You might also like

- AUDITING - PRELIM - For PrintingDocument4 pagesAUDITING - PRELIM - For PrintingAndreiu Mark EsmeleNo ratings yet

- MINDANAO MISSION ACADEMY Accountancy Exam ReviewDocument2 pagesMINDANAO MISSION ACADEMY Accountancy Exam ReviewHLeigh Nietes-GabutanNo ratings yet

- Auditing Problems: First PreboardDocument8 pagesAuditing Problems: First PreboardCarlo AgravanteNo ratings yet

- Chapter 1 Cash and Cash Equivalent ProjectDocument8 pagesChapter 1 Cash and Cash Equivalent ProjectJohn Carlo DelorinoNo ratings yet

- Mindanao Mission Academy Accountancy ExamDocument4 pagesMindanao Mission Academy Accountancy ExamHLeigh Nietes-GabutanNo ratings yet

- ExtAud 3 Midterm Exam W AnswersDocument12 pagesExtAud 3 Midterm Exam W AnswersJANET ILLESESNo ratings yet

- Fundamentals of Accounting2-FinalDocument3 pagesFundamentals of Accounting2-FinalHLeigh Nietes-GabutanNo ratings yet

- AP 2nd Monthly AssessmentDocument6 pagesAP 2nd Monthly AssessmentCiena Mae AsasNo ratings yet

- Audit of CashDocument4 pagesAudit of CashBromanineNo ratings yet

- Cup 1 FA 1 and FA 2Document16 pagesCup 1 FA 1 and FA 2Thony Danielle LabradorNo ratings yet

- Part 1: Reviewer#5: Midterm Quiz 9fundamentals of Accounting 1 & 2)Document5 pagesPart 1: Reviewer#5: Midterm Quiz 9fundamentals of Accounting 1 & 2)annedanyle acabadoNo ratings yet

- DIY Drill AuditDocument7 pagesDIY Drill AuditRoniella Liezyl Glindro CanlasNo ratings yet

- QE With Solutions 1st YearDocument6 pagesQE With Solutions 1st YearJeryco Quijano BrionesNo ratings yet

- A. Crossword: Complete The Crossword by Referring To The Questions BelowDocument4 pagesA. Crossword: Complete The Crossword by Referring To The Questions BelowHLeigh Nietes-GabutanNo ratings yet

- Đề thi thử Intern EY 2022Document117 pagesĐề thi thử Intern EY 2022Minh Nhật BùiNo ratings yet

- EASY ROUND INCOME TAXESDocument13 pagesEASY ROUND INCOME TAXESCamila Mae AlduezaNo ratings yet

- Audit of Cash - SeatworkDocument4 pagesAudit of Cash - SeatworkTEOPE, EMERLIZA DE CASTRONo ratings yet

- Calculating Cash and Cash EquivalentsDocument4 pagesCalculating Cash and Cash EquivalentsGlydell MapayeNo ratings yet

- Mexican Corp Accounts Receivable AdjustmentsDocument4 pagesMexican Corp Accounts Receivable AdjustmentsA.B AmpuanNo ratings yet

- Long Quiz 1 Acc 205Document6 pagesLong Quiz 1 Acc 205Philip LarozaNo ratings yet

- College Accounting Final ExamDocument17 pagesCollege Accounting Final ExamAiron Keith Along100% (1)

- ACC17-FAR Take Home Activities 1 and 2: Test IDocument19 pagesACC17-FAR Take Home Activities 1 and 2: Test IJustine Cruz67% (3)

- FAR Handout 03 - Trade ReceivablesDocument4 pagesFAR Handout 03 - Trade ReceivablesadieNo ratings yet

- Receivables QuizDocument2 pagesReceivables Quizhoneyjoy salapantanNo ratings yet

- Auditing and Assurance Quiz, Cash and Cash EquivalentsDocument5 pagesAuditing and Assurance Quiz, Cash and Cash EquivalentswesNo ratings yet

- Petty Cash Audit and Bank ReconciliationDocument50 pagesPetty Cash Audit and Bank ReconciliationJohn Lloyd Yasto100% (1)

- Fundamentals of AccountingDocument5 pagesFundamentals of AccountingHLeigh Nietes-GabutanNo ratings yet

- Quiz With Solutions IA 1 2nd YearsDocument6 pagesQuiz With Solutions IA 1 2nd YearsJeryco Quijano BrionesNo ratings yet

- 2021 Prelim Exam Auditing Concepts and Applications 1Document15 pages2021 Prelim Exam Auditing Concepts and Applications 1moreNo ratings yet

- Acc106 ReviewersDocument15 pagesAcc106 ReviewersJulina Olsim EstudNo ratings yet

- 5 6248879817396060958Document6 pages5 6248879817396060958Jeff GonzalesNo ratings yet

- F CFAS-EXAM - Docx 143874436Document48 pagesF CFAS-EXAM - Docx 143874436Athena AthenaNo ratings yet

- ACC 140 1 Period - Quiz 2Document7 pagesACC 140 1 Period - Quiz 2Rica Mille MartinNo ratings yet

- St. Peter's College Acctg 22 Auditing Final ExamDocument6 pagesSt. Peter's College Acctg 22 Auditing Final Exammarx marolinaNo ratings yet

- Auditing Cash Procedures & Bank ReconciliationsDocument9 pagesAuditing Cash Procedures & Bank ReconciliationsRizzel SubaNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaEsse ValdezNo ratings yet

- Accounting10 (Reviewer)Document5 pagesAccounting10 (Reviewer)Erika Panit ReyesNo ratings yet

- Receivable-FinancingDocument2 pagesReceivable-Financingjohnreydomingo98No ratings yet

- Accounting Process Discussion ExercisesDocument3 pagesAccounting Process Discussion ExercisesCathlyn PatalitaNo ratings yet

- Principles Seifu Work SheetDocument5 pagesPrinciples Seifu Work SheetYonas85% (13)

- The current ratio informs you about a company's liquidityDocument3 pagesThe current ratio informs you about a company's liquidityCarlo ParasNo ratings yet

- FARDocument222 pagesFARAireNo ratings yet

- Refresher Course: Audit of Cash and Cash EquivalentsDocument4 pagesRefresher Course: Audit of Cash and Cash EquivalentsFery Ann100% (1)

- KALBARYONISHERLY2Document8 pagesKALBARYONISHERLY2De MarcusNo ratings yet

- AP - 02 LOANS AND RECEIVALBES With Answer PDFDocument12 pagesAP - 02 LOANS AND RECEIVALBES With Answer PDFJymldy Encln67% (3)

- (123doc) - Tai-Lieu-Accounting-Principles-Mid-Semester-Test PDFDocument4 pages(123doc) - Tai-Lieu-Accounting-Principles-Mid-Semester-Test PDFTrung HậuNo ratings yet

- Audit of CashDocument3 pagesAudit of CashCleopha Mae Torres100% (3)

- Final Exam 12 PDF FreeDocument17 pagesFinal Exam 12 PDF FreeEmey CalbayNo ratings yet

- Audit of Cash LecturesDocument3 pagesAudit of Cash Lecturespekka172No ratings yet

- Bank Reconciliation HandoutsDocument7 pagesBank Reconciliation HandoutsRODELYN PERALESNo ratings yet

- Acc 106 Quiz BR and Ar NoakDocument8 pagesAcc 106 Quiz BR and Ar Noakhoneyjoy salapantanNo ratings yet

- Questionnaire-Practical Accounting 1 Test I: Answer The FollowingDocument10 pagesQuestionnaire-Practical Accounting 1 Test I: Answer The FollowingKristee PlanesNo ratings yet

- Final Intermediate 1 2015 2016Document10 pagesFinal Intermediate 1 2015 2016ZeeNo ratings yet

- BS Accountancy Midterm Exam ReviewDocument4 pagesBS Accountancy Midterm Exam ReviewPineda, King Moises PangilinanNo ratings yet

- Practice Problem 2 Cash ReconDocument5 pagesPractice Problem 2 Cash ReconKhyla DivinagraciaNo ratings yet

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)From EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Project Management Accounting: Budgeting, Tracking, and Reporting Costs and ProfitabilityFrom EverandProject Management Accounting: Budgeting, Tracking, and Reporting Costs and ProfitabilityRating: 4 out of 5 stars4/5 (2)

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- Calculate current and non-current liabilities for financial statementDocument11 pagesCalculate current and non-current liabilities for financial statementJane GavinoNo ratings yet

- VALLEJOS ACCTG 301 Biological Assets Answer KeyDocument4 pagesVALLEJOS ACCTG 301 Biological Assets Answer KeyEllah Rah78% (9)

- Internal Audit Practice From A To Z PDFDocument675 pagesInternal Audit Practice From A To Z PDFKarim Adam100% (1)

- Maximizing Profit with Linear ProgrammingDocument8 pagesMaximizing Profit with Linear ProgrammingJoshua DelgadoNo ratings yet

- SALIC Chapter 10 and 11 pp.629 646Document5 pagesSALIC Chapter 10 and 11 pp.629 646Jane GavinoNo ratings yet

- Ho 1 Pre-Work AnswerDocument2 pagesHo 1 Pre-Work AnswerJane GavinoNo ratings yet

- Northern CPA Review Co. (NCPAR)Document12 pagesNorthern CPA Review Co. (NCPAR)Dieter LudwigNo ratings yet

- Final Examination Acc4Document7 pagesFinal Examination Acc4Jane GavinoNo ratings yet

- A Firm That Engages in Foreign Direct Investment (FDI) in Other Countries Is Called A (N)Document4 pagesA Firm That Engages in Foreign Direct Investment (FDI) in Other Countries Is Called A (N)Jane GavinoNo ratings yet

- Chapter 1Document1 pageChapter 1Jane GavinoNo ratings yet

- Internal controls for production cycleDocument39 pagesInternal controls for production cycleJane GavinoNo ratings yet

- Internal Control ConceptsDocument18 pagesInternal Control ConceptsJane GavinoNo ratings yet

- Handout No. 1 Answers 1 To 4Document2 pagesHandout No. 1 Answers 1 To 4Jane GavinoNo ratings yet

- Acc 113 2nd Periodical Examination PDF FreeDocument17 pagesAcc 113 2nd Periodical Examination PDF FreeStefanie FerminNo ratings yet

- Quizzer Cash - Solution Printed KoDocument119 pagesQuizzer Cash - Solution Printed Kogoerginamarquez80% (10)

- QuelDocument1 pageQuelJane GavinoNo ratings yet

- Exercise InvestmentsDocument1 pageExercise InvestmentsJane GavinoNo ratings yet

- Start CallistoDocument5 pagesStart CallistoJane GavinoNo ratings yet

- CPA Review: Auditing Theory and Other ServicesDocument6 pagesCPA Review: Auditing Theory and Other ServicesshambiruarNo ratings yet

- Handout No. 1 Answers 1 To 4Document2 pagesHandout No. 1 Answers 1 To 4Jane GavinoNo ratings yet

- Testbank AuditingDocument57 pagesTestbank AuditingJane Gavino100% (1)

- Star Callisto - Astrologer: Professional SummaryDocument2 pagesStar Callisto - Astrologer: Professional SummaryJane GavinoNo ratings yet

- Auditing Theory 250 QuestionsDocument39 pagesAuditing Theory 250 Questionsxxxxxxxxx75% (4)

- Corporate Liquidation & Reorganization Chapter ExplainedDocument4 pagesCorporate Liquidation & Reorganization Chapter ExplainedJane GavinoNo ratings yet

- Correct Financial Records ErrorsDocument7 pagesCorrect Financial Records ErrorsJoy Miraflor AlinoodNo ratings yet

- Start CallistoDocument5 pagesStart CallistoJane GavinoNo ratings yet

- Corporate Liquidation & Reorganization Chapter ExplainedDocument4 pagesCorporate Liquidation & Reorganization Chapter ExplainedJane GavinoNo ratings yet

- Star Callisto - Astrologer: Professional SummaryDocument2 pagesStar Callisto - Astrologer: Professional SummaryJane GavinoNo ratings yet

- Answers To Final ExamsDocument42 pagesAnswers To Final ExamsMd. Jahangir AlamNo ratings yet

- Quiz 2 Joint ArrangementsDocument4 pagesQuiz 2 Joint ArrangementsJane Gavino100% (2)

- Npioh, Jurnal Sugandi Maida 594-599Document6 pagesNpioh, Jurnal Sugandi Maida 594-599Nona InnasyaNo ratings yet

- FRM Test 03 - Topic - TVM + Mutual FundsDocument20 pagesFRM Test 03 - Topic - TVM + Mutual FundsKamal BhatiaNo ratings yet

- ABC - PFRS 3 Final Exam ReviewDocument17 pagesABC - PFRS 3 Final Exam ReviewCristel TannaganNo ratings yet

- FABM 1 Lesson 6 Accounting Concepts and PrinciplesDocument3 pagesFABM 1 Lesson 6 Accounting Concepts and PrinciplesTiffany CenizaNo ratings yet

- Financial Management On Catfish Farms (PDFDrive)Document61 pagesFinancial Management On Catfish Farms (PDFDrive)AmiibahNo ratings yet

- Fintech Report Estonia 2019: October 2019Document45 pagesFintech Report Estonia 2019: October 2019Alessandro AventaggiatoNo ratings yet

- ECON 118:: Chapter: None, "Advanced Accounting Intro, A Catch-Up"Document38 pagesECON 118:: Chapter: None, "Advanced Accounting Intro, A Catch-Up"Danny StevensonNo ratings yet

- Electronic Contribution Collection List SummaryDocument2 pagesElectronic Contribution Collection List SummaryMark Kevin IIINo ratings yet

- IAS 28 Example: Accounting For A Downstream Transaction: Last Updated: 11/8/2018Document3 pagesIAS 28 Example: Accounting For A Downstream Transaction: Last Updated: 11/8/2018devanand bhawNo ratings yet

- RES 3200 Chapter 2 Real Estate FinancingDocument12 pagesRES 3200 Chapter 2 Real Estate FinancingbaorunchenNo ratings yet

- Axis Fixed Term PlansDocument213 pagesAxis Fixed Term PlansCuriousMan87No ratings yet

- Bajaj Allianz General Insurance Company LTD.: Declaration by The InsuredDocument1 pageBajaj Allianz General Insurance Company LTD.: Declaration by The InsuredArtiNo ratings yet

- Transaction Procedures Purchase Sblc-Lloyds Bank LTDDocument2 pagesTransaction Procedures Purchase Sblc-Lloyds Bank LTDMANOJ VIJAYANNo ratings yet

- Accounting Oral ExamDocument5 pagesAccounting Oral ExamalmmuuhNo ratings yet

- CAT Level 2 QuestionnairesDocument16 pagesCAT Level 2 QuestionnairesRona Amor MundaNo ratings yet

- CertificateDocument4 pagesCertificateMilap NaiduNo ratings yet

- October Month Current AffairsDocument87 pagesOctober Month Current AffairsSantosh Kumar ChallaNo ratings yet

- CPIPG Management Report H1 2023 FINALDocument102 pagesCPIPG Management Report H1 2023 FINALCarloNo ratings yet

- List of POPs for NPS with Reg No, Name and AddressDocument8 pagesList of POPs for NPS with Reg No, Name and Address98675No ratings yet

- Aia Smart Reward SaverDocument8 pagesAia Smart Reward SaverAhmad NurdinNo ratings yet

- Water BillDocument1 pageWater BillAlex R0% (1)

- Godrej ConsumerDocument7 pagesGodrej ConsumermuralyyNo ratings yet

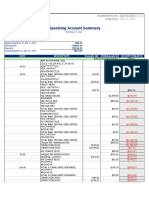

- Statement of Accounts: Today's StatementsDocument1 pageStatement of Accounts: Today's StatementsAnonymous 1oW40srJJ2No ratings yet

- BankUSA Cash Movement Case StudyDocument3 pagesBankUSA Cash Movement Case StudyJairo OjedaNo ratings yet

- Mahmuda MemDocument3 pagesMahmuda MemDurer KashbonNo ratings yet

- Installment Sales Preparartion of Financial StatementDocument2 pagesInstallment Sales Preparartion of Financial StatementRiza Mae AlceNo ratings yet

- Sbi PDFDocument4 pagesSbi PDFAvijit SamantaNo ratings yet

- Risk Based Internal Auditing in BanksDocument55 pagesRisk Based Internal Auditing in BanksAKSHAT RAJESH SHAH100% (1)

- Prime It Bank Statement - July 2019Document4 pagesPrime It Bank Statement - July 2019api-306226330No ratings yet

- Insurance TerminologyDocument46 pagesInsurance TerminologyMiraRai75% (4)