You might also like

- DocxDocument5 pagesDocxLorraine Mae Robrido100% (2)

- Introduction to Managerial Accounting Cost ConceptsDocument85 pagesIntroduction to Managerial Accounting Cost Conceptsحسين عبدالرحمن100% (1)

- File: Chapter 05 - Consolidated Financial Statements - Intra-Entity Asset Transactions Multiple ChoiceDocument53 pagesFile: Chapter 05 - Consolidated Financial Statements - Intra-Entity Asset Transactions Multiple Choicejana ayoubNo ratings yet

- Managerial Accounting and Cost ConceptsDocument67 pagesManagerial Accounting and Cost ConceptsTristan AdrianNo ratings yet

- Session 9 Introduction To Management AccountingDocument52 pagesSession 9 Introduction To Management Accounting靳雪娇No ratings yet

- Managerial Accounting: Learning ObjectivesDocument52 pagesManagerial Accounting: Learning ObjectivesRandy SuryajayaNo ratings yet

- Weygandt, Kieso, & Kimmel: Managerial AccountingDocument56 pagesWeygandt, Kieso, & Kimmel: Managerial AccountingJerome MogaNo ratings yet

- MA Week 1Document61 pagesMA Week 1Lam BiNo ratings yet

- Intro To Management AcctgDocument46 pagesIntro To Management AcctgpotatookunNo ratings yet

- Managerial Accounting InsightsDocument4 pagesManagerial Accounting InsightsAbd MuizNo ratings yet

- Module 1-Intro To Management AccountingDocument48 pagesModule 1-Intro To Management AccountingAna ValenovaNo ratings yet

- CH 01Document34 pagesCH 01Bena JagonobNo ratings yet

- Managerial Accounting, 13 Edition, Garrison/ Noreen/ BrewerDocument25 pagesManagerial Accounting, 13 Edition, Garrison/ Noreen/ BrewerAhsan Sayeed Nabeel Depro100% (1)

- Chapter 14Document55 pagesChapter 14giannimizrahi5No ratings yet

- ACCO 20113 Week 2 Strategic Cost MGT and Cost ConceptsDocument85 pagesACCO 20113 Week 2 Strategic Cost MGT and Cost ConceptsBhosx KimNo ratings yet

- GS 202 Managerial Accounting - Basics: By: Allan F. Galvez, PH.DDocument27 pagesGS 202 Managerial Accounting - Basics: By: Allan F. Galvez, PH.DJayson TasarraNo ratings yet

- Cost Accounting FundamentalsDocument56 pagesCost Accounting FundamentalsAbdillahi Ibrahim Sh NorNo ratings yet

- Managerial Accounting OverviewDocument34 pagesManagerial Accounting OverviewGeorgie SarmientoNo ratings yet

- Managerial Accounting. Lecture 1Document33 pagesManagerial Accounting. Lecture 1Aman UllahNo ratings yet

- Managerial AccountingDocument34 pagesManagerial AccountingCesar CabreraNo ratings yet

- C1 IntroDocument13 pagesC1 IntroNgọc Phương HoàngNo ratings yet

- MGT Acc. & Cost ConceptsDocument24 pagesMGT Acc. & Cost ConceptsJonathan JibuNo ratings yet

- Introduction To Management AccountingDocument23 pagesIntroduction To Management AccountingGaluh Boga Kuswara100% (1)

- Managerial Accounting and Cost Concepts: Mcgraw Hill/IrwinDocument29 pagesManagerial Accounting and Cost Concepts: Mcgraw Hill/IrwinMuhammad Zia KhanNo ratings yet

- Chapter 1Document13 pagesChapter 1Hoài Thu NguyễnNo ratings yet

- Managerial Accounting and the Business Environment Chapter One SummaryDocument23 pagesManagerial Accounting and the Business Environment Chapter One SummarysanosyNo ratings yet

- Management Accounting: An OverviewDocument12 pagesManagement Accounting: An Overviewahmed arfanNo ratings yet

- CH 01 Cost of ManaufacturedDocument68 pagesCH 01 Cost of ManaufacturedAshfaq AhmedNo ratings yet

- Module-1-ACCO-018Document26 pagesModule-1-ACCO-018easiroy23No ratings yet

- BudgetingDocument5 pagesBudgetingishhNo ratings yet

- Session - 1: Introduction: PGP 2022-24 Prof. M. Shameem JawedDocument39 pagesSession - 1: Introduction: PGP 2022-24 Prof. M. Shameem JawedAnkitShettyNo ratings yet

- Managerial Accounting Code: 0502603Document13 pagesManagerial Accounting Code: 0502603nanaNo ratings yet

- IffatZehra - 2972 - 15876 - 1 - Chap 1Document51 pagesIffatZehra - 2972 - 15876 - 1 - Chap 1Sabeeh Mustafa ZubairiNo ratings yet

- Managerial Accounting and Cost Concepts: Mcgraw-Hill/IrwinDocument24 pagesManagerial Accounting and Cost Concepts: Mcgraw-Hill/IrwinYasmine MagdiNo ratings yet

- Lecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesLecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro Davaoace ender zeroNo ratings yet

- Session 6.1 Lecture Ch14 Managerial AccountingDocument31 pagesSession 6.1 Lecture Ch14 Managerial AccountingPhan Tuan ThuanNo ratings yet

- Chapter 01 - Managerial Accounting and Business EnvironmentDocument27 pagesChapter 01 - Managerial Accounting and Business EnvironmentVy Trần Lê ThảoNo ratings yet

- Chapter 1 - IntroductionDocument2 pagesChapter 1 - IntroductionJane ValenciaNo ratings yet

- PowerDocument66 pagesPoweralmamaefranco9No ratings yet

- Chapter 1 - Management AccountingDocument22 pagesChapter 1 - Management AccountingjerlyNo ratings yet

- Strategic Cost MGT and Cost ConceptsDocument99 pagesStrategic Cost MGT and Cost ConceptsKendall JennerNo ratings yet

- Managerial Accounting: Tool For Business Decision Making Third EditionDocument56 pagesManagerial Accounting: Tool For Business Decision Making Third Editionএ.বি.এস. আশিকNo ratings yet

- Overview of MASDocument6 pagesOverview of MASDonna AmbaganNo ratings yet

- CH 11Document55 pagesCH 11Bhavin purohitNo ratings yet

- Since 1977 Management Advisory ServicesDocument6 pagesSince 1977 Management Advisory ServicesdaemonspadechocoyNo ratings yet

- Management Accounting Roles and FunctionsDocument7 pagesManagement Accounting Roles and FunctionsANTONIA LORENA BITUINNo ratings yet

- Cost Classifications and Income StatementDocument50 pagesCost Classifications and Income StatementGovinda Gde Phillips39No ratings yet

- Wey AP 14e PPT Ch19 Managerial-AccountingDocument45 pagesWey AP 14e PPT Ch19 Managerial-Accountinghanhuyen0311No ratings yet

- L5257 - 1 Introduction 2017Document46 pagesL5257 - 1 Introduction 2017Reza Nursyah PutraNo ratings yet

- Introduction To Management AccountingDocument47 pagesIntroduction To Management AccountingMULATNo ratings yet

- MAS-01 Management Accounting ConceptsDocument6 pagesMAS-01 Management Accounting ConceptsJohn Aries ReyesNo ratings yet

- Management Advisory Services RoleDocument15 pagesManagement Advisory Services RoleJAY AUBREY PINEDANo ratings yet

- ControllingDocument54 pagesControllingFügedy TamásNo ratings yet

- Chapter 1, (Garrison Text) Summary:: AccountingDocument4 pagesChapter 1, (Garrison Text) Summary:: AccountingAhmadYaseenNo ratings yet

- Full Download Managerial Accounting For Managers 2nd Edition Noreen Solutions ManualDocument35 pagesFull Download Managerial Accounting For Managers 2nd Edition Noreen Solutions Manuallinderleafeulah100% (33)

- Ontrolling: Source: Management - A Global Perspective by Weihrich and Koontz 11 EditionDocument19 pagesOntrolling: Source: Management - A Global Perspective by Weihrich and Koontz 11 EditionKyle SaylonNo ratings yet

- Shukrullah Assignment No 2Document4 pagesShukrullah Assignment No 2Shukrullah JanNo ratings yet

- ch01 CostAccDocument18 pagesch01 CostAccqueneemaeaustriaNo ratings yet

- Principles of Cost AccountingDocument37 pagesPrinciples of Cost AccountingAhmed hassanNo ratings yet

- Introduction To MADocument32 pagesIntroduction To MAnusratNo ratings yet

- Lecture 3Document31 pagesLecture 3PiyushNo ratings yet

- Nền kinh tế của các quốc gia và toàn cầu trong nhữ.vi.enDocument4 pagesNền kinh tế của các quốc gia và toàn cầu trong nhữ.vi.enBradNo ratings yet

- Stress ManagementDocument13 pagesStress ManagementBradNo ratings yet

- Strategic ManagmentDocument11 pagesStrategic ManagmentBradNo ratings yet

- Ex-3 6Document1 pageEx-3 6BradNo ratings yet

- Guidelines On Writing A Research Proposal - Ebba - 0Document4 pagesGuidelines On Writing A Research Proposal - Ebba - 0BradNo ratings yet

- Contents of A Good Research Proposal v1.0Document2 pagesContents of A Good Research Proposal v1.0Bright Williams BoakyeNo ratings yet

- Corporate Finace 1 PDFDocument4 pagesCorporate Finace 1 PDFwafflesNo ratings yet

- Rogers' Chocolates SWOT and Competitor AnalysisDocument29 pagesRogers' Chocolates SWOT and Competitor AnalysisthreeinvestigatorsNo ratings yet

- Statement of Cash Flows - CRDocument24 pagesStatement of Cash Flows - CRMzingaye100% (1)

- SEC Form 20-Is Definitive - 2015 - 0Document263 pagesSEC Form 20-Is Definitive - 2015 - 0Aeron Paul AntonioNo ratings yet

- Chapter 21: The Simplest Short-Run Macro Model: Desired Aggregate ExpenditureDocument8 pagesChapter 21: The Simplest Short-Run Macro Model: Desired Aggregate ExpenditureSaaki GaneshNo ratings yet

- Cost Dynamics - Elements and ClassificationDocument4 pagesCost Dynamics - Elements and ClassificationBrian OmbatiNo ratings yet

- Summer Training Project Report Derivatives in The Stock MarketDocument42 pagesSummer Training Project Report Derivatives in The Stock Marketprashant purohitNo ratings yet

- O.P.C.F 16 Suspension of CoverageDocument1 pageO.P.C.F 16 Suspension of CoverageGarry sharmaNo ratings yet

- EFA AssignmentDocument5 pagesEFA AssignmentDeviNo ratings yet

- EuroHedge Summit Brochure - April 2011Document12 pagesEuroHedge Summit Brochure - April 2011Absolute ReturnNo ratings yet

- Groupon2 3Document3 pagesGroupon2 328kpjrrx4nNo ratings yet

- Underwriting SOPDocument5 pagesUnderwriting SOPChris JacksonNo ratings yet

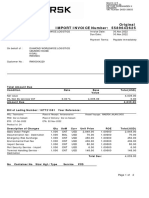

- Original IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)Document2 pagesOriginal IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)AllyNo ratings yet

- Final Judgment For Defendants v. Wells Fargo Bank, N.A., in A Residential Mortgage Foreclosure Case After Trial Held in Hernando County, Florida, Before Judge Angel On Feb. 14, 2013.Document11 pagesFinal Judgment For Defendants v. Wells Fargo Bank, N.A., in A Residential Mortgage Foreclosure Case After Trial Held in Hernando County, Florida, Before Judge Angel On Feb. 14, 2013.Chuck Kalogianis100% (1)

- Arvind Mills AnalysisDocument18 pagesArvind Mills AnalysisAnup AgarwalNo ratings yet

- Basics of Negotiable InstrumentsDocument46 pagesBasics of Negotiable Instrumentsgox350% (2)

- Banking TSN 2018 2nd ExamDocument54 pagesBanking TSN 2018 2nd ExamAngel DeiparineNo ratings yet

- Cash Pooling in Today's WorldDocument10 pagesCash Pooling in Today's Worldoramirezb2No ratings yet

- Cooper 2015 - Shadow Money and The Shadow WorkforceDocument30 pagesCooper 2015 - Shadow Money and The Shadow Workforceanton.de.rotaNo ratings yet

- Customer Satisfaction towards RTGS & NEFTDocument70 pagesCustomer Satisfaction towards RTGS & NEFTRajibKumar100% (1)

- ECBC Brochurea4 Munich23 V7webDocument44 pagesECBC Brochurea4 Munich23 V7webVasilisNo ratings yet

- Summer Moon Presentation December 13,2004Document25 pagesSummer Moon Presentation December 13,2004Essam Al BakryNo ratings yet

- Oct 2022 Unit 2 QPDocument32 pagesOct 2022 Unit 2 QPKarama OmarNo ratings yet

- VanShop rental (1 year)Total:39,300Document51 pagesVanShop rental (1 year)Total:39,300Abdullah Muhammad0% (1)

- Homework Chapter 4Document4 pagesHomework Chapter 4Thu Giang TranNo ratings yet

- ICICI Pru Smart Life BrochureDocument23 pagesICICI Pru Smart Life Brochuresrinivas reddyNo ratings yet

- Acctg 207B Final ExamDocument5 pagesAcctg 207B Final ExamJERROLD EIRVIN PAYOPAYNo ratings yet