You might also like

- Ch10solution ManualDocument31 pagesCh10solution ManualJyunde WuNo ratings yet

- 2021 Carlyle Investor Day PresentationDocument229 pages2021 Carlyle Investor Day PresentationJay ZNo ratings yet

- Introduction PepsicoDocument28 pagesIntroduction PepsicoKaran Shoor67% (3)

- Value-based financial management: Towards a Systematic Process for Financial Decision - MakingFrom EverandValue-based financial management: Towards a Systematic Process for Financial Decision - MakingNo ratings yet

- Portfolio Perspectives September 2019 PDFDocument16 pagesPortfolio Perspectives September 2019 PDFgpNo ratings yet

- Chapter 4 ZicaDocument62 pagesChapter 4 ZicaTh'bo Muzorewa ChizyukaNo ratings yet

- Global Monthly Perspectives (May 2021)Document29 pagesGlobal Monthly Perspectives (May 2021)masterumNo ratings yet

- Rating Action:: Moody's Upgrades Indonesia's Sovereign Rating To Baa3 Outlook StableDocument5 pagesRating Action:: Moody's Upgrades Indonesia's Sovereign Rating To Baa3 Outlook StableMelyastarda SiregarNo ratings yet

- Blog - Fed Watch Nifty FiftyDocument3 pagesBlog - Fed Watch Nifty FiftyOwm Close CorporationNo ratings yet

- Global Macro Commentary July 14Document2 pagesGlobal Macro Commentary July 14dpbasicNo ratings yet

- Bullish Under The Hood December Policy TakeawaysDocument3 pagesBullish Under The Hood December Policy Takeawaysvishal_lal89No ratings yet

- The Contra-QE Trade LoomsDocument3 pagesThe Contra-QE Trade LoomsdpbasicNo ratings yet

- February Monthly LetterDocument2 pagesFebruary Monthly LetterTheLernerGroupNo ratings yet

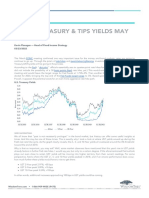

- Blog - Where Treasury TIPS Yields May Be HeadedDocument5 pagesBlog - Where Treasury TIPS Yields May Be HeadedOwm Close CorporationNo ratings yet

- 2013 q2 Crescent Commentary Steve RomickDocument16 pages2013 q2 Crescent Commentary Steve RomickCanadianValueNo ratings yet

- (LGT) 20210316 - DRU - Sector RotationDocument3 pages(LGT) 20210316 - DRU - Sector RotationRuehYinn YapNo ratings yet

- Breaking From Tradition: in This Bear Market, Growth OutperformedDocument3 pagesBreaking From Tradition: in This Bear Market, Growth OutperformedSharkyNo ratings yet

- Determinants of Sovereign Credit RatingsDocument50 pagesDeterminants of Sovereign Credit RatingsRuben Carlo AsuncionNo ratings yet

- Black Diamond Global Enhanced Income Fund MRFP 2022-12-31Document8 pagesBlack Diamond Global Enhanced Income Fund MRFP 2022-12-31T.A.P.ExE.CEONo ratings yet

- Global Fixed IncomeDocument5 pagesGlobal Fixed IncomeSpeculation OnlyNo ratings yet

- Global Macro Commentary Jan 13Document2 pagesGlobal Macro Commentary Jan 13dpbasicNo ratings yet

- Market Monitor 4Document3 pagesMarket Monitor 4Susan LaskoNo ratings yet

- Motilal Oswal-Market Valuation Apr 2020Document5 pagesMotilal Oswal-Market Valuation Apr 2020ramkrishna mahatoNo ratings yet

- OLLI ICR 2018 Final - V8Document26 pagesOLLI ICR 2018 Final - V8Ala BasterNo ratings yet

- QMU Underperformance in Fixed Income Markets IFS FINAL 3.22.12 ADADocument3 pagesQMU Underperformance in Fixed Income Markets IFS FINAL 3.22.12 ADAPaulo AraujoNo ratings yet

- Ltcma Full ReportDocument150 pagesLtcma Full ReportJuan José Solis DelgadoNo ratings yet

- Global Macro Commentary July 21 - Too Much of EverythingDocument2 pagesGlobal Macro Commentary July 21 - Too Much of EverythingdpbasicNo ratings yet

- Global Macro Commentary April 2Document3 pagesGlobal Macro Commentary April 2dpbasicNo ratings yet

- NBC Financial Group MonthlyDocument8 pagesNBC Financial Group MonthlyMiir ViirNo ratings yet

- CMO BofA 02-05-2024 AdaDocument8 pagesCMO BofA 02-05-2024 AdaAlejandroNo ratings yet

- Moodys Disclosures On Credit Ratings of Fiji - 19 January 2012Document5 pagesMoodys Disclosures On Credit Ratings of Fiji - 19 January 2012Intelligentsiya HqNo ratings yet

- Global Macro Commentary Jan 7Document2 pagesGlobal Macro Commentary Jan 7dpbasicNo ratings yet

- CA Final SFM Compiler Ver 6.0Document452 pagesCA Final SFM Compiler Ver 6.0Accounts Primesoft100% (1)

- Doshi Gama Fund April 2013Document2 pagesDoshi Gama Fund April 2013ados1984No ratings yet

- Investor Presentation: Fourth Quarter 2021Document41 pagesInvestor Presentation: Fourth Quarter 2021orvinwankeNo ratings yet

- Hussman 112513Document18 pagesHussman 112513alphathesisNo ratings yet

- 06.14.22 Market Sense Final DeckDocument16 pages06.14.22 Market Sense Final DeckRhytham SoniNo ratings yet

- R03 Capital Market Expectations, Part 1 - Framework and Macro Considerations HY NotesDocument7 pagesR03 Capital Market Expectations, Part 1 - Framework and Macro Considerations HY NotesArcadioNo ratings yet

- Global Outperformers Jenga Investment Partners LTDDocument287 pagesGlobal Outperformers Jenga Investment Partners LTDEdsel RaperNo ratings yet

- The Future of Your Wealth: How the World Is Changing and What You Need to Do about It: A Guide for High Net Worth Individuals and FamiliesFrom EverandThe Future of Your Wealth: How the World Is Changing and What You Need to Do about It: A Guide for High Net Worth Individuals and FamiliesNo ratings yet

- Empower June 2012Document68 pagesEmpower June 2012pravin963No ratings yet

- Summer InsectsDocument72 pagesSummer InsectsCanadianValue0% (1)

- Analysis and Uses of Financial StatementsDocument144 pagesAnalysis and Uses of Financial StatementsPepe ArriagaNo ratings yet

- ValuEngine Weekly Newsletter January 27, 2012Document12 pagesValuEngine Weekly Newsletter January 27, 2012ValuEngine.comNo ratings yet

- Global Macro Commentary March 12Document2 pagesGlobal Macro Commentary March 12dpbasicNo ratings yet

- Does Dividend Policy Foretell Earnings Growth?: Draft: December 2001 Comments WelcomeDocument34 pagesDoes Dividend Policy Foretell Earnings Growth?: Draft: December 2001 Comments WelcomeSnehanshu BanerjeeNo ratings yet

- Global Macro Commentary Feb 26Document2 pagesGlobal Macro Commentary Feb 26dpbasicNo ratings yet

- CMO BofA 02-12-2024 AdaDocument8 pagesCMO BofA 02-12-2024 AdaAlejandroNo ratings yet

- OriginalDocument52 pagesOriginalmdyafi8084No ratings yet

- Cifre PepsiDocument59 pagesCifre PepsiOana ModreanuNo ratings yet

- Gathering Speed - Update On The Monetary Policy - June 2022Document5 pagesGathering Speed - Update On The Monetary Policy - June 2022Huzefa BharmalNo ratings yet

- Q322 Investor PresentationDocument42 pagesQ322 Investor PresentationAlex ENo ratings yet

- The Investment ClockDocument4 pagesThe Investment ClockJean Carlos TorresNo ratings yet

- What Shares Should I Buy (Important Pe Vs MKTG)Document35 pagesWhat Shares Should I Buy (Important Pe Vs MKTG)Fify AhmadNo ratings yet

- May Monthly LetterDocument2 pagesMay Monthly LetterTheLernerGroupNo ratings yet

- ID2021 CapitalRaising Urquhart FINALDocument20 pagesID2021 CapitalRaising Urquhart FINALHemad IksdaNo ratings yet

- er20130211BullPhatDragon PDFDocument2 pageser20130211BullPhatDragon PDFAmanda MooreNo ratings yet

- Blackrock - Going Direct 2019Document16 pagesBlackrock - Going Direct 2019garchev100% (1)

- Apollo Global Management Credit Outlook 1706830735Document55 pagesApollo Global Management Credit Outlook 1706830735ducnguyentcbNo ratings yet

- Larry Robbins Glenview Capital Ira Sohn 2014 PresentationDocument49 pagesLarry Robbins Glenview Capital Ira Sohn 2014 Presentationmarketfolly.comNo ratings yet

- From Calamity to Stability: Harnessing the Wisdom of Past Financial Crises to Build a Stable and Resilient Global Financial SystemFrom EverandFrom Calamity to Stability: Harnessing the Wisdom of Past Financial Crises to Build a Stable and Resilient Global Financial SystemNo ratings yet

- Financial Intelligence: Navigating the Numbers in BusinessFrom EverandFinancial Intelligence: Navigating the Numbers in BusinessNo ratings yet

- Successful Defined Contribution Investment Design: How to Align Target-Date, Core, and Income Strategies to the PRICE of RetirementFrom EverandSuccessful Defined Contribution Investment Design: How to Align Target-Date, Core, and Income Strategies to the PRICE of RetirementNo ratings yet

- The Internet Bubble Bursts On The Screen Documentary Shows Brief Life of A Dot-Com - The New York TimesDocument5 pagesThe Internet Bubble Bursts On The Screen Documentary Shows Brief Life of A Dot-Com - The New York TimesblacksmithMGNo ratings yet

- Sanjay+Gospodinov+ +nvidiaDocument16 pagesSanjay+Gospodinov+ +nvidiablacksmithMGNo ratings yet

- Do Stocks Outperform Treasury BillsDocument53 pagesDo Stocks Outperform Treasury BillsblacksmithMGNo ratings yet

- Starting Over Again - The Covid-19 Pandemic Is Forcing A Rethink in Macroeconomics - Briefing - The EconomistDocument20 pagesStarting Over Again - The Covid-19 Pandemic Is Forcing A Rethink in Macroeconomics - Briefing - The EconomistblacksmithMGNo ratings yet

- Future of Work and SkillsDocument24 pagesFuture of Work and SkillsblacksmithMGNo ratings yet

- US Faces Inflation Threat As Money Supply Rockets - Financial TimesDocument2 pagesUS Faces Inflation Threat As Money Supply Rockets - Financial TimesblacksmithMGNo ratings yet

- ETF Flash Crash of August 24 2015 and Insane Bid-Ask Spreads (Working Paper)Document4 pagesETF Flash Crash of August 24 2015 and Insane Bid-Ask Spreads (Working Paper)blacksmithMGNo ratings yet

- Return of InflationDocument21 pagesReturn of InflationblacksmithMGNo ratings yet

- Looking Back Going Forward: Long Term Global GrowthDocument60 pagesLooking Back Going Forward: Long Term Global GrowthblacksmithMGNo ratings yet

- Mi Bothsidesenergy enDocument8 pagesMi Bothsidesenergy enblacksmithMGNo ratings yet

- TOP Mind: 2020 UPDATE, and A Peek at 2021Document10 pagesTOP Mind: 2020 UPDATE, and A Peek at 2021blacksmithMGNo ratings yet

- Outlook 2021Document39 pagesOutlook 2021blacksmithMGNo ratings yet

- The Big Market Delusion Valuation and Investment ImplicationsDocument12 pagesThe Big Market Delusion Valuation and Investment ImplicationsblacksmithMGNo ratings yet

- Asset Bubbles and Where To Find Them: Commentary by Joe Davis, Vanguard Global Chief EconomistDocument4 pagesAsset Bubbles and Where To Find Them: Commentary by Joe Davis, Vanguard Global Chief EconomistblacksmithMGNo ratings yet

- Our Shared Beliefs: Baillie GiffordDocument16 pagesOur Shared Beliefs: Baillie GiffordblacksmithMGNo ratings yet

- Assignment On NAFTADocument6 pagesAssignment On NAFTAnur naher muktaNo ratings yet

- Exhibit 3.1 Articles of Incorporation of Merchandise Creations, IncDocument4 pagesExhibit 3.1 Articles of Incorporation of Merchandise Creations, IncJazcel GalsimNo ratings yet

- Provisional Certificate PDFDocument2 pagesProvisional Certificate PDFShubhamNo ratings yet

- Mergersand Acquisitionsonthe Polish Capital MarketDocument11 pagesMergersand Acquisitionsonthe Polish Capital MarketPrashant KumbarNo ratings yet

- Ram SAP MM Class StatuscssDocument15 pagesRam SAP MM Class StatuscssAll rounderzNo ratings yet

- Final Question Bank Xii Accoutancy-2022-23Document206 pagesFinal Question Bank Xii Accoutancy-2022-23Khushi Sharma100% (1)

- Bajaj Auto: Presented By:-ITM Bschool Navi Mumbai KhargharDocument23 pagesBajaj Auto: Presented By:-ITM Bschool Navi Mumbai KhargharDeepali KunjeerNo ratings yet

- Malhotra MarketingResearchAWE PPT Ch02Document25 pagesMalhotra MarketingResearchAWE PPT Ch02maria bitarNo ratings yet

- Profit Planning Discussion ProblemsDocument5 pagesProfit Planning Discussion ProblemsVatchdemonNo ratings yet

- Property Law - II 38Document24 pagesProperty Law - II 38raj kkNo ratings yet

- Documentation: Manufacture, Control and DistributionDocument10 pagesDocumentation: Manufacture, Control and DistributionAyalew DesyeNo ratings yet

- Kunci Jawaban CH 1pdf PDF FreeDocument44 pagesKunci Jawaban CH 1pdf PDF FreeNajwa KhansaNo ratings yet

- LeadsDocument47 pagesLeadsZuqo SalesNo ratings yet

- Johnny Doc Criminal Complaint 2021Document8 pagesJohnny Doc Criminal Complaint 2021philly victorNo ratings yet

- Petissu (Final)Document51 pagesPetissu (Final)Patricia SantosNo ratings yet

- Astm F2974-18Document2 pagesAstm F2974-18Martin TapankovNo ratings yet

- Payments Card Includes Credit Cards and Debit CardsDocument6 pagesPayments Card Includes Credit Cards and Debit CardsdivyavishalNo ratings yet

- BondsDocument19 pagesBondsSam SamNo ratings yet

- The 2014 Global Innovation Media Report - PWCDocument7 pagesThe 2014 Global Innovation Media Report - PWCMohammad Umer InamNo ratings yet

- G FR Procurement 2Document94 pagesG FR Procurement 2anshuranijhaNo ratings yet

- Ra 7160Document191 pagesRa 7160Ford OsipNo ratings yet

- Chapter Three: International Trade and Foreign Direct InvestmentDocument48 pagesChapter Three: International Trade and Foreign Direct InvestmentLicece ImhNo ratings yet

- 408 Tax Case BriefDocument256 pages408 Tax Case BriefIsabel Luchie GuimaryNo ratings yet

- Qualitative Process Analysis 1Document42 pagesQualitative Process Analysis 1mtahir777945No ratings yet

- IGCSE Business Studies-2017-2019-SyllabusDocument30 pagesIGCSE Business Studies-2017-2019-Syllabusnmrasa100% (1)

- 2023-Report-Annual-Marketing-En - Shared by WorldLine TechnologypdfDocument28 pages2023-Report-Annual-Marketing-En - Shared by WorldLine TechnologypdfThuy NghiemNo ratings yet

- Accounting Worksheet Problems and SolutionsDocument1 pageAccounting Worksheet Problems and SolutionsPauline BiancaNo ratings yet