You might also like

- Civics Full Study GuideDocument21 pagesCivics Full Study Guideapi-293218730No ratings yet

- Arkansas Tax Titles RevisitedDocument23 pagesArkansas Tax Titles RevisitedTina BillingsleyNo ratings yet

- Section-By-Section Coronavirus Tax Relief MeasuresDocument4 pagesSection-By-Section Coronavirus Tax Relief MeasuresFox News80% (5)

- US Vs DorrDocument7 pagesUS Vs DorrMary Christine Cesara DaepNo ratings yet

- Corporate Recovery and Tax Incentives For EnterprisesDocument5 pagesCorporate Recovery and Tax Incentives For EnterprisesIvy BoseNo ratings yet

- Frequently Ask Question - BudgetingDocument28 pagesFrequently Ask Question - BudgetingNrf Frn100% (1)

- Philconsa v. EnriquezDocument4 pagesPhilconsa v. EnriquezIldefonso HernaezNo ratings yet

- In Re CunananDocument7 pagesIn Re CunananRmLyn MclnaoNo ratings yet

- Dahl - 1957 - The Concept of PowerDocument15 pagesDahl - 1957 - The Concept of Powermiki7555No ratings yet

- 2000constitution TGPDocument13 pages2000constitution TGPVincent Tan100% (6)

- Poli Law Digests Compiled 2012-2015 by Dean Candelaria PDFDocument34 pagesPoli Law Digests Compiled 2012-2015 by Dean Candelaria PDFdemosrea100% (1)

- Everything You Need To Know About CREATE Act in The PhilippinesDocument4 pagesEverything You Need To Know About CREATE Act in The PhilippinesMaricrisNo ratings yet

- Ordinances V ResolutionsDocument4 pagesOrdinances V ResolutionsLoven Jake Masias100% (1)

- The 1987 Constitution of The Republic of The PhilippinesDocument12 pagesThe 1987 Constitution of The Republic of The PhilippinesJerica MercadoNo ratings yet

- Statcon - Atty Guji Notes 2Document59 pagesStatcon - Atty Guji Notes 2KaiNo ratings yet

- Philippine Constitution Association vs. Enriquez GR No 113105Document3 pagesPhilippine Constitution Association vs. Enriquez GR No 113105Lizzie GeraldinoNo ratings yet

- Statutory Construction Notes - KKK - 1Document10 pagesStatutory Construction Notes - KKK - 1CJNo ratings yet

- PWC News Alert 30 September 2020 Taxation and Other Laws Relaxation and Amendment of Certain Provisions Act 2020 NotifiedDocument9 pagesPWC News Alert 30 September 2020 Taxation and Other Laws Relaxation and Amendment of Certain Provisions Act 2020 Notifiedsujit guptaNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022Document24 pagesProposed Tax Changes Under The Finance Bill 2022 ALN Kenya Legal Alert April 2022yomak94018No ratings yet

- Finance Act 2021 Major HighlightsDocument6 pagesFinance Act 2021 Major HighlightsAyodeji BabatundeNo ratings yet

- Samilcommentary Dec2023 enDocument10 pagesSamilcommentary Dec2023 enhekele9111No ratings yet

- AFF's Memorandum On Federal & Provincial Finance Acts, 2022Document61 pagesAFF's Memorandum On Federal & Provincial Finance Acts, 2022ABODE PVT LIMITEDNo ratings yet

- Decoding Indian Union BudgetDocument6 pagesDecoding Indian Union BudgetkumarNo ratings yet

- Nigeria - Highlights of Finance Act 2021 - EY - GlobalDocument16 pagesNigeria - Highlights of Finance Act 2021 - EY - GlobalAyodeji BabatundeNo ratings yet

- Do You Know GST - August 2021Document11 pagesDo You Know GST - August 2021CA Ranjan MehtaNo ratings yet

- Taxjournal July 2020Document60 pagesTaxjournal July 2020Venkatesh PrabhuNo ratings yet

- Decoding Indian Union Budget Finance Bil PDFDocument7 pagesDecoding Indian Union Budget Finance Bil PDFkumarNo ratings yet

- Create Bill 1Document2 pagesCreate Bill 1Nurse NotesNo ratings yet

- Create Law: 10 Most Asked QuestionsDocument2 pagesCreate Law: 10 Most Asked QuestionsEldren CelloNo ratings yet

- Submission To Senate Inquiry Govt Amendments TLAB Multinational TaxDocument8 pagesSubmission To Senate Inquiry Govt Amendments TLAB Multinational Taxandrew.kezzaNo ratings yet

- RR No. 34-2020 v2Document3 pagesRR No. 34-2020 v2JejomarNo ratings yet

- Write-Up CITIRA BillDocument3 pagesWrite-Up CITIRA BillMaeJoNo ratings yet

- Tax Alert No. 91 (Senate Bill (SB) No. 1357 or The Corporate Recovery and Tax Incentives For Enterprises Act (CREATE) )Document9 pagesTax Alert No. 91 (Senate Bill (SB) No. 1357 or The Corporate Recovery and Tax Incentives For Enterprises Act (CREATE) )Karina PulidoNo ratings yet

- Topic: Prospectus and Doctrine Of: Disclosure-Regulations Vs Self Regulations: A Critical StudyDocument18 pagesTopic: Prospectus and Doctrine Of: Disclosure-Regulations Vs Self Regulations: A Critical StudyAnusha Rao ThotaNo ratings yet

- Analysis of 10 Important Changes in GST From 1st October 2022 - Taxguru - in PDFDocument4 pagesAnalysis of 10 Important Changes in GST From 1st October 2022 - Taxguru - in PDFPawan AswaniNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- House Bill 4001Document7 pagesHouse Bill 4001Elizabeth WashingtonNo ratings yet

- RMO No. 42-2020Document2 pagesRMO No. 42-2020Miming BudoyNo ratings yet

- Corporate Recovery and Tax Incentives For Enterprises (Create) BillDocument15 pagesCorporate Recovery and Tax Incentives For Enterprises (Create) BillRonn Robby RosalesNo ratings yet

- Tax Brief - June 2012Document8 pagesTax Brief - June 2012Rheneir MoraNo ratings yet

- Create Law SummaryDocument2 pagesCreate Law SummaryJiza GarciaNo ratings yet

- Grant Thornton Alert - The Finance Bill 2020Document10 pagesGrant Thornton Alert - The Finance Bill 2020elinzolaNo ratings yet

- Tax AmendmentsDocument5 pagesTax AmendmentsLipi ThapliyalNo ratings yet

- Corporate Recovery Tax Incentives Enterprises Act: AND FORDocument2 pagesCorporate Recovery Tax Incentives Enterprises Act: AND FORAl-jbr Tub SarNo ratings yet

- TDS in GSTDocument3 pagesTDS in GSTacm001No ratings yet

- TNF Korea Tax Reform Aug10 2023Document7 pagesTNF Korea Tax Reform Aug10 2023crazymoneyNo ratings yet

- CREATE Law - 10 Most Asked QuestionsDocument4 pagesCREATE Law - 10 Most Asked QuestionscarloNo ratings yet

- Create BillDocument31 pagesCreate BillJanet PaglingayenNo ratings yet

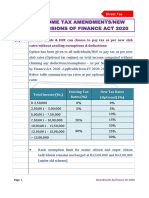

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Ra 11534 - Corporate Recovery & Tax Incentives For Enterprises Act (Create)Document11 pagesRa 11534 - Corporate Recovery & Tax Incentives For Enterprises Act (Create)Rolly Balagon Caballero100% (1)

- Research On CREATE LawDocument7 pagesResearch On CREATE LawalbycadavisNo ratings yet

- UntitledDocument2 pagesUntitledYamier Hakam DammangNo ratings yet

- Deloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedDocument4 pagesDeloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedSunil GidwaniNo ratings yet

- Amity Global Business School, PuneDocument15 pagesAmity Global Business School, PuneChand KalraNo ratings yet

- Category Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxDocument16 pagesCategory Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxshwetakuppanNo ratings yet

- Uae Corporate Tax Law SummaryDocument37 pagesUae Corporate Tax Law SummarypankajNo ratings yet

- AFF Tax Memorandum v5Document28 pagesAFF Tax Memorandum v5Azhar AliNo ratings yet

- Delloite CIT (A) PDFDocument7 pagesDelloite CIT (A) PDFshashi vermaNo ratings yet

- YYC July NewsletterDocument11 pagesYYC July NewsletterCatherine ChuaNo ratings yet

- Pa Tax Brief - February 2020Document12 pagesPa Tax Brief - February 2020Teresita TibayanNo ratings yet

- Bars On Initiation of CIRPDocument4 pagesBars On Initiation of CIRPAtulya Singh ChauhanNo ratings yet

- Federal Budget 2020-21Document7 pagesFederal Budget 2020-21yiang.tranNo ratings yet

- KPMG-Technical Update May 22 enDocument3 pagesKPMG-Technical Update May 22 enbryanmark2512No ratings yet

- Revenue Regulations No. 34-2020Document3 pagesRevenue Regulations No. 34-2020zelayneNo ratings yet

- Tax Alert (April 2020) FinalDocument30 pagesTax Alert (April 2020) FinalRheneir MoraNo ratings yet

- Ce TaxDocument65 pagesCe Taxryl100% (1)

- Direct Taxes Code 2010Document14 pagesDirect Taxes Code 2010musti_shahNo ratings yet

- CREATE Bill Salient PointsDocument2 pagesCREATE Bill Salient PointsMats Lucero100% (1)

- CREATE Salient ProvisionsDocument3 pagesCREATE Salient ProvisionsAldrin Santos AntonioNo ratings yet

- Briefing On The Corporate Recovery and Tax Incentives For Enterprise (CREATE) ActDocument56 pagesBriefing On The Corporate Recovery and Tax Incentives For Enterprise (CREATE) ActEdward GanNo ratings yet

- Budget 2022 - Comprehensive Guide On Personal Finance-17Document15 pagesBudget 2022 - Comprehensive Guide On Personal Finance-17Shubham ShawNo ratings yet

- Task 8Document23 pagesTask 8Anooja SajeevNo ratings yet

- Bond Tax Exemption Nigeria July 2012Document3 pagesBond Tax Exemption Nigeria July 2012Mark allenNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Executive Orders and Presidential PowersDocument23 pagesExecutive Orders and Presidential Powersshanayub496No ratings yet

- Labour Code's New Contours Revealed: Orbán Visits SlovakiaDocument12 pagesLabour Code's New Contours Revealed: Orbán Visits SlovakiaThe Slovak SpectatorNo ratings yet

- Statutory Construction - Module 1.2 - Law-Making ProcessDocument30 pagesStatutory Construction - Module 1.2 - Law-Making ProcessHenrick YsonNo ratings yet

- Statutory Construction by Agpalo Book 2003Document88 pagesStatutory Construction by Agpalo Book 2003Vir Stella MarianitoNo ratings yet

- Prime Minister or President: Are Some Ways Better Than Others?Document10 pagesPrime Minister or President: Are Some Ways Better Than Others?Alexa Joy C. InguilloNo ratings yet

- US UK Culture - Summary SheetDocument30 pagesUS UK Culture - Summary SheetK57 TRAN THI MINH NGOCNo ratings yet

- Role of President in Indian Legal System?: Continue .Document2 pagesRole of President in Indian Legal System?: Continue .Rvi MahayNo ratings yet

- Comparitive Uk & UsaDocument13 pagesComparitive Uk & UsaEliim RehmanNo ratings yet

- Narang A.S., India Political System, Process and Development, Gitanjali Publishing House, New Delhi, 2015, P. 672 - 674Document26 pagesNarang A.S., India Political System, Process and Development, Gitanjali Publishing House, New Delhi, 2015, P. 672 - 674saif aliNo ratings yet

- Statcon - Week2 Readings 2Document142 pagesStatcon - Week2 Readings 2Kê MilanNo ratings yet

- Chapter-1 Civics and Government 1 To 25Document11 pagesChapter-1 Civics and Government 1 To 25inzali naylaNo ratings yet

- Macababad Evidence NotesDocument5 pagesMacababad Evidence Notesvendetta scrubNo ratings yet

- Branches of The Philippine Government: Separation of PowersDocument3 pagesBranches of The Philippine Government: Separation of PowersAl-zobair MacarayaNo ratings yet

- Prelim FinalDocument18 pagesPrelim FinalCaren PacomiosNo ratings yet

- Legislative: I. Evolution of The Philippine Legislative SystemDocument5 pagesLegislative: I. Evolution of The Philippine Legislative SystemMargaret La RosaNo ratings yet

- Pos 4 FinDocument18 pagesPos 4 FinNandan GowdaNo ratings yet