study of 10 CountriesDr Bhadrappa HaralayyaNo ratings yet

- All Real and FinancialDocument16 pagesAll Real and FinancialOgwoGPNo ratings yet

- Ecomomic DevelopmentDocument19 pagesEcomomic DevelopmentUmair SamNo ratings yet

- Theory of Financial Intermediation. 1.0 History of Financail IntermediariesDocument23 pagesTheory of Financial Intermediation. 1.0 History of Financail IntermediariesAmeh AnyebeNo ratings yet

- Money MarketDocument13 pagesMoney Marketkitten301No ratings yet

- 2WPSN140313Document29 pages2WPSN140313Rakesh BetiwarNo ratings yet

- Financial Sector Reforms and Monetary Policy: The Indian Experience Rakesh Mohan IDocument42 pagesFinancial Sector Reforms and Monetary Policy: The Indian Experience Rakesh Mohan IRam KumarNo ratings yet

- 08 Chapter 2Document45 pages08 Chapter 2Sujit KumarNo ratings yet

- $$ Final Indian Finanacial System 2$Document112 pages$$ Final Indian Finanacial System 2$Kumaran VelNo ratings yet

- Impact of Financial Development On Economic Growth of PakistanDocument11 pagesImpact of Financial Development On Economic Growth of PakistanAhmad Ali Kasuri AdvNo ratings yet

- OF Finance Sector in India: Policies and Performance AnalysisDocument13 pagesOF Finance Sector in India: Policies and Performance AnalysisrajourNo ratings yet

- Financial Sector Reforms in India: Policies and Performance AnalysisDocument27 pagesFinancial Sector Reforms in India: Policies and Performance AnalysisVijay Kumar SrivastavaNo ratings yet

- Final Indian FinanacialsystemDocument111 pagesFinal Indian FinanacialsystemMonica NatarajanNo ratings yet

- Role of Money Related Showcase in Development of Indian EconomyDocument4 pagesRole of Money Related Showcase in Development of Indian EconomyInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Financial SectorDocument24 pagesFinancial SectorJitendra TandelNo ratings yet

- Jurnal BPPK: Volume 1, Nomor 4, Oktober 2010Document43 pagesJurnal BPPK: Volume 1, Nomor 4, Oktober 2010danielNo ratings yet

- FM - Financial Development and Economic Growth 25042015Document10 pagesFM - Financial Development and Economic Growth 25042015NaDiaNo ratings yet

- CHAPTER VII - Summary & ConclusionDocument5 pagesCHAPTER VII - Summary & ConclusionAnkit SinghNo ratings yet

- The Cause-Effect Relationship Between Economic Growth and Stock Market Development - The Case of VietnamDocument22 pagesThe Cause-Effect Relationship Between Economic Growth and Stock Market Development - The Case of VietnamTrang Nguyễn Ngọc Hồng TrangNo ratings yet

- Chapter-1 Introduction To The Financial SystemDocument24 pagesChapter-1 Introduction To The Financial SystemwubeNo ratings yet

- Financial Market Evolution and GlobalisationDocument34 pagesFinancial Market Evolution and GlobalisationSanket GarjeNo ratings yet

- Capital Markets, Economic Growth and Sustainable Development Financing: A Case Study of NigeriaDocument12 pagesCapital Markets, Economic Growth and Sustainable Development Financing: A Case Study of Nigeriahayatudin jusufNo ratings yet

- MPRA Paper 2145Document18 pagesMPRA Paper 2145Obaid GillNo ratings yet

- Eco Growth Report MiteshDocument1 pageEco Growth Report MiteshMitesh BidNo ratings yet

- Disha Agarwal (1) Financial Services BNFDocument20 pagesDisha Agarwal (1) Financial Services BNFdisha agarwalNo ratings yet

- Introduction of Financial InstitutionDocument12 pagesIntroduction of Financial InstitutionGanesh Kumar100% (2)

- Unit 2 Money Market 2Document9 pagesUnit 2 Money Market 2mkmahesh813No ratings yet

- Jurnal Int MakroDocument13 pagesJurnal Int MakroiawidhiantiniNo ratings yet

- MPRA Paper 81201Document29 pagesMPRA Paper 81201shagun khandelwalNo ratings yet

- Toyin Chapter OneDocument96 pagesToyin Chapter OneKadri Adebayo MISNo ratings yet

- 08 - Chapter 3 PDFDocument68 pages08 - Chapter 3 PDFJavedNo ratings yet

- The Impact of Financial Development On Economic Growth of NigeriaDocument13 pagesThe Impact of Financial Development On Economic Growth of NigeriaPORI ENTERPRISESNo ratings yet

- Economic Development and The Functionality of The Financial SystemDocument27 pagesEconomic Development and The Functionality of The Financial SystemMarcosNo ratings yet

- 13 LitianDocument4 pages13 Litianrush2raazNo ratings yet

- Financial SystemDocument161 pagesFinancial SystemMpho Peloewtse TauNo ratings yet

- Solution Manual For Introduction To Finance Markets Investments and Financial Management 16th EditionDocument18 pagesSolution Manual For Introduction To Finance Markets Investments and Financial Management 16th EditionDawn Steward100% (40)

- My Publication, PESR, CAL and GrowthDocument15 pagesMy Publication, PESR, CAL and GrowthAtiq ur Rehman QamarNo ratings yet

- Financial Institutions and MarketsDocument283 pagesFinancial Institutions and MarketsGood Anony7No ratings yet

- Financial Markets: The Recent Experience of A Developing EconomyDocument15 pagesFinancial Markets: The Recent Experience of A Developing EconomyVedant BhansaliNo ratings yet

- Finance and Economic DevelopmentDocument26 pagesFinance and Economic DevelopmentHardeep SinghNo ratings yet

- Updates On JAIIB/CAIIB Papers Note:: Module ADocument15 pagesUpdates On JAIIB/CAIIB Papers Note:: Module ARamasundaram TNo ratings yet

- Financial System and Financial MarketsDocument11 pagesFinancial System and Financial MarketsHariNo ratings yet

- FIM PresentationDocument14 pagesFIM Presentationsomeone specialNo ratings yet

- Chapter One Extinction of ObligationsDocument46 pagesChapter One Extinction of ObligationsHemen zinahbizuNo ratings yet

- HSBC iPad-iPod Touch Application FormDocument1 pageHSBC iPad-iPod Touch Application FormBc CyNo ratings yet

- Gap Thesis and The Survival of Informal Financial Sector in NigeriaDocument6 pagesGap Thesis and The Survival of Informal Financial Sector in NigeriaMadiha MunirNo ratings yet

- CH 01 - QS 1-17-18 Ac 3-4Document14 pagesCH 01 - QS 1-17-18 Ac 3-4Sharmi laNo ratings yet

- Tutorial - Chapter 11 - Monetary Policy - QuestionsDocument4 pagesTutorial - Chapter 11 - Monetary Policy - QuestionsNandiieNo ratings yet

- iPAY International S.A. 2014Document20 pagesiPAY International S.A. 2014LuxembourgAtaGlanceNo ratings yet

- Manual of Regulation For BanksDocument27 pagesManual of Regulation For BanksCLAINE AVELINONo ratings yet

- A Study On Working CapitalDocument92 pagesA Study On Working CapitalNeehasultana ShaikNo ratings yet

- Finance Master Thesis PDFDocument7 pagesFinance Master Thesis PDFafkojbvmz100% (2)

- Suryaa Hotel Bal SheetDocument3 pagesSuryaa Hotel Bal Sheetarjun chauhan100% (1)

- Tabel DFDocument15 pagesTabel DFSexy TofuNo ratings yet

- B1 How To Deal With Money LIU006: WWW - English-Practice - atDocument1 pageB1 How To Deal With Money LIU006: WWW - English-Practice - atIoana-Daniela PîrvuNo ratings yet

- Brokerage Agreement-ExclusiveDocument3 pagesBrokerage Agreement-ExclusiveMarvin B. SoteloNo ratings yet

- NEW DT Bullet (MCQ'S) by CA Saumil Manglani - CS Exec June 22 & Dec 22 ExamsDocument168 pagesNEW DT Bullet (MCQ'S) by CA Saumil Manglani - CS Exec June 22 & Dec 22 ExamsAkash MalikNo ratings yet

- DanielDocument17 pagesDanielJerome MogaNo ratings yet

- InvoiceDocument2 pagesInvoiceTHIMMEGOWDA H MNo ratings yet

- Loyalty Card Plus: Application FormDocument2 pagesLoyalty Card Plus: Application FormKillah BeatsNo ratings yet

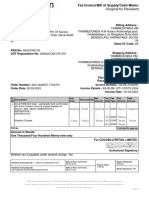

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)raviNo ratings yet

- (Springer Finance) Dr. Manuel Ammann (Auth.) - Credit Risk Valuation - Methods, Models, and Applications-Springer Berlin Heidelberg (2001)Document258 pages(Springer Finance) Dr. Manuel Ammann (Auth.) - Credit Risk Valuation - Methods, Models, and Applications-Springer Berlin Heidelberg (2001)Amel AmarNo ratings yet

- AccountingDocument8 pagesAccountingfransiscaNo ratings yet

- Pifra Business Finance ProjectDocument17 pagesPifra Business Finance ProjectWaqas AhmedNo ratings yet

- BBA Sem - II Syllabus - 13.112019Document28 pagesBBA Sem - II Syllabus - 13.112019Gaurav BuchkulNo ratings yet

- UaeDocument134 pagesUaeJad LouisNo ratings yet

- Electronic Trading ConceptsDocument98 pagesElectronic Trading ConceptsAnurag TripathiNo ratings yet

- NBFCDocument52 pagesNBFCDrRajdeep SinghNo ratings yet

- Midterm I 2022 KEYDocument17 pagesMidterm I 2022 KEYkuo zoeNo ratings yet

- Solved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedDocument1 pageSolved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedAnbu jaromiaNo ratings yet

- CISI Exam Booking Instructions-1Document4 pagesCISI Exam Booking Instructions-1simon.dk.designerNo ratings yet

- PT Astra Agro Lestari TBK.: Summary of Financial StatementDocument2 pagesPT Astra Agro Lestari TBK.: Summary of Financial StatementIntan Maulida SuryaningsihNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsFrom EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNo ratings yet

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsFrom EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsRating: 5 out of 5 stars5/5 (1)

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondFrom EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNo ratings yet

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)From EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Rating: 4 out of 5 stars4/5 (5)