You might also like

- Bkm9e Answers Chap009Document9 pagesBkm9e Answers Chap009AhmadYaseenNo ratings yet

- Chapter 6: Risk Aversion and Capital Allocation To Risky AssetsDocument14 pagesChapter 6: Risk Aversion and Capital Allocation To Risky AssetsBiloni KadakiaNo ratings yet

- RR Problems SolutionsDocument5 pagesRR Problems SolutionsShaikh FarazNo ratings yet

- Basic: Problem SetsDocument4 pagesBasic: Problem SetspinoNo ratings yet

- Risk and Return Practice QuestionsDocument6 pagesRisk and Return Practice QuestionsPavanNo ratings yet

- Return and RiskDocument20 pagesReturn and Riskdkriray100% (1)

- Chap 7 End of Chap SolDocument13 pagesChap 7 End of Chap SolWan Chee100% (1)

- FNCE 30001 Week 12 Portfolio Performance EvaluationDocument83 pagesFNCE 30001 Week 12 Portfolio Performance EvaluationVrtpy Ciurban100% (1)

- INDEX MODELS CHAPTERDocument9 pagesINDEX MODELS CHAPTERzyNo ratings yet

- Bkm9e Answers Chap006Document13 pagesBkm9e Answers Chap006AhmadYaseenNo ratings yet

- BKM CH 06 Answers W CFADocument11 pagesBKM CH 06 Answers W CFAAhmed Bashir100% (19)

- Practice Questions Risk and ReturnsDocument6 pagesPractice Questions Risk and ReturnsMuhammad YahyaNo ratings yet

- BKM CH 06 Answers W CFADocument11 pagesBKM CH 06 Answers W CFAKyThoaiNo ratings yet

- Tutorial 4 CHP 5 - SolutionDocument6 pagesTutorial 4 CHP 5 - SolutionwilliamnyxNo ratings yet

- FIN604 MID - Farhan Zubair - 18164052Document7 pagesFIN604 MID - Farhan Zubair - 18164052ZNo ratings yet

- Risk and Return: Models Linking Risk and Expected ReturnDocument10 pagesRisk and Return: Models Linking Risk and Expected ReturnadafgsdfgNo ratings yet

- Min-Variance Portfolio & Optimal Risky PortfolioDocument4 pagesMin-Variance Portfolio & Optimal Risky PortfolioHelen B. EvansNo ratings yet

- CAPM Assignment (Risk, Return & CAPMDocument5 pagesCAPM Assignment (Risk, Return & CAPMnikhilchatNo ratings yet

- Study Questions Risk and ReturnDocument4 pagesStudy Questions Risk and ReturnAlif SultanliNo ratings yet

- Dividend Decisions Explained Through MM Model ExamplesDocument3 pagesDividend Decisions Explained Through MM Model Examplesjdon50% (2)

- CF - Questions and Practice Problems - Chapter 15Document3 pagesCF - Questions and Practice Problems - Chapter 15Lê Hoàng Long NguyễnNo ratings yet

- Chapter 5: Introduction To Risk, Return, and The Historical RecordDocument7 pagesChapter 5: Introduction To Risk, Return, and The Historical RecordBiloni KadakiaNo ratings yet

- Lecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelDocument34 pagesLecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelL SNo ratings yet

- The Mock Test2923Document15 pagesThe Mock Test2923elongoria278No ratings yet

- Chapter 17 Solutions BKM Investments 9eDocument11 pagesChapter 17 Solutions BKM Investments 9enpiper29100% (1)

- Solutions Class Examples AFM2015Document36 pagesSolutions Class Examples AFM2015SherelleJiaxinLiNo ratings yet

- Capital Asset Pricing Theory and Arbitrage Pricing TheoryDocument19 pagesCapital Asset Pricing Theory and Arbitrage Pricing TheoryMohammed ShafiNo ratings yet

- Investment Analysis and Portfolio MGT - Question With SolutionDocument10 pagesInvestment Analysis and Portfolio MGT - Question With SolutionFagbola Oluwatobi OmolajaNo ratings yet

- Arbitrage Pricing TheoryDocument4 pagesArbitrage Pricing TheoryShabbir NadafNo ratings yet

- Combinepdf PDFDocument65 pagesCombinepdf PDFCam SpaNo ratings yet

- PracticeQuestion CH 6&8Document13 pagesPracticeQuestion CH 6&8putinNo ratings yet

- BKM 10e Chap013Document18 pagesBKM 10e Chap013jl123123No ratings yet

- Chapter 8: Index Models: Problem SetsDocument14 pagesChapter 8: Index Models: Problem SetsAlyse97No ratings yet

- Lecture-20 Equity ValuationDocument10 pagesLecture-20 Equity ValuationSumit Kumar GuptaNo ratings yet

- BKM Chapter14Document5 pagesBKM Chapter14Vishakha DarbariNo ratings yet

- Optimal Risky Portfolios MCQsDocument62 pagesOptimal Risky Portfolios MCQsJerine TanNo ratings yet

- Risk and Return: 1. Chapter 11 (Textbook) : 7, 13, 14, 24Document3 pagesRisk and Return: 1. Chapter 11 (Textbook) : 7, 13, 14, 24anon_355962815100% (1)

- Cost 2021-MayDocument8 pagesCost 2021-MayDAVID I MUSHINo ratings yet

- Ross 9e FCF SMLDocument425 pagesRoss 9e FCF SMLAlmayayaNo ratings yet

- Binary Dependent Variable Multiple ChoiceDocument3 pagesBinary Dependent Variable Multiple ChoiceGary AshcroftNo ratings yet

- CH 14Document9 pagesCH 14Pola PolzNo ratings yet

- Risk and ReturnDocument3 pagesRisk and ReturnPiyush RathiNo ratings yet

- Multiple Choice Questions Please Circle The Correct Answer There Is Only One Correct Answer Per QuestionDocument39 pagesMultiple Choice Questions Please Circle The Correct Answer There Is Only One Correct Answer Per Questionquickreader12No ratings yet

- Chapter 03Document80 pagesChapter 03raiNo ratings yet

- Fin-450 CH 13 QUIZDocument7 pagesFin-450 CH 13 QUIZNick Rydal JensenNo ratings yet

- Cfa Chapter 9 Problems: The Capital Asset Pricing ModelDocument7 pagesCfa Chapter 9 Problems: The Capital Asset Pricing ModelFagbola Oluwatobi Omolaja100% (1)

- Investment BKM 5th EditonDocument21 pagesInvestment BKM 5th EditonKonstantin BezuhanovNo ratings yet

- Chapter 14 - HW With SolutionsDocument6 pagesChapter 14 - HW With Solutionsa882906100% (1)

- Payout Policy: File, Then Send That File Back To Google Classwork - Assignment by Due Date & Due Time!Document4 pagesPayout Policy: File, Then Send That File Back To Google Classwork - Assignment by Due Date & Due Time!Gian RandangNo ratings yet

- Portfolio Management Handout 1 - Questions PDFDocument6 pagesPortfolio Management Handout 1 - Questions PDFPriyankaNo ratings yet

- A 109 SMDocument39 pagesA 109 SMRam Krishna KrishNo ratings yet

- FINMATHS Assignment2Document15 pagesFINMATHS Assignment2Wei Wen100% (1)

- APT+exercises+post 1Document6 pagesAPT+exercises+post 1Karan GambhirNo ratings yet

- Prob 14Document6 pagesProb 14LaxminarayanaMurthyNo ratings yet

- Homework 5 SolutionDocument3 pagesHomework 5 SolutionalstonetNo ratings yet

- Chapter 11Document7 pagesChapter 11NguyenThiTuOanhNo ratings yet

- Tutorial 5 - SolutionsDocument8 pagesTutorial 5 - SolutionsHa PhiNo ratings yet

- PS 2Document6 pagesPS 2WristWork EntertainmentNo ratings yet

- Investments Canadian Canadian 8th Edition Bodie Solutions ManualDocument9 pagesInvestments Canadian Canadian 8th Edition Bodie Solutions ManualSherryWalkeryxog100% (33)

- Proforma Mahindra TeqoDocument1 pageProforma Mahindra Teqop m yadavNo ratings yet

- Executive SummaryDocument45 pagesExecutive SummarymaachudaapniNo ratings yet

- Bintang Persada Hotel Breakfast CouponDocument4 pagesBintang Persada Hotel Breakfast CouponPutu BudaNo ratings yet

- Citibank SingaporeDocument8 pagesCitibank SingaporeYudis TiawanNo ratings yet

- Far410 (Jan 2018)Document8 pagesFar410 (Jan 2018)nurathirahNo ratings yet

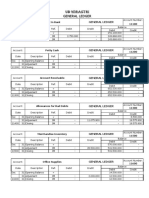

- General Ledger After ClosingDocument8 pagesGeneral Ledger After ClosingYOHANANo ratings yet

- Role and Functions of RBI: HistoryDocument9 pagesRole and Functions of RBI: HistorydimpledeepaNo ratings yet

- Case FriaDocument7 pagesCase FriaMichelle Marie TablizoNo ratings yet

- Dela Paz Vs L & J Development CompanyDocument2 pagesDela Paz Vs L & J Development CompanyMia AdlawanNo ratings yet

- Investasi Sementara Pada ObligasiDocument34 pagesInvestasi Sementara Pada ObligasiAli-ImronNo ratings yet

- Study of National Pension SchemeDocument27 pagesStudy of National Pension SchemeYashpal ThakurNo ratings yet

- Sox PDFDocument8 pagesSox PDFRoland ValNo ratings yet

- Group8 - ReportDocument27 pagesGroup8 - ReportAgastin kNo ratings yet

- Goldman Sachs-opinion-The Procter & Gamble CompanyDocument37 pagesGoldman Sachs-opinion-The Procter & Gamble CompanyUnnikrishnan SNo ratings yet

- 1.1 - Industry Profile: Chapter - 1Document75 pages1.1 - Industry Profile: Chapter - 1Deekshith NNo ratings yet

- Pepsi Killing SoftlyDocument32 pagesPepsi Killing SoftlyVamsi ReddyNo ratings yet

- Republic Vs Mambulao Lumber - CDDocument1 pageRepublic Vs Mambulao Lumber - CDmenforeverNo ratings yet

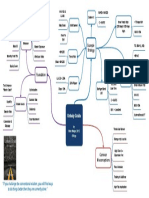

- #6. Unholy Grails by Nick Radge, 2012 - 224 PGDocument1 page#6. Unholy Grails by Nick Radge, 2012 - 224 PGpatar greatNo ratings yet

- NudobulojapDocument2 pagesNudobulojapDevamNo ratings yet

- Philippine First Insurance CompanyDocument2 pagesPhilippine First Insurance CompanyRoda May DiñoNo ratings yet

- KPMG Semiconductor Outlook 2018 Web PDFDocument24 pagesKPMG Semiconductor Outlook 2018 Web PDFDavid MorganNo ratings yet

- Quizzer - Buscom 01Document7 pagesQuizzer - Buscom 01khyla Marie NooraNo ratings yet

- Po 3000033325Document2 pagesPo 3000033325Berlin GohNo ratings yet

- Structure ProblemsDocument3 pagesStructure ProblemsHaider SyedNo ratings yet

- Annual ReportDocument88 pagesAnnual ReportAbhishek KumarNo ratings yet

- (Intermediate Accounting 1A) : Lecture AidDocument13 pages(Intermediate Accounting 1A) : Lecture AidShe RCNo ratings yet

- Collection Disbursement ReportDocument6 pagesCollection Disbursement Reportmkmohit991No ratings yet

- Study Guide Topic A: European CouncilDocument9 pagesStudy Guide Topic A: European CouncilAaqib ChaturbhaiNo ratings yet

- Can India Afford To Boycott Chinese ProductsDocument2 pagesCan India Afford To Boycott Chinese ProductsSowmya MinnuNo ratings yet