You might also like

- Experiencing Change in German Controlling: Management Accounting in a Globalizing WorldFrom EverandExperiencing Change in German Controlling: Management Accounting in a Globalizing WorldNo ratings yet

- Lesson 09 Financial AnalysisDocument72 pagesLesson 09 Financial AnalysisMar SantosNo ratings yet

- "How Well Am I Doing?" Financial Statement Analysis: Chapter SixteenDocument72 pages"How Well Am I Doing?" Financial Statement Analysis: Chapter SixteenJudith Ann EscobarNo ratings yet

- MA-16-How Well Am I Doing - Financial Statement AnalysisDocument72 pagesMA-16-How Well Am I Doing - Financial Statement AnalysisAna Patricia Basa MacapagalNo ratings yet

- Financial Statement Analysis: Mcgraw-Hill/IrwinDocument58 pagesFinancial Statement Analysis: Mcgraw-Hill/Irwinberna taştanNo ratings yet

- Financial RatiosDocument63 pagesFinancial RatiosrdttecNo ratings yet

- Chapter 3 (Accounting - What The Numbers Mean 10e)Document17 pagesChapter 3 (Accounting - What The Numbers Mean 10e)Nguyen Dac ThichNo ratings yet

- Chapter 3 (Accounting - What The Numbers Mean 10e)Document17 pagesChapter 3 (Accounting - What The Numbers Mean 10e)Nguyen Dac ThichNo ratings yet

- The Basis For Business Decisions: Financial & Managerial AccountingDocument59 pagesThe Basis For Business Decisions: Financial & Managerial AccountingTajalli FatimaNo ratings yet

- Chap 003Document16 pagesChap 003fdiinvestimetNo ratings yet

- FINMAN Financial-Statement-Analysis PDFDocument66 pagesFINMAN Financial-Statement-Analysis PDFstel mariNo ratings yet

- Chap017-Financial Statement AnalysisDocument21 pagesChap017-Financial Statement AnalysismarseliaNo ratings yet

- Long Term Decision Making Capital Budgeting Decisions: Mcgraw-Hill/IrwinDocument55 pagesLong Term Decision Making Capital Budgeting Decisions: Mcgraw-Hill/IrwinjaganishNo ratings yet

- ACN Chap 1Document55 pagesACN Chap 1Rabbi RahmanNo ratings yet

- Accounting Chapter 9Document89 pagesAccounting Chapter 9api-27283455No ratings yet

- Corporate Financing and The Six Lessons of Market EfficiencyDocument25 pagesCorporate Financing and The Six Lessons of Market EfficiencyHasnain KharNo ratings yet

- Ch13 ACCT1101 S1 2223 MoodleDocument70 pagesCh13 ACCT1101 S1 2223 Moodle华邦盛No ratings yet

- Chap017 - Financial and Accounting InforDocument30 pagesChap017 - Financial and Accounting InforNgân KimNo ratings yet

- Goals and Governance of The Corporation Goals and Governance of The Corporation Accounting and FinanceDocument32 pagesGoals and Governance of The Corporation Goals and Governance of The Corporation Accounting and FinanceAbdullah BugshanNo ratings yet

- Project Analysis: Fundamentals of Corporate FinanceDocument18 pagesProject Analysis: Fundamentals of Corporate FinanceFahad ShaikhNo ratings yet

- Chapter 004 - Profit PlanningDocument81 pagesChapter 004 - Profit PlanningCẩm Tuyền Lê ThịNo ratings yet

- Chapter 4 (Accounting - What The Numbers Mean 10e)Document22 pagesChapter 4 (Accounting - What The Numbers Mean 10e)Nguyen Dac ThichNo ratings yet

- The Basis For Business Decisions: Williams Haka Bettner MeigsDocument20 pagesThe Basis For Business Decisions: Williams Haka Bettner Meigsdevansh kakkarNo ratings yet

- CH 12Document36 pagesCH 12qiqi fNo ratings yet

- Analyzing and Interpreting Financial Statements: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinDocument67 pagesAnalyzing and Interpreting Financial Statements: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinAmGad SHarifNo ratings yet

- Intro 22Document23 pagesIntro 22Asad HaiderNo ratings yet

- Financial & Managerial Accounting: The Basis For Business DecisionsDocument29 pagesFinancial & Managerial Accounting: The Basis For Business DecisionsAndleeb UmerNo ratings yet

- Financial Statement Analysis: Mcgraw-Hill/Irwin © The Mcgraw-Hill Companies, Inc., 2005Document50 pagesFinancial Statement Analysis: Mcgraw-Hill/Irwin © The Mcgraw-Hill Companies, Inc., 2005Kumail AbbasNo ratings yet

- Flexible Budgets and Overhead Analysis: Mcgraw-Hill/IrwinDocument78 pagesFlexible Budgets and Overhead Analysis: Mcgraw-Hill/Irwinsaka haiNo ratings yet

- Chapter 01Document28 pagesChapter 01Ayesha ZahidNo ratings yet

- Chap002 MacroeconomíaDocument13 pagesChap002 MacroeconomíaVictor Alfonso Barrera TrujilloNo ratings yet

- Master Budgets and Planning: © The Mcgraw-Hill Companies, Inc., 2007 Mcgraw-Hill/IrwinDocument64 pagesMaster Budgets and Planning: © The Mcgraw-Hill Companies, Inc., 2007 Mcgraw-Hill/IrwinVy VõNo ratings yet

- Chapter 11Document78 pagesChapter 11Anggitha Ayu F.PNo ratings yet

- Essentials of Financial Statement Analysis: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 5Document34 pagesEssentials of Financial Statement Analysis: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 5Dylan AdrianNo ratings yet

- Libby 10e Chap013Document53 pagesLibby 10e Chap013rakan.cocoNo ratings yet

- Financial Statement AnalysisDocument35 pagesFinancial Statement Analysispuja raulNo ratings yet

- Practical Investment Management by Robert.A.Strong Slides ch08Document28 pagesPractical Investment Management by Robert.A.Strong Slides ch08mzqaceNo ratings yet

- Chapter 16Document15 pagesChapter 16Hưng Lê QuangNo ratings yet

- "How Well Am I Doing?" Financial Statement Analysis: Dr. Eduardo Bustos FaríasDocument38 pages"How Well Am I Doing?" Financial Statement Analysis: Dr. Eduardo Bustos FaríasMies OdellNo ratings yet

- Cash FlowDocument56 pagesCash Flowhunza1100% (2)

- Financial Statement AnalysisDocument85 pagesFinancial Statement AnalysisJasmine Bete CabasaNo ratings yet

- The Accounting Cycle: Accruals and DeferralsDocument51 pagesThe Accounting Cycle: Accruals and DeferralsSaira Saeed0% (1)

- Chapter 11-4Document78 pagesChapter 11-4Amy SIlverbergNo ratings yet

- Chapter 2 - RevDocument36 pagesChapter 2 - Revarhamali.179No ratings yet

- Interest Rate Risk IDocument17 pagesInterest Rate Risk Ianon_215805No ratings yet

- Financial Statement Analysis Chapter 15Document13 pagesFinancial Statement Analysis Chapter 15April N. Alfonso100% (1)

- © Mcgraw Hill Companies, Inc., 2000Document19 pages© Mcgraw Hill Companies, Inc., 2000RamadeviChowdaryRayapatiNo ratings yet

- Operating and Financial Leverage: Block, Hirt, and DanielsenDocument31 pagesOperating and Financial Leverage: Block, Hirt, and DanielsenOona NiallNo ratings yet

- Expense-To-Sales RatioDocument3 pagesExpense-To-Sales RatioRaman KulkarniNo ratings yet

- Kuliah Pertm#7Document78 pagesKuliah Pertm#7Satria D' LigtningNo ratings yet

- Lec 2Document10 pagesLec 2munnicod64No ratings yet

- Income and Changes in Retained EarningsDocument36 pagesIncome and Changes in Retained EarningsComm SofianNo ratings yet

- Bab 10 Anggaran FleksibelDocument73 pagesBab 10 Anggaran FleksibelAdinda Novia SariNo ratings yet

- Segment Reporting and Decentralization: Chapter TwelveDocument119 pagesSegment Reporting and Decentralization: Chapter TwelveAtif SaeedNo ratings yet

- Valuing Stocks: Fundamentals of Corporate FinanceDocument32 pagesValuing Stocks: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Financial Analysis - KHCDocument9 pagesFinancial Analysis - KHCapi-643732098No ratings yet

- The Value of Common Stocks: Principles of Corporate FinanceDocument31 pagesThe Value of Common Stocks: Principles of Corporate FinanceGodson AkwoviahNo ratings yet

- Investment Decision Making Between Games Workshop and Hornby Finance EssayDocument23 pagesInvestment Decision Making Between Games Workshop and Hornby Finance EssayHND Assignment HelpNo ratings yet

- Cost-Volume-Profit Relationships: The Mcgraw-Hill Companies, Inc. 2008 Mcgraw-Hill/IrwinDocument25 pagesCost-Volume-Profit Relationships: The Mcgraw-Hill Companies, Inc. 2008 Mcgraw-Hill/IrwinCharina Jenine T. TraqueñaNo ratings yet

- Chap9 BudgetingDocument83 pagesChap9 Budgetinggeorgiana tesoiNo ratings yet

- Retail MathDocument7 pagesRetail MathApaar Arora50% (2)

- 3.2 Data Tables Class ExcerciseDocument15 pages3.2 Data Tables Class ExcerciseRaghavendra NaduvinamaniNo ratings yet

- Poa SbaDocument31 pagesPoa SbaAshley AngelNo ratings yet

- BUS 630 Week 1 AssignmentDocument5 pagesBUS 630 Week 1 Assignmenttaranisha29No ratings yet

- Variable and Absorption Costing Activity (Pagarigan, R.)Document4 pagesVariable and Absorption Costing Activity (Pagarigan, R.)Rendyel PagariganNo ratings yet

- UniqloDocument17 pagesUniqloUmar GondalNo ratings yet

- Powersports Business Market Data Book 2019Document68 pagesPowersports Business Market Data Book 2019Harmanpreet SinghNo ratings yet

- HikalDocument22 pagesHikalADNo ratings yet

- Cottle-Taylor India: 02 Income Statement (Patel) 03 Income Statement (Lang) 04 Proposed Income StatementDocument16 pagesCottle-Taylor India: 02 Income Statement (Patel) 03 Income Statement (Lang) 04 Proposed Income StatementDeepakRamNo ratings yet

- Job CostingDocument28 pagesJob CostingAbi BieNo ratings yet

- Arba Minch University College of Agricultural Sciences Department of Agribusiness and Value Chain ManagementDocument55 pagesArba Minch University College of Agricultural Sciences Department of Agribusiness and Value Chain Managementdursam328No ratings yet

- Preschool Business TempDocument28 pagesPreschool Business TempMilan SonigraNo ratings yet

- Project Case - Brannigan Foods - Financial CalculationsDocument2 pagesProject Case - Brannigan Foods - Financial CalculationsDuyên NguyễnNo ratings yet

- Architecture Firm Business PlanDocument28 pagesArchitecture Firm Business PlanOliviaNo ratings yet

- CH 9 Intermediate Accounting Test BankDocument40 pagesCH 9 Intermediate Accounting Test Bankhisyam kinciNo ratings yet

- CHAPTER 7 by ProductDocument4 pagesCHAPTER 7 by Productliyneh mebrahituNo ratings yet

- Daiso of Japan The Dollar Store Harvard Case Study Solution & Online Case AnalysisDocument22 pagesDaiso of Japan The Dollar Store Harvard Case Study Solution & Online Case AnalysisAgota FlaiszNo ratings yet

- Audit of Taj HotelDocument34 pagesAudit of Taj HotelAkashTokeNo ratings yet

- Management Accounting Concept and Application by Cabrera PDFDocument29 pagesManagement Accounting Concept and Application by Cabrera PDFMar-ramos Ramos50% (6)

- Business Proposal Barber ShopDocument7 pagesBusiness Proposal Barber Shopkings kingsNo ratings yet

- Tell Me A Story - ACCA GlobalDocument11 pagesTell Me A Story - ACCA GlobalAccounts DXCentreNo ratings yet

- Financial Accounting Module 6 SummaryDocument6 pagesFinancial Accounting Module 6 SummaryKashika LathNo ratings yet

- Annual Report Analysis - Maruti Suzuki LTD 2Document60 pagesAnnual Report Analysis - Maruti Suzuki LTD 2naman_popli50% (2)

- Womens Clothing Boutique Business PlanDocument64 pagesWomens Clothing Boutique Business PlanyodamNo ratings yet

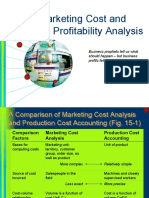

- Marketing Cost and Profitability AnalysisDocument10 pagesMarketing Cost and Profitability AnalysisBharathi RajuNo ratings yet

- Cradle-to-Cradle Design at Herman Miller: Moving Toward Environmental SustainabilityDocument15 pagesCradle-to-Cradle Design at Herman Miller: Moving Toward Environmental Sustainabilitysn0134No ratings yet

- Lecture 5: Cost, Price, and Price For Performance: Professor Randy H. Katz Computer Science 252 Spring 1996Document29 pagesLecture 5: Cost, Price, and Price For Performance: Professor Randy H. Katz Computer Science 252 Spring 1996saddamhussain4No ratings yet

- Mother Earth News 004Document102 pagesMother Earth News 004Jan PranNo ratings yet

- Analysis of Central Insurance Canada Case 1Document7 pagesAnalysis of Central Insurance Canada Case 1Aashan Paul100% (1)

- TRANSFER PRICING AT TIMKEN Update 2017Document13 pagesTRANSFER PRICING AT TIMKEN Update 2017ihsan hassouneNo ratings yet