You might also like

- Oil & Gas Firm Earnings Rise Despite CovidDocument5 pagesOil & Gas Firm Earnings Rise Despite CovidBrian StanleyNo ratings yet

- 21 02 08 DP More Margin More Upside Buy TP 38 From 32Document24 pages21 02 08 DP More Margin More Upside Buy TP 38 From 32tarun606No ratings yet

- MISC Berhad Outperform : Weaker Core Earnings in 1QFY21Document5 pagesMISC Berhad Outperform : Weaker Core Earnings in 1QFY21Iqbal YusufNo ratings yet

- Ramco Cement Q2FY24 ResultsDocument8 pagesRamco Cement Q2FY24 ResultseknathNo ratings yet

- Kgi PTT 239026Document11 pagesKgi PTT 239026dtNo ratings yet

- PPB Group: 2019: Good Results Amid Challenging EnvironmentDocument4 pagesPPB Group: 2019: Good Results Amid Challenging EnvironmentZhi Ming CheahNo ratings yet

- Stalwart of Bio-Economy Revolution!Document22 pagesStalwart of Bio-Economy Revolution!nitinmuthaNo ratings yet

- Petronet Motilal OswalDocument8 pagesPetronet Motilal OswaljoeNo ratings yet

- Coal India (COAL IN) : Q4FY19 Result UpdateDocument6 pagesCoal India (COAL IN) : Q4FY19 Result Updatesaran21No ratings yet

- Vinati Organics LTD: Expansions and New Project To Drive Earnings GrowthDocument6 pagesVinati Organics LTD: Expansions and New Project To Drive Earnings GrowthBhaveek OstwalNo ratings yet

- Australian Securities Exchange Notice: Half Year Results To 30 June 2020Document4 pagesAustralian Securities Exchange Notice: Half Year Results To 30 June 2020TimBarrowsNo ratings yet

- DEME Press Release FY 2022 enDocument16 pagesDEME Press Release FY 2022 enKevin ParkerNo ratings yet

- 1Q21 Net Income Above Expectation: Semirara Mining CorporationDocument8 pages1Q21 Net Income Above Expectation: Semirara Mining CorporationJajahinaNo ratings yet

- Ultratech Cement Limited: Outlook Remains ChallengingDocument5 pagesUltratech Cement Limited: Outlook Remains ChallengingamitNo ratings yet

- Voltas Dolat 140519 PDFDocument7 pagesVoltas Dolat 140519 PDFADNo ratings yet

- Accumulate: Growth Momentum Continues!Document7 pagesAccumulate: Growth Momentum Continues!sj singhNo ratings yet

- Dilip Buildcon: Strong ComebackDocument11 pagesDilip Buildcon: Strong ComebackPawan AsraniNo ratings yet

- Polycab India's Q1FY23 revenue up 48%, margins expandDocument10 pagesPolycab India's Q1FY23 revenue up 48%, margins expandResearch ReportsNo ratings yet

- Prabhudas Lilladher Apar Industries Q3DY24 Results ReviewDocument7 pagesPrabhudas Lilladher Apar Industries Q3DY24 Results ReviewvenkyniyerNo ratings yet

- Vinati Organics: AccumulateDocument7 pagesVinati Organics: AccumulateBhaveek OstwalNo ratings yet

- Apar IndustriesDocument6 pagesApar IndustriesMONIL BARBHAYANo ratings yet

- Bharat Forge (BHFC IN) : Q4FY21 Result UpdateDocument6 pagesBharat Forge (BHFC IN) : Q4FY21 Result UpdateEquity NestNo ratings yet

- JK Cement: Valuations Factor in Positive Downgrade To HOLDDocument9 pagesJK Cement: Valuations Factor in Positive Downgrade To HOLDShubham BawkarNo ratings yet

- Wipro (WPRO IN) : Q1FY22 Result UpdateDocument13 pagesWipro (WPRO IN) : Q1FY22 Result UpdatePrahladNo ratings yet

- United U-Li Corporation : OutperformDocument2 pagesUnited U-Li Corporation : OutperformZhi_Ming_Cheah_8136No ratings yet

- Q3FY22 Result Update Indo Count Industries LTD: Steady Numbers FY22E Volume Guidance ReducedDocument10 pagesQ3FY22 Result Update Indo Count Industries LTD: Steady Numbers FY22E Volume Guidance ReducedbradburywillsNo ratings yet

- JPMorgan SmurfitKappaH1resultswrap-accelerationfromhereasboxpricescomethrough Jul 28 2021Document15 pagesJPMorgan SmurfitKappaH1resultswrap-accelerationfromhereasboxpricescomethrough Jul 28 2021Camila CalderonNo ratings yet

- Suzlon Energy: Momentum Building UpDocument9 pagesSuzlon Energy: Momentum Building Uparun_algoNo ratings yet

- BP Plastics Holding Berhad Outperform : 1HFY21 Above ExpectationDocument4 pagesBP Plastics Holding Berhad Outperform : 1HFY21 Above ExpectationZhi_Ming_Cheah_8136No ratings yet

- Dolat Capital Market - Vinati Organics - Q2FY20 Result Update - 1Document6 pagesDolat Capital Market - Vinati Organics - Q2FY20 Result Update - 1Bhaveek OstwalNo ratings yet

- UltratechCement Edel 190118Document15 pagesUltratechCement Edel 190118suprabhattNo ratings yet

- Indofood CBP: Navigating WellDocument11 pagesIndofood CBP: Navigating WellAbimanyu LearingNo ratings yet

- DAGRI Growth AheadDocument7 pagesDAGRI Growth AheadanjugaduNo ratings yet

- Acc (Acc In) - Q2cy21 Result Update - PL IndiaDocument6 pagesAcc (Acc In) - Q2cy21 Result Update - PL IndiadarshanmaldeNo ratings yet

- Tata Steel - Q4FY22 Result Update - 05052022 - 05-05-2022 - 11Document9 pagesTata Steel - Q4FY22 Result Update - 05052022 - 05-05-2022 - 11varanasidineshNo ratings yet

- PC - JSW Q4FY21 Update - May 2021 20210522171333Document6 pagesPC - JSW Q4FY21 Update - May 2021 20210522171333Aniket DhanukaNo ratings yet

- H.G. Infra quarterly results beat estimates; maintain 'BuyDocument9 pagesH.G. Infra quarterly results beat estimates; maintain 'BuyDhavalNo ratings yet

- Britannia Equity ResearchDocument11 pagesBritannia Equity ResearchVaibhav BajpaiNo ratings yet

- UltraTech Cement's strong growth visibilityDocument10 pagesUltraTech Cement's strong growth visibilityLive NIftyNo ratings yet

- Nickel StudyDocument7 pagesNickel StudyILSEN N. DAETNo ratings yet

- Volume 5 - March 2022: Descriptions FY2021 FY2020 %Document5 pagesVolume 5 - March 2022: Descriptions FY2021 FY2020 %fielimkarelNo ratings yet

- Press Release Fy 21Document4 pagesPress Release Fy 21Esha ChaudharyNo ratings yet

- Hindalco Industries LTD - Q3FY24 Result Update - 14022024 - 14-02-2024 - 14Document9 pagesHindalco Industries LTD - Q3FY24 Result Update - 14022024 - 14-02-2024 - 14Nikhil GadeNo ratings yet

- Bhel (Bhel In) : Q4FY19 Result UpdateDocument6 pagesBhel (Bhel In) : Q4FY19 Result Updatesaran21No ratings yet

- Results FY2022Document27 pagesResults FY2022Sofia GuedesNo ratings yet

- Vinati Organics' PAP project to drive 95% revenue growthDocument21 pagesVinati Organics' PAP project to drive 95% revenue growthsujay85No ratings yet

- Jindal Stainless Profitability Surges on Strong DemandDocument9 pagesJindal Stainless Profitability Surges on Strong DemandAniket DhanukaNo ratings yet

- Ultratech Cement (UTCEM IN) : Q1FY21 Result UpdateDocument6 pagesUltratech Cement (UTCEM IN) : Q1FY21 Result UpdatewhitenagarNo ratings yet

- UAE Equity Research: Agthia Group PJSC Rating Maintained at BUYDocument5 pagesUAE Equity Research: Agthia Group PJSC Rating Maintained at BUYxen101No ratings yet

- AIA Engineering Feb 19Document6 pagesAIA Engineering Feb 19darshanmaldeNo ratings yet

- PC - Hindalco Q4FY21 Update - May 2021 20210522002841 PDFDocument6 pagesPC - Hindalco Q4FY21 Update - May 2021 20210522002841 PDFAniket DhanukaNo ratings yet

- DR - ADRO (2 Mei 2019)Document7 pagesDR - ADRO (2 Mei 2019)siput_lembekNo ratings yet

- AIA Engineering - Q4FY22 Result Update - 30 May 2022Document7 pagesAIA Engineering - Q4FY22 Result Update - 30 May 2022PavanNo ratings yet

- Polycab India's Strong Export Orders Drive FY20 Earnings GrowthDocument10 pagesPolycab India's Strong Export Orders Drive FY20 Earnings Growthkishore13No ratings yet

- UAE Equity Research Rates Agthia Group a Buy on Solid Growth OutlookDocument5 pagesUAE Equity Research Rates Agthia Group a Buy on Solid Growth Outlookxen101No ratings yet

- Heidelberg Cement India (HEIM IN) : Q3FY20 Result UpdateDocument6 pagesHeidelberg Cement India (HEIM IN) : Q3FY20 Result UpdateanjugaduNo ratings yet

- CMP: INR2,022 TP: INR2,636 (+30%) Stellar Growth, RM Exerts Pressure On MarginDocument10 pagesCMP: INR2,022 TP: INR2,636 (+30%) Stellar Growth, RM Exerts Pressure On MarginPoonam AggarwalNo ratings yet

- MARICO UPGRADEDocument8 pagesMARICO UPGRADEPranavPillaiNo ratings yet

- 2q 21 Earnings ReleaseDocument24 pages2q 21 Earnings ReleaseguitraderNo ratings yet

- Reaching Zero with Renewables: Biojet FuelsFrom EverandReaching Zero with Renewables: Biojet FuelsNo ratings yet

- ING Think Eurozone Inflation Divergence in Expectations DropsDocument6 pagesING Think Eurozone Inflation Divergence in Expectations DropsOwm Close CorporationNo ratings yet

- 5 Key Factors Facing U.S. Treasury Yields - Seeking AlphaDocument12 pages5 Key Factors Facing U.S. Treasury Yields - Seeking AlphaOwm Close CorporationNo ratings yet

- ING Think Rates Spark Inflation Reasserts Itself As The Main Driver of Rates 2Document5 pagesING Think Rates Spark Inflation Reasserts Itself As The Main Driver of Rates 2Owm Close CorporationNo ratings yet

- Invasion Effect On PGMS: Base Case Unchanged, But Upside Price RiskDocument4 pagesInvasion Effect On PGMS: Base Case Unchanged, But Upside Price RiskOwm Close CorporationNo ratings yet

- Blog - The WisdomTree Q2 2022 Economic and Market Outlook in 10 Charts or LessDocument11 pagesBlog - The WisdomTree Q2 2022 Economic and Market Outlook in 10 Charts or LessOwm Close CorporationNo ratings yet

- Blog - Fed Watch Nifty FiftyDocument3 pagesBlog - Fed Watch Nifty FiftyOwm Close CorporationNo ratings yet

- Gmo Resources Strategy: FactsDocument2 pagesGmo Resources Strategy: FactsOwm Close CorporationNo ratings yet

- ING Think China GDP Was Moderate But The Pain Should Come in 2qDocument3 pagesING Think China GDP Was Moderate But The Pain Should Come in 2qOwm Close CorporationNo ratings yet

- ING Think Us Housing Market Exhibits More Signs of SlowdownDocument6 pagesING Think Us Housing Market Exhibits More Signs of SlowdownOwm Close CorporationNo ratings yet

- Fed Hikes 50bp With Much More To Come: Economic and Financial AnalysisDocument5 pagesFed Hikes 50bp With Much More To Come: Economic and Financial AnalysisOwm Close CorporationNo ratings yet

- Blog - Anti Quality BubbleDocument6 pagesBlog - Anti Quality BubbleOwm Close CorporationNo ratings yet

- ING Think The Impact of The War in Ukraine On Food Agri Has Only Just Started To UnravelDocument7 pagesING Think The Impact of The War in Ukraine On Food Agri Has Only Just Started To UnravelOwm Close CorporationNo ratings yet

- Uncertainty Over Russian Gas Flows Means Large Risk Premium Will RemainDocument5 pagesUncertainty Over Russian Gas Flows Means Large Risk Premium Will RemainOwm Close CorporationNo ratings yet

- Blog - Quality For Uncertain TimesDocument6 pagesBlog - Quality For Uncertain TimesOwm Close CorporationNo ratings yet

- Blog - Is This A Defining Moment For The Bond MarketDocument4 pagesBlog - Is This A Defining Moment For The Bond MarketOwm Close CorporationNo ratings yet

- Lithium Exploration Budgets Rebounded in 2021 and Increased 25% Year Over Year To $249 MillionDocument3 pagesLithium Exploration Budgets Rebounded in 2021 and Increased 25% Year Over Year To $249 MillionOwm Close CorporationNo ratings yet

- Blog - Looking Back at Equity Factors in Q1 With WisdomTree-2Document7 pagesBlog - Looking Back at Equity Factors in Q1 With WisdomTree-2Owm Close CorporationNo ratings yet

- ING Think Japanese Investors Turn Cautious On Sovereign Bonds Ahead of Global QTDocument4 pagesING Think Japanese Investors Turn Cautious On Sovereign Bonds Ahead of Global QTOwm Close CorporationNo ratings yet

- An Impressive Start To The Year For Nickel As It Hits 10-Year HighDocument7 pagesAn Impressive Start To The Year For Nickel As It Hits 10-Year HighOwm Close CorporationNo ratings yet

- En - 20220322 Award of Epcm Contract To AfryDocument4 pagesEn - 20220322 Award of Epcm Contract To AfryOwm Close CorporationNo ratings yet

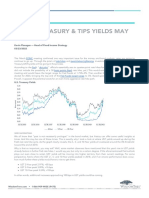

- Blog - Where Treasury TIPS Yields May Be HeadedDocument5 pagesBlog - Where Treasury TIPS Yields May Be HeadedOwm Close CorporationNo ratings yet

- The Flip Side of Large M&A DealsDocument6 pagesThe Flip Side of Large M&A DealsOwm Close CorporationNo ratings yet

- Endeavour Mining: Ninth Successive Year of OutperformanceDocument12 pagesEndeavour Mining: Ninth Successive Year of OutperformanceOwm Close CorporationNo ratings yet

- Horizonte Furnace - 20220225-Award-Of-Furnace-ContractDocument4 pagesHorizonte Furnace - 20220225-Award-Of-Furnace-ContractOwm Close CorporationNo ratings yet

- Copper Leans To The Upside Into Next QuarterDocument4 pagesCopper Leans To The Upside Into Next QuarterOwm Close CorporationNo ratings yet

- ING Think Aluminium Caught Up in Nickels Wild RideDocument4 pagesING Think Aluminium Caught Up in Nickels Wild RideOwm Close CorporationNo ratings yet

- ASX Release: Karouni Plant Site Where Construction Commenced in February 2015Document6 pagesASX Release: Karouni Plant Site Where Construction Commenced in February 2015Owm Close CorporationNo ratings yet

- Inflation: Don't You (Forget About Me) - Franklin TempletonDocument8 pagesInflation: Don't You (Forget About Me) - Franklin TempletonOwm Close CorporationNo ratings yet

- Rate Shock Pandemic Spreading - Juggling DynamiteDocument3 pagesRate Shock Pandemic Spreading - Juggling DynamiteOwm Close CorporationNo ratings yet

- ING Think Why Us Secs Proposed Climate Disclosure Rules Are A Game ChangerDocument6 pagesING Think Why Us Secs Proposed Climate Disclosure Rules Are A Game ChangerOwm Close CorporationNo ratings yet

- Manual Panasonic AG-DVC7Document4 pagesManual Panasonic AG-DVC7richercitolector01No ratings yet

- Primary Storage DevicesDocument2 pagesPrimary Storage DevicesOumotiaNo ratings yet

- 2012 PTQ q1Document132 pages2012 PTQ q1jainrakeshj4987No ratings yet

- Vitamin D For MS PatientsDocument1 pageVitamin D For MS PatientsDimitrios PapadimitriouNo ratings yet

- Upper Limb OrthosisDocument47 pagesUpper Limb OrthosisPraneethaNo ratings yet

- Isoefficiency Function A Scalability Metric For PaDocument20 pagesIsoefficiency Function A Scalability Metric For PaDasha PoluninaNo ratings yet

- Astm d5580Document9 pagesAstm d5580Nhu SuongNo ratings yet

- Ang Kin BalletDocument16 pagesAng Kin BalletJane JNo ratings yet

- Economic and Eco-Friendly Analysis of Solar Power Refrigeration SystemDocument5 pagesEconomic and Eco-Friendly Analysis of Solar Power Refrigeration SystemSiddh BhattNo ratings yet

- Roll No. Form No.: Private Admission Form S.S.C. Examination First Annual 2023 9th FRESHDocument3 pagesRoll No. Form No.: Private Admission Form S.S.C. Examination First Annual 2023 9th FRESHBeenish MirzaNo ratings yet

- ZDocument6 pagesZDinesh SelvakumarNo ratings yet

- Aluminum Wire Data and PropertiesDocument31 pagesAluminum Wire Data and PropertiesMaria SNo ratings yet

- Diease LossDocument10 pagesDiease LossGeetha EconomistNo ratings yet

- Class-Directory-of-SY-2019-2020-on-ctuc200 (psh1)Document5 pagesClass-Directory-of-SY-2019-2020-on-ctuc200 (psh1)Narciso Ana JenecelNo ratings yet

- Seaskills Maritime Academy: Purchase OrderDocument8 pagesSeaskills Maritime Academy: Purchase OrderSELVA GANESHNo ratings yet

- Induction Motor StarterDocument5 pagesInduction Motor StarterAnikendu MaitraNo ratings yet

- Showcase your talent and skills at Momentum 2021Document48 pagesShowcase your talent and skills at Momentum 2021Tanishq VermaNo ratings yet

- Learner's Module in Grade 7 Mathematics Pages 1 - 4 Global Mathematics, Page 2 - 18 Synergy For Success in Mathematics, Pages 2 - 13Document12 pagesLearner's Module in Grade 7 Mathematics Pages 1 - 4 Global Mathematics, Page 2 - 18 Synergy For Success in Mathematics, Pages 2 - 13Maricel Tarenio MacalinoNo ratings yet

- CUMINDocument17 pagesCUMIN19BFT Food TechnologyNo ratings yet

- Kanishkar H - ResumeDocument1 pageKanishkar H - ResumeSURYA ANo ratings yet

- E-Learning - Learning For Smart GenerationZ-Dr.U.S.pandey, Sangita RawalDocument2 pagesE-Learning - Learning For Smart GenerationZ-Dr.U.S.pandey, Sangita RawaleletsonlineNo ratings yet

- MITSUBISHI Elevator PDFDocument12 pagesMITSUBISHI Elevator PDFBirhami AkhirNo ratings yet

- WMA14 01 Rms 20220199 UNUSEDDocument17 pagesWMA14 01 Rms 20220199 UNUSEDVanessa NgNo ratings yet

- Haas Accessories FlyerDocument12 pagesHaas Accessories FlyerAndrewFranciscoNo ratings yet

- Windows 7 Dial-Up Connection Setup GuideDocument7 pagesWindows 7 Dial-Up Connection Setup GuideMikeNo ratings yet

- Expert Coaching CatalogDocument37 pagesExpert Coaching CatalogJosh WhiteNo ratings yet

- LU9245Document2 pagesLU9245mudassir.bukhariNo ratings yet

- Understanding and Applying The ANSI/ ISA 18.2 Alarm Management StandardDocument260 pagesUnderstanding and Applying The ANSI/ ISA 18.2 Alarm Management StandardHeri Fadli SinagaNo ratings yet

- Chem 101 Fall17 Worksheet 2Document2 pagesChem 101 Fall17 Worksheet 2mikayla sirovatkaNo ratings yet

- Topics in English SyntaxDocument131 pagesTopics in English SyntaxPro GamerNo ratings yet