You might also like

- Gift Card Hack MethodDocument8 pagesGift Card Hack MethodEphantus0% (1)

- Memo On Uniform Implementation of DO 174Document3 pagesMemo On Uniform Implementation of DO 174Anonymous XvwKtnSrMR100% (2)

- Screenshot 2022-08-04 at 12.53.07 PDFDocument1 pageScreenshot 2022-08-04 at 12.53.07 PDFSimi NaomiNo ratings yet

- Bureau of Customs CMO-28-2017Document1 pageBureau of Customs CMO-28-2017PortCallsNo ratings yet

- PDFDocument514 pagesPDFAli KuscuNo ratings yet

- 3 6bitcoinDocument1 page3 6bitcoinjohn.whiteNo ratings yet

- 2014-2019 TAXATION LAW BAR Questions and AnswersDocument81 pages2014-2019 TAXATION LAW BAR Questions and AnswersJuris Mendoza74% (19)

- EH403 TAXATION MIDTERMS Estate and Donors - EditedDocument22 pagesEH403 TAXATION MIDTERMS Estate and Donors - Editedethel hyugaNo ratings yet

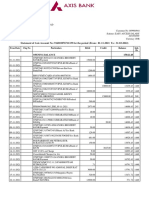

- Statement of Axis Account No:916010076711339 For The Period (From: 01-11-2021 To: 31-03-2022)Document5 pagesStatement of Axis Account No:916010076711339 For The Period (From: 01-11-2021 To: 31-03-2022)kaushik kaklotarNo ratings yet

- Your Personal Bank Chequing Account Statement: Toronto, ON M5W 1L5Document2 pagesYour Personal Bank Chequing Account Statement: Toronto, ON M5W 1L5John BarrNo ratings yet

- Payslip 90002364 10 2020Document1 pagePayslip 90002364 10 2020souvik deyNo ratings yet

- Tax Notes (Dizon Book)Document3 pagesTax Notes (Dizon Book)Enteng KabisoteNo ratings yet

- Verbiage of MT 799 and MT 760Document4 pagesVerbiage of MT 799 and MT 760Narayan Arul100% (3)

- 2024 53 Aocg MemoDocument3 pages2024 53 Aocg Memokiluwa2022No ratings yet

- CAO 04 2021 Processing of TPC Transactions Under The CARS ProgramDocument5 pagesCAO 04 2021 Processing of TPC Transactions Under The CARS ProgramCarlo GiancarloNo ratings yet

- cmc-131-2021-FDA Updates and List of VAT-Exempt ProductsDocument50 pagescmc-131-2021-FDA Updates and List of VAT-Exempt ProductsCHUBZ0902No ratings yet

- RMC No 35-2016Document2 pagesRMC No 35-2016Rodel Ryan YanaNo ratings yet

- DHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 08-12-2004 Order Number 40-YA-BC-493795Document2 pagesDHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 08-12-2004 Order Number 40-YA-BC-493795CREWNo ratings yet

- Bureau of Customs Memo 2018-04-009 Extension of The Suspension of The-Implementation of CAO 05-2016Document4 pagesBureau of Customs Memo 2018-04-009 Extension of The Suspension of The-Implementation of CAO 05-2016PortCallsNo ratings yet

- $i ,, :, 9. ! !! ,, 0Ms I, ,: June 21 2021 .'/ :. 'PYDocument3 pages$i ,, :, 9. ! !! ,, 0Ms I, ,: June 21 2021 .'/ :. 'PYmitch galaxNo ratings yet

- FSA Fod6E1nDocument1 pageFSA Fod6E1nAlfred SorenNo ratings yet

- Contract New Format - 12GG0041Document5 pagesContract New Format - 12GG0041MadonnaTipawanNo ratings yet

- Rmo No.47-2019Document2 pagesRmo No.47-2019Sid CandelariaNo ratings yet

- Amending RR No. 12-2013 on Valuation of Gifts in PropertyDocument1 pageAmending RR No. 12-2013 on Valuation of Gifts in PropertyGil PinoNo ratings yet

- Order-Us-119-F-No - 275252020-ItDocument3 pagesOrder-Us-119-F-No - 275252020-ItBlue CliffNo ratings yet

- DHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 01-14-2005 Order Number 43-YA-BC-599047Document2 pagesDHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 01-14-2005 Order Number 43-YA-BC-599047CREWNo ratings yet

- COA - M2018-001 Pagibig RemittanceDocument25 pagesCOA - M2018-001 Pagibig RemittanceYusairah DarapaNo ratings yet

- Commissioner Oflnterial O35eDocument4 pagesCommissioner Oflnterial O35eMartin SandersonNo ratings yet

- Investment Incentives Regulation No. 84 of 2000Document9 pagesInvestment Incentives Regulation No. 84 of 2000abdume74No ratings yet

- RR No. 7-2017Document2 pagesRR No. 7-2017Lenin Rey PolonNo ratings yet

- DHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 08-20-1998 Order Number 40-YA-BC-803055Document2 pagesDHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 08-20-1998 Order Number 40-YA-BC-803055CREWNo ratings yet

- 7172 22 Si OgDocument14 pages7172 22 Si OgB N Law AssociatesNo ratings yet

- REVOKING REVENUE REGULATIONS REINSTATING PRIOR PROVISIONSDocument2 pagesREVOKING REVENUE REGULATIONS REINSTATING PRIOR PROVISIONSAndrew Benedict PardilloNo ratings yet

- RMC No. 7-2021Document1 pageRMC No. 7-2021nathalie velasquezNo ratings yet

- MERALCO liable for real property tax on electric facilitiesDocument18 pagesMERALCO liable for real property tax on electric facilitiesMeku DigeNo ratings yet

- Government of India Amends Merchant Shipping Rules to Comply with MLC 2006 AmendmentsDocument4 pagesGovernment of India Amends Merchant Shipping Rules to Comply with MLC 2006 AmendmentsQUADRANT MARITIMENo ratings yet

- JKLSFDocument11 pagesJKLSFYrra LimchocNo ratings yet

- Esic Chinta Se Mukti: Extension of ESI Scheme To Construction Site Workers-RegDocument6 pagesEsic Chinta Se Mukti: Extension of ESI Scheme To Construction Site Workers-Reggurparvinder singhNo ratings yet

- RR No. 10-2021Document2 pagesRR No. 10-2021eric yuulNo ratings yet

- CMO 06 2020 Automated Clearance Procedures For Commercial Goods On Informal Entry Process PDFDocument6 pagesCMO 06 2020 Automated Clearance Procedures For Commercial Goods On Informal Entry Process PDFoperations.foxlogisticsNo ratings yet

- CMO29 2015 Revised Procedures Documentation Process For Formal Consumption EntryDocument2 pagesCMO29 2015 Revised Procedures Documentation Process For Formal Consumption Entryusjrlaw2011No ratings yet

- DLLL 164) LL Iziti:Tlli: National Highways Authority of IndiaDocument2 pagesDLLL 164) LL Iziti:Tlli: National Highways Authority of Indiaakshay gargNo ratings yet

- Tw. - NSRZ: 1ffi - $&Ffi.'Ri A.T4Document1 pageTw. - NSRZ: 1ffi - $&Ffi.'Ri A.T4Lenin Rey PolonNo ratings yet

- RMC No. 6-2022Document2 pagesRMC No. 6-2022Gretch PanoNo ratings yet

- DAO 2, s.1994 - Further Amending MO 32, s.1985Document10 pagesDAO 2, s.1994 - Further Amending MO 32, s.1985ATTY. R.A.L.C.No ratings yet

- RMC No. 134-2019Document1 pageRMC No. 134-2019cris gerard trinidadNo ratings yet

- Mcgraw Hills Essentials of Federal Taxation 2019 10th Edition Spilker Solutions ManualDocument19 pagesMcgraw Hills Essentials of Federal Taxation 2019 10th Edition Spilker Solutions Manualairpoiseanalyzernt5t100% (21)

- DHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 10-14-1999 Order Number 43-YA-BC-019869Document2 pagesDHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 10-14-1999 Order Number 43-YA-BC-019869CREWNo ratings yet

- M S Oblum Electrical Industries PVT Vs Collector of Customs Bombay On 2 September 1997Document6 pagesM S Oblum Electrical Industries PVT Vs Collector of Customs Bombay On 2 September 1997Mahi SNo ratings yet

- RMC No. 117-2021 Clarification On Submission of 2307 and 2316Document2 pagesRMC No. 117-2021 Clarification On Submission of 2307 and 2316Gerald SantosNo ratings yet

- ShowfileDocument17 pagesShowfileSandip YadavNo ratings yet

- International Tonnage Certificate (Surat Ukur)Document3 pagesInternational Tonnage Certificate (Surat Ukur)Samsul Basri LubisNo ratings yet

- Revenue Regulations No. 6 ' 9.0 2 2: Muauc Ofthe Philippines Department or FinanceDocument3 pagesRevenue Regulations No. 6 ' 9.0 2 2: Muauc Ofthe Philippines Department or FinancerodrigoNo ratings yet

- Aug 31, 2005Document6 pagesAug 31, 2005ishubhojeetNo ratings yet

- M-Oogane@Tokyo-Keiki Co JPDocument4 pagesM-Oogane@Tokyo-Keiki Co JPsophietkdpurchasingNo ratings yet

- RMC No 19-2018Document2 pagesRMC No 19-2018Paul GeorgeNo ratings yet

- RMC No 24-2019 Submission of Bir Form 2316Document2 pagesRMC No 24-2019 Submission of Bir Form 2316joelsy100100% (1)

- Carpio Vs Modair Manila Co. LTD., Inc.Document25 pagesCarpio Vs Modair Manila Co. LTD., Inc.Rudnar Jay Bañares BarbaraNo ratings yet

- RMC No 38-2019Document1 pageRMC No 38-2019TrishNo ratings yet

- Coord AmendmentEPFSch PenSchDocument11 pagesCoord AmendmentEPFSch PenSchyogesh gangjiNo ratings yet

- RDO 45-MarikinaOMDocument132 pagesRDO 45-MarikinaOM6rainbow50% (6)

- Response To SCNDocument15 pagesResponse To SCNRama KamalNo ratings yet

- RMC 2017 No. 104 Circularizing TRAIN Law & President's Veto MessageDocument1 pageRMC 2017 No. 104 Circularizing TRAIN Law & President's Veto MessageBien Bowie A. CortezNo ratings yet

- Act 631 Finance Act 2003Document20 pagesAct 631 Finance Act 2003Adam Haida & CoNo ratings yet

- DHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 10-19-1999 Order Number 43-YA-BC-020221Document2 pagesDHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 10-19-1999 Order Number 43-YA-BC-020221CREWNo ratings yet

- DHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 01-03-2003 Order Number 43-YA-BC-373468Document2 pagesDHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 01-03-2003 Order Number 43-YA-BC-373468CREWNo ratings yet

- DHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 04-01-1999 Order Number 43-YA-BC-910655Document2 pagesDHS, FEMA and Dept. of State: Failure of Hurricane Relief Efforts: 04-01-1999 Order Number 43-YA-BC-910655CREWNo ratings yet

- RR 5-2016Document3 pagesRR 5-2016McrislbNo ratings yet

- Petroleum Exploration and Exploitation in NorwayFrom EverandPetroleum Exploration and Exploitation in NorwayRating: 5 out of 5 stars5/5 (1)

- $i ,, :, 9. ! !! ,, 0Ms I, ,: June 21 2021 .'/ :. 'PYDocument3 pages$i ,, :, 9. ! !! ,, 0Ms I, ,: June 21 2021 .'/ :. 'PYmitch galaxNo ratings yet

- Congratulations Selected Candidates Customs BureauDocument4 pagesCongratulations Selected Candidates Customs Bureaumitch galaxNo ratings yet

- 23 Letter To Hon. Irene Alejano-MesoDocument3 pages23 Letter To Hon. Irene Alejano-Mesomitch galaxNo ratings yet

- Icommissionej, ,, I L I !: Bureau of CustomsDocument4 pagesIcommissionej, ,, I L I !: Bureau of Customsmitch galaxNo ratings yet

- We Wish To Inform You of Your Selection For Issuance of Appointment To The Following PositionsDocument5 pagesWe Wish To Inform You of Your Selection For Issuance of Appointment To The Following Positionsmitch galaxNo ratings yet

- 11 - Notice of Appointment Various Positions POM MICP Cebu Leg SubicDocument3 pages11 - Notice of Appointment Various Positions POM MICP Cebu Leg Subicmitch galaxNo ratings yet

- 19 Tagoloan Sangguniang Bayan RESOLUTION No. 261, S. 2018 - 2Document3 pages19 Tagoloan Sangguniang Bayan RESOLUTION No. 261, S. 2018 - 2mitch galaxNo ratings yet

- 25 Interpol RED Notice Cho Chulsoo Fugitive Wanted April 17, 20Document3 pages25 Interpol RED Notice Cho Chulsoo Fugitive Wanted April 17, 20mitch galaxNo ratings yet

- MICP - Readiness Report NG Xray FindingsDocument2 pagesMICP - Readiness Report NG Xray Findingsmitch galaxNo ratings yet

- Philippine Customs Repatriates Illegal Korean WasteDocument9 pagesPhilippine Customs Repatriates Illegal Korean Wastemitch galaxNo ratings yet

- Qualification StandardsDocument1 pageQualification Standardsmitch galaxNo ratings yet

- 41 PICTURES OF REEXPORTATION OF ILLEGAL WASTES-mergedDocument12 pages41 PICTURES OF REEXPORTATION OF ILLEGAL WASTES-mergedmitch galaxNo ratings yet

- 22 51 Containers 31-35 (Pics)Document5 pages22 51 Containers 31-35 (Pics)mitch galaxNo ratings yet

- 23 Letter To Hon. Irene Alejano-MesoDocument3 pages23 Letter To Hon. Irene Alejano-Mesomitch galaxNo ratings yet

- Interview Questionnaire (EMNSA)Document7 pagesInterview Questionnaire (EMNSA)mitch galaxNo ratings yet

- 26 Resolution On Preliminary Investigation 91-97Document7 pages26 Resolution On Preliminary Investigation 91-97mitch galaxNo ratings yet

- Green Guide Customs MEAs 2018Document114 pagesGreen Guide Customs MEAs 2018mitch galaxNo ratings yet

- Ocom Turn SlipDocument1 pageOcom Turn Slipmitch galaxNo ratings yet

- Turn-Over Slip: Turned-Over By: Received byDocument1 pageTurn-Over Slip: Turned-Over By: Received bymitch galaxNo ratings yet

- Survey Questionnaire (EMNSA)Document18 pagesSurvey Questionnaire (EMNSA)mitch galaxNo ratings yet

- Ocom Turn SlipDocument1 pageOcom Turn Slipmitch galaxNo ratings yet

- We Give Our Yes - Jamie Rivera Song LyricsDocument1 pageWe Give Our Yes - Jamie Rivera Song LyricsDomingo F. Combate Jr.No ratings yet

- Prayer Before PilgrimageDocument1 pagePrayer Before Pilgrimagemitch galaxNo ratings yet

- What is a plenary indulgenceDocument5 pagesWhat is a plenary indulgencemitch galaxNo ratings yet

- Prayer Before PilgrimageDocument1 pagePrayer Before Pilgrimagemitch galaxNo ratings yet

- List of Jubilee Churches in The CountryDocument18 pagesList of Jubilee Churches in The Countrymitch galaxNo ratings yet

- Volume & Revenue Analysis January 18, 2021Document23 pagesVolume & Revenue Analysis January 18, 2021mitch galaxNo ratings yet

- Father Pio Healing PrayerDocument1 pageFather Pio Healing Prayermitch galaxNo ratings yet

- 1 EcoWaste Coalition Honors Customs Official With Environmental Justice AwardDocument3 pages1 EcoWaste Coalition Honors Customs Official With Environmental Justice Awardmitch galaxNo ratings yet

- CREATE Salient ProvisionsDocument3 pagesCREATE Salient ProvisionsAldrin Santos AntonioNo ratings yet

- C5 Sa PIjm 8 W6 HH6 IrDocument7 pagesC5 Sa PIjm 8 W6 HH6 Irarun royNo ratings yet

- Digitec - Sales Receipt - 81894093Document1 pageDigitec - Sales Receipt - 81894093smokin tigernenteNo ratings yet

- Taxation Semester VI T. Y. B. ComDocument265 pagesTaxation Semester VI T. Y. B. ComSushant kawadeNo ratings yet

- China Bank Capital Loss RulingDocument107 pagesChina Bank Capital Loss RulingHi Law School0% (1)

- 2 - Madrigal Vs RaffertyDocument7 pages2 - Madrigal Vs RaffertyCollen Anne PagaduanNo ratings yet

- Manage Payroll Easily in 40 CharactersDocument7 pagesManage Payroll Easily in 40 CharacterssamruddhiNo ratings yet

- Pension Withdrawal GuideDocument6 pagesPension Withdrawal GuideKathleen Catubay SamsonNo ratings yet

- OpTransactionHistory21 01 2016Document3 pagesOpTransactionHistory21 01 2016venkatesanjsNo ratings yet

- NEFT Challan details for payment to Dr A P J Abdul Kalam Tech UnivDocument1 pageNEFT Challan details for payment to Dr A P J Abdul Kalam Tech UnivMradal TiwariNo ratings yet

- Hotel Eastern Gate: Subhanighat, Bishwroad, Sylhet, BangladeshDocument1 pageHotel Eastern Gate: Subhanighat, Bishwroad, Sylhet, BangladeshNightof NomoonNo ratings yet

- Discount (October 1)Document9 pagesDiscount (October 1)Shiela Marie FranciscoNo ratings yet

- XDocument2 pagesXSophiaFrancescaEspinosaNo ratings yet

- FRFRDocument3 pagesFRFRNaeem AhmadNo ratings yet

- Group 6Document27 pagesGroup 6Joyce Kay AzucenaNo ratings yet

- Benefit Illustration For HDFC Life Sanchay Par AdvantageDocument3 pagesBenefit Illustration For HDFC Life Sanchay Par AdvantageLaviNo ratings yet

- Discussion Forum Bus 5111 Unit 2Document2 pagesDiscussion Forum Bus 5111 Unit 2MohamedNo ratings yet

- Financial RelationsDocument4 pagesFinancial RelationsPriti PatelNo ratings yet

- Tax Invoice for Fortune Oil and Soya ProductsDocument1 pageTax Invoice for Fortune Oil and Soya ProductsCA Shrikant VaranasiNo ratings yet

- E-Filing of Income Tax Return: SUBMITTED BY: Nisha Ghodake Roll No: 17019. (Functional Project)Document7 pagesE-Filing of Income Tax Return: SUBMITTED BY: Nisha Ghodake Roll No: 17019. (Functional Project)NISHA GHODAKENo ratings yet