You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Ant Financial: Unpacking The $150B Fintech GiantDocument54 pagesAnt Financial: Unpacking The $150B Fintech GiantHow Xiang NgNo ratings yet

- Statment REV OctDocument4 pagesStatment REV OctSlabu FatoumataNo ratings yet

- Session 9 - Bank CapitalDocument18 pagesSession 9 - Bank CapitalArun KumarNo ratings yet

- Session 12-13 - Basel II - Credit RiskDocument18 pagesSession 12-13 - Basel II - Credit RiskArun KumarNo ratings yet

- Session 5 - 6 Financial Statements of BankDocument15 pagesSession 5 - 6 Financial Statements of BankArun KumarNo ratings yet

- 1-15ilovepdf MergedDocument121 pages1-15ilovepdf MergedArun KumarNo ratings yet

- Session 1 - 4 Banking System & StructureDocument27 pagesSession 1 - 4 Banking System & StructureArun KumarNo ratings yet

- Session 26 - Bank Credit - BasicsDocument8 pagesSession 26 - Bank Credit - BasicsArun KumarNo ratings yet

- Session 21 & 22 (CH 17,18,19 & 20 - RV)Document65 pagesSession 21 & 22 (CH 17,18,19 & 20 - RV)Arun KumarNo ratings yet

- Session 30 - Trade FinanceDocument33 pagesSession 30 - Trade FinanceArun KumarNo ratings yet

- 2 Project RisksDocument28 pages2 Project RisksArun KumarNo ratings yet

- Session 3 & 4 (CH 2 - Approaches To Valuation - DCF & RV)Document44 pagesSession 3 & 4 (CH 2 - Approaches To Valuation - DCF & RV)Arun KumarNo ratings yet

- Level I 2018 2019 Program Changes PDFDocument2 pagesLevel I 2018 2019 Program Changes PDFMuhammad BurairNo ratings yet

- Introduction To Transaction ProcessingDocument6 pagesIntroduction To Transaction ProcessingmafeNo ratings yet

- O Level MCQDocument77 pagesO Level MCQTaimoorNo ratings yet

- Management Accounting ProjectDocument15 pagesManagement Accounting Projecturvigarg079No ratings yet

- HedgeingDocument83 pagesHedgeingfarah_pawestriNo ratings yet

- Status Master Services Agreement - Aria Linea Jet - RocketRoute LTDDocument1 pageStatus Master Services Agreement - Aria Linea Jet - RocketRoute LTDTheodore RoeNo ratings yet

- Inisiasi Tuton Ke-1Document8 pagesInisiasi Tuton Ke-1Pandu SaktiNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

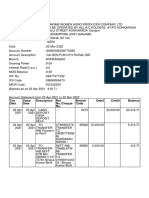

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument16 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceTanu ParidaNo ratings yet

- Measuring and Evaluating The Performance of Banks and Their Principal CompetitorsDocument22 pagesMeasuring and Evaluating The Performance of Banks and Their Principal CompetitorsMarwa HassanNo ratings yet

- WIM Pricing GuideDocument54 pagesWIM Pricing Guidemoveee2No ratings yet

- PT Rumah Kita MebelDocument18 pagesPT Rumah Kita MebelSaia Pandi100% (1)

- Financial Accounting 2 BBA 212 Instructions: 1 Answer One (1) Question Only Q. 1Document4 pagesFinancial Accounting 2 BBA 212 Instructions: 1 Answer One (1) Question Only Q. 1Mwilah Joshua ChalobaNo ratings yet

- Tha Ifsca Banking Handbook Gen Directions Version 212112021075913Document54 pagesTha Ifsca Banking Handbook Gen Directions Version 212112021075913Rishab GoelNo ratings yet

- Salale UniversityDocument10 pagesSalale UniversityRegasa GutemaNo ratings yet

- Blackbook ProjectDocument42 pagesBlackbook ProjectTasbi KhanNo ratings yet

- Accounting HistoryDocument23 pagesAccounting HistoryMotion ChipondaNo ratings yet

- CRM - Icici BankDocument45 pagesCRM - Icici BankRadhika ChadhaNo ratings yet

- Principles of Auditing MCQ Questions and Answers Part - 3Document12 pagesPrinciples of Auditing MCQ Questions and Answers Part - 3Umar ZamarNo ratings yet

- 1 - PDFsam - Hitungan Cicilan Leasing Avanza Mandiri Tunas FinanceDocument6 pages1 - PDFsam - Hitungan Cicilan Leasing Avanza Mandiri Tunas Financeanon_177763922No ratings yet

- Ensayo 2 Ingles Nif B 15Document5 pagesEnsayo 2 Ingles Nif B 15Yalmer GómezNo ratings yet

- DC3 UnlockedDocument5 pagesDC3 UnlockedRajesh Kumar SinghNo ratings yet

- SB-1605 April-1Document11 pagesSB-1605 April-1Pankaj PandeyNo ratings yet

- Swati GargDocument3 pagesSwati GargThe Cultural CommitteeNo ratings yet

- Internationalization of Financial MarketsDocument2 pagesInternationalization of Financial MarketsJannaviel MirandillaNo ratings yet

- Intercorporate Acquisitions and Investment in Other EntitiesDocument21 pagesIntercorporate Acquisitions and Investment in Other Entitieswahyu dirosoNo ratings yet

- An Overview of Financial SystemDocument4 pagesAn Overview of Financial SystemYee Sin MeiNo ratings yet

- CFI Accounting Fundementals Jenga Inc ExerciseDocument3 pagesCFI Accounting Fundementals Jenga Inc ExercisesovalaxNo ratings yet