You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- BOQ English VersionDocument15 pagesBOQ English VersionEzequiel Dos SantosNo ratings yet

- Earthing MisconceptionsDocument2 pagesEarthing MisconceptionsAnkush SinghNo ratings yet

- 02 - ValvesDocument25 pages02 - ValvesRio Indoknivezia100% (1)

- Tecnip Umbilical Systems PDFDocument20 pagesTecnip Umbilical Systems PDFAndré ParavidinoNo ratings yet

- Kalimantan Coal Railway Project PDFDocument23 pagesKalimantan Coal Railway Project PDFpuput utomoNo ratings yet

- Delta Tertiary WindingDocument1 pageDelta Tertiary WindingwilliamnuevoNo ratings yet

- Bills ConversionsDocument20 pagesBills ConversionssudhirbmaliNo ratings yet

- Cold IroningDocument139 pagesCold IroningkonstadineNo ratings yet

- Madiha Assignment 07Document28 pagesMadiha Assignment 07Usman MahmoodNo ratings yet

- Living in A World With Low Crude Oil Prices, An El Niño and Biodiesel SubsidiesDocument32 pagesLiving in A World With Low Crude Oil Prices, An El Niño and Biodiesel SubsidiesUsman MahmoodNo ratings yet

- Panel 3 - 0 MR ChandranDocument7 pagesPanel 3 - 0 MR ChandranUsman MahmoodNo ratings yet

- Plenary 2 - 5 Dorab MistryDocument11 pagesPlenary 2 - 5 Dorab MistryUsman MahmoodNo ratings yet

- Plenary 2 - 2 Emily FrenchDocument11 pagesPlenary 2 - 2 Emily FrenchUsman MahmoodNo ratings yet

- 1 Abdul Rasheed JanmohammadDocument20 pages1 Abdul Rasheed JanmohammadUsman MahmoodNo ratings yet

- S# Vessels Names Berthed Disport Loadport Product Seller QuantityDocument7 pagesS# Vessels Names Berthed Disport Loadport Product Seller QuantityUsman MahmoodNo ratings yet

- SR. # Vessel Name Berth Date Load Port Discharge Port Product Name Seller Name QuantityDocument6 pagesSR. # Vessel Name Berth Date Load Port Discharge Port Product Name Seller Name QuantityUsman MahmoodNo ratings yet

- Outlook For World Vegoils 2016 2016: by Dorab E Mistry Godrej International LimitedDocument17 pagesOutlook For World Vegoils 2016 2016: by Dorab E Mistry Godrej International LimitedUsman MahmoodNo ratings yet

- Announcement TR 62d51088 7b5bDocument2 pagesAnnouncement TR 62d51088 7b5bUsman MahmoodNo ratings yet

- Edible Oil Import Feb-2020Document5 pagesEdible Oil Import Feb-2020Usman MahmoodNo ratings yet

- Compliance Contract TemplateDocument1 pageCompliance Contract TemplateUsman MahmoodNo ratings yet

- S# Vessel Name Disport Berthed Loadport Product Seller QuantityDocument4 pagesS# Vessel Name Disport Berthed Loadport Product Seller QuantityUsman MahmoodNo ratings yet

- S# Vessel Names Disport Berthed Loadport Product Sellers QuantityDocument5 pagesS# Vessel Names Disport Berthed Loadport Product Sellers QuantityUsman MahmoodNo ratings yet

- S# Vessel Names Disport Berthed On Loadport Products Seller QuantityDocument5 pagesS# Vessel Names Disport Berthed On Loadport Products Seller QuantityUsman MahmoodNo ratings yet

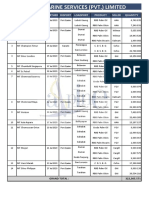

- Alpine Marine Services (PVT.) Limited: SR. # Vessel Name Berth Date Load Port Discharge Port Product Name Seller NameDocument12 pagesAlpine Marine Services (PVT.) Limited: SR. # Vessel Name Berth Date Load Port Discharge Port Product Name Seller NameUsman MahmoodNo ratings yet

- S# Vessels Names Berthed Disport Loadport Product Seller QuantityDocument6 pagesS# Vessels Names Berthed Disport Loadport Product Seller QuantityUsman MahmoodNo ratings yet

- Toyota Yaris Atic CVT 1.5Document1 pageToyota Yaris Atic CVT 1.5Usman MahmoodNo ratings yet

- Saima Paari Avenue PDFDocument9 pagesSaima Paari Avenue PDFUsman MahmoodNo ratings yet

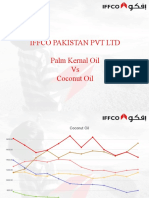

- Iffco Pakistan PVT LTD Palm Kernal Oil Vs Coconut OilDocument3 pagesIffco Pakistan PVT LTD Palm Kernal Oil Vs Coconut OilUsman MahmoodNo ratings yet

- Crude Oil DataDocument2 pagesCrude Oil DataUsman MahmoodNo ratings yet

- Alpine Marine Services (PVT.) LimitedDocument6 pagesAlpine Marine Services (PVT.) LimitedUsman MahmoodNo ratings yet

- Binga: Her Father Was Heavily Addicted To DrugsDocument97 pagesBinga: Her Father Was Heavily Addicted To DrugsRaffaNo ratings yet

- Unit 8: Environmental Studies: Q2e Listening & Speaking 5: Audio ScriptDocument7 pagesUnit 8: Environmental Studies: Q2e Listening & Speaking 5: Audio ScriptLay LylyNo ratings yet

- 01 ElevatorComponents en Interaktiv-09-2017Document113 pages01 ElevatorComponents en Interaktiv-09-2017Sanjeeb Sinha100% (1)

- Jis B 0100 - 2013Document94 pagesJis B 0100 - 2013igormetaldata100% (1)

- RBI Qualitative Damage Assessment As A Part of The RBI (Risk-Based Inspection) Proc ManuscriptJovanovic - V07aj29092014Document22 pagesRBI Qualitative Damage Assessment As A Part of The RBI (Risk-Based Inspection) Proc ManuscriptJovanovic - V07aj29092014rudi setiawanNo ratings yet

- Completion Practices in Deep Sour Tuscaloosa Wells: SPE, Amoco Production CoDocument10 pagesCompletion Practices in Deep Sour Tuscaloosa Wells: SPE, Amoco Production CoAnonymous VNu3ODGavNo ratings yet

- PC F25a 04 1Document69 pagesPC F25a 04 1John PapasNo ratings yet

- O & IO-540 Oper Manual 60297-10Document114 pagesO & IO-540 Oper Manual 60297-10Waqar AhmedNo ratings yet

- Experiment-No 1Document2 pagesExperiment-No 1Sandra GonzalesNo ratings yet

- 262 Crawler Hydr DiagramsDocument2 pages262 Crawler Hydr DiagramsPavel SokolovNo ratings yet

- Rotary Positive Displacement PumpsDocument16 pagesRotary Positive Displacement Pumpsalexmuchmure2158No ratings yet

- Final Lab ReportDocument10 pagesFinal Lab ReportEric PerkeyNo ratings yet

- AE 231 Thermodynamics Week 3 Week 3: Instructor: Assoc. Prof. Dr. Sinan EyiDocument47 pagesAE 231 Thermodynamics Week 3 Week 3: Instructor: Assoc. Prof. Dr. Sinan EyiOnur ÖZÇELİKNo ratings yet

- Corporate Presentation - LJHCDocument16 pagesCorporate Presentation - LJHCJulianNo ratings yet

- Product Manual 36703 (Revision NEW) : Pgev and Pge Locomotive GovernorsDocument132 pagesProduct Manual 36703 (Revision NEW) : Pgev and Pge Locomotive GovernorsElaine Cristina OliveiraNo ratings yet

- Altablue TT: 10-Liter Melters With Dual Stream PumpsDocument2 pagesAltablue TT: 10-Liter Melters With Dual Stream PumpsFlávio dos Santos Ferreira JuniorNo ratings yet

- Is 13694Document11 pagesIs 13694Yashu HandaNo ratings yet

- Paper 2 June 2007 PhysicsDocument16 pagesPaper 2 June 2007 PhysicssolarixeNo ratings yet

- (1 - CV) Model Predictive Control Method For Modular Multilevel Converter ApplicationsDocument7 pages(1 - CV) Model Predictive Control Method For Modular Multilevel Converter ApplicationsNam Hoang ThanhNo ratings yet

- York SB0005Document16 pagesYork SB0005DNo ratings yet

- Project Tundra A Step in The Wrong Direction September 2020Document34 pagesProject Tundra A Step in The Wrong Direction September 2020inforumdocsNo ratings yet

- Manual de Revelador HM-X-AFPDocument28 pagesManual de Revelador HM-X-AFPGustavo Huamán Mallma100% (1)