You might also like

- QnA ISA 200 & ISA 210Document5 pagesQnA ISA 200 & ISA 210auditNo ratings yet

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeFrom EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeRating: 5 out of 5 stars5/5 (1)

- Tutorial 1 Q ADocument5 pagesTutorial 1 Q AKelvin LeongNo ratings yet

- Information Systems Auditing: The IS Audit Reporting ProcessFrom EverandInformation Systems Auditing: The IS Audit Reporting ProcessRating: 4.5 out of 5 stars4.5/5 (3)

- Lesson 1 - Overview of The Risk-Based Audit ProcessDocument7 pagesLesson 1 - Overview of The Risk-Based Audit ProcessYANIII12345No ratings yet

- Handout 2 - Introduction To Auditing and Assurance of Specialized IndustriesDocument2 pagesHandout 2 - Introduction To Auditing and Assurance of Specialized IndustriesPotato CommissionerNo ratings yet

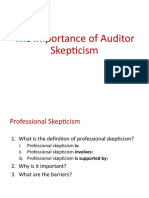

- Article On Professional ScepticismDocument7 pagesArticle On Professional ScepticismSaksham KhuranaNo ratings yet

- Informe de Ingles de Aditoria Financiera - Es.enDocument8 pagesInforme de Ingles de Aditoria Financiera - Es.enLESLIE ANETTE AREVALO FLORESNo ratings yet

- Explain Meaning of Professional Judgement and Professional Skepticism Professional Judgement and Professional SkepticismDocument3 pagesExplain Meaning of Professional Judgement and Professional Skepticism Professional Judgement and Professional SkepticismLinh Nguyễn KhánhNo ratings yet

- Auditing US Gaap InformationDocument16 pagesAuditing US Gaap InformationAna SalNo ratings yet

- ACC802 Topic 2:: Auditor Duties and ResponsibilitiesDocument40 pagesACC802 Topic 2:: Auditor Duties and ResponsibilitiesRamiza KhatoonNo ratings yet

- Response Apb DP Auditor Scepticism October 2010Document12 pagesResponse Apb DP Auditor Scepticism October 2010Nasir ArifNo ratings yet

- Audit Mid NotesDocument6 pagesAudit Mid Noteshadi shaikhNo ratings yet

- PSA 120 - Reflection PaperDocument2 pagesPSA 120 - Reflection PaperNicole Bait-itNo ratings yet

- Acctg 14.1Document13 pagesAcctg 14.1arman dela cruzNo ratings yet

- 50 - Auditing and Accounting StandardsDocument12 pages50 - Auditing and Accounting Standardsindu_prasad_1No ratings yet

- Standards On Auditing and Its Usage in AuditingDocument5 pagesStandards On Auditing and Its Usage in Auditingbhagaban_fm8098No ratings yet

- Audit Theory Chapter 7 Overview of FS Audit ProcessDocument13 pagesAudit Theory Chapter 7 Overview of FS Audit ProcessAdam SmithNo ratings yet

- Chapter 1Document17 pagesChapter 1RahulNo ratings yet

- Introduction SlideDocument7 pagesIntroduction SlideELLEN MUDZVITINo ratings yet

- Standards of AuditingDocument86 pagesStandards of Auditingmaulesh bhattNo ratings yet

- Standards by Sanidhya Saraf Serial 1 5Document85 pagesStandards by Sanidhya Saraf Serial 1 5rahul gobburiNo ratings yet

- Acca Code of Ethics (Notes)Document16 pagesAcca Code of Ethics (Notes)nurmaisarahnurazim1No ratings yet

- Shubam KeswaniDocument175 pagesShubam KeswaniDhruv GolyanNo ratings yet

- Bacc307 Assignment 1Document7 pagesBacc307 Assignment 1Denny ChakauyaNo ratings yet

- 1 Overview of The Risk Based Audit ProcessDocument7 pages1 Overview of The Risk Based Audit ProcessJohn Carl BlancaflorNo ratings yet

- Module 001 Overview of The Risk-Based AuditDocument12 pagesModule 001 Overview of The Risk-Based AuditCherwin bentulan100% (1)

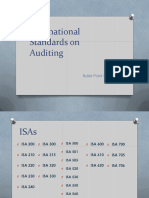

- Isa 200Document17 pagesIsa 200Mirza Ehsan Ullah MughalNo ratings yet

- Module 1 Overview of The Audit ProcessDocument7 pagesModule 1 Overview of The Audit ProcessJeane Bongalan100% (2)

- Audit 1 - Exercise W2 - AnsDocument2 pagesAudit 1 - Exercise W2 - AnsSyahirah RashidNo ratings yet

- Auditing Concepts: 1. Professional SkepticismDocument8 pagesAuditing Concepts: 1. Professional SkepticismPhebieon MukwenhaNo ratings yet

- Chapter 6 Risk Assessment (PART 1)Document9 pagesChapter 6 Risk Assessment (PART 1)Aravinthan INSAF SmartClassNo ratings yet

- Auditing Standards Summary DK-Dheeraj KukrejaDocument16 pagesAuditing Standards Summary DK-Dheeraj KukrejaRajavati NadarNo ratings yet

- PSA 120 and PSA 200Document26 pagesPSA 120 and PSA 200Anna CastroNo ratings yet

- Isa 200Document3 pagesIsa 200divakarareddyNo ratings yet

- Summary of SADocument22 pagesSummary of SAEkansh GargNo ratings yet

- Lesson 3 Financial Statements AuditDocument5 pagesLesson 3 Financial Statements AuditMark TaysonNo ratings yet

- Sa 200Document4 pagesSa 200Flying fishNo ratings yet

- Auditor Considerations SIGNIFICANT UNUSUAL COMPLEX TRANSACTIONSDocument8 pagesAuditor Considerations SIGNIFICANT UNUSUAL COMPLEX TRANSACTIONSramachandran_ca8060No ratings yet

- Lesson 3Document31 pagesLesson 3Aldrin DagamiNo ratings yet

- Auditing Auditing Report Cabral and de JesusDocument43 pagesAuditing Auditing Report Cabral and de JesusLalaine De JesusNo ratings yet

- Auditor's Opinion and Report, Materiality, Missatement & FraudDocument6 pagesAuditor's Opinion and Report, Materiality, Missatement & Fraudgimata kochomataNo ratings yet

- Revision of ISA's and Audit ReportDocument30 pagesRevision of ISA's and Audit ReportZakariya ZuberiNo ratings yet

- ACCO 30043 Assignment No.3Document8 pagesACCO 30043 Assignment No.3RoseanneNo ratings yet

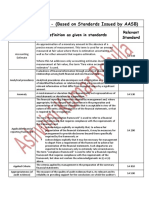

- Audit Dictionary - (Based On Standards Issued by AASB) : Definition As Given in Standards Relevant StandardDocument15 pagesAudit Dictionary - (Based On Standards Issued by AASB) : Definition As Given in Standards Relevant Standardshubham KumarNo ratings yet

- Psa 120-200Document2 pagesPsa 120-200Hannah FigueroaNo ratings yet

- Adv. Aud. CH 6 Auditor Resp.Document5 pagesAdv. Aud. CH 6 Auditor Resp.HagarMahmoudNo ratings yet

- Accounting 16aDocument93 pagesAccounting 16aLelouch BritanianNo ratings yet

- The Audit of Related Parties and The Application of Professional SkepticismDocument18 pagesThe Audit of Related Parties and The Application of Professional SkepticismTamirat Eshetu WoldeNo ratings yet

- Standards On AuditingDocument37 pagesStandards On AuditingAryan ShaikhNo ratings yet

- All ISADocument30 pagesAll ISANTurin1435No ratings yet

- ISA Bullet Points For D11Document24 pagesISA Bullet Points For D11Muzamil RaoNo ratings yet

- Lecture 2 Professional Skepticism Judgement and Judgement BiasDocument37 pagesLecture 2 Professional Skepticism Judgement and Judgement BiasNabila SedkiNo ratings yet

- Superior University: Advance Auditing Mid AssignmentDocument34 pagesSuperior University: Advance Auditing Mid AssignmentMirza Ehsan Ullah MughalNo ratings yet

- Impartiality: ISO 9001 Auditing Practices Group Guidance OnDocument6 pagesImpartiality: ISO 9001 Auditing Practices Group Guidance OnGa Ce J ManuelNo ratings yet

- Jurnal Business Padlah Riyadi. 2023Document10 pagesJurnal Business Padlah Riyadi. 2023Padlah Riyadi. SE., Ak., CA., MM.No ratings yet

- C9ay1 HsijbDocument15 pagesC9ay1 HsijbEyob FirstNo ratings yet

- Professional Skepticism 2Document10 pagesProfessional Skepticism 2kedir mohamedNo ratings yet

- My Audit NotesDocument52 pagesMy Audit NotesGurpreet SinghNo ratings yet

- Ethics & Terms of Audit EngagementDocument8 pagesEthics & Terms of Audit Engagementbroabhi143No ratings yet

- Q 4Document3 pagesQ 4kate bautistaNo ratings yet

- Bautista Kate Final Exam-IbtDocument1 pageBautista Kate Final Exam-Ibtkate bautistaNo ratings yet

- Government Rank and File Employee Summary of Compensation and Benefits in 2020Document4 pagesGovernment Rank and File Employee Summary of Compensation and Benefits in 2020kate bautistaNo ratings yet

- My Topic Is About Partnership. PartnershipDocument4 pagesMy Topic Is About Partnership. Partnershipkate bautistaNo ratings yet

- Report That Limits Its Use To Those Users or ThatDocument7 pagesReport That Limits Its Use To Those Users or Thatkate bautistaNo ratings yet

- Overview of Elements of The Financial Report Audit Process: Learning ObjectivesDocument24 pagesOverview of Elements of The Financial Report Audit Process: Learning Objectiveskate bautistaNo ratings yet

- Case StudyDocument1 pageCase Studykate bautistaNo ratings yet

- Case StudyDocument1 pageCase Studykate bautistaNo ratings yet