You might also like

- RMC 46-02Document4 pagesRMC 46-02matinikkiNo ratings yet

- ITAD Ruling 102-2002 May 28, 2002Document5 pagesITAD Ruling 102-2002 May 28, 2002Aine Mamle TeeNo ratings yet

- RMC 46-02Document2 pagesRMC 46-02saintkarriNo ratings yet

- 1999 ITAD RulingsDocument97 pages1999 ITAD RulingsJerwin DaveNo ratings yet

- Revenue Regulation Implementing RP-Singapore Tax TreatyDocument15 pagesRevenue Regulation Implementing RP-Singapore Tax Treatybianca.denise.dawisNo ratings yet

- Itad Bir Ruling No. 044-21Document9 pagesItad Bir Ruling No. 044-21Crizedhen VardeleonNo ratings yet

- $,upreme (!court: 3republtc of Tbe LlbtlipptnesDocument26 pages$,upreme (!court: 3republtc of Tbe LlbtlipptnesDianahAlcazarNo ratings yet

- Police Power PDFDocument150 pagesPolice Power PDFRenceNo ratings yet

- 3MPhils Vs CIRDocument3 pages3MPhils Vs CIRJDR JDRNo ratings yet

- Philippine Mining Act and FTAA Challenged in Didipio v GozunDocument5 pagesPhilippine Mining Act and FTAA Challenged in Didipio v GozunMarifel Lagare100% (1)

- Admin III Part 2 WordDocument22 pagesAdmin III Part 2 WordCGNo ratings yet

- Regulatory Framework and Legal Issues in BusinessDocument16 pagesRegulatory Framework and Legal Issues in BusinessKeneth Joe CabungcalNo ratings yet

- SC upholds constitutionality of Philippine Mining ActDocument7 pagesSC upholds constitutionality of Philippine Mining ActYe Seul DvngrcNo ratings yet

- INTELLECTUAL PROPERTY RIGHTSDocument21 pagesINTELLECTUAL PROPERTY RIGHTSshelNo ratings yet

- Taxation Fulltxt-2nd BatchDocument68 pagesTaxation Fulltxt-2nd BatchNovie AmorNo ratings yet

- Tio v. VideogR. No. L-75697, June 18, 1987.Document5 pagesTio v. VideogR. No. L-75697, June 18, 1987.Emerson NunezNo ratings yet

- G.R. No. L-44007 CaseDocument8 pagesG.R. No. L-44007 CaseAntonio Reyes IVNo ratings yet

- Case 10 La Bugal-BLaan v. Ramos, G.R. No. 127882 Dec. 01, 2004 - SummaryDocument7 pagesCase 10 La Bugal-BLaan v. Ramos, G.R. No. 127882 Dec. 01, 2004 - Summaryblude cosingNo ratings yet

- Bir Itad Ruling 73-03Document3 pagesBir Itad Ruling 73-03restless11No ratings yet

- Nelson Y. NG For Petitioner. The City Legal Officer For Respondents City Mayor and City TreasurerDocument11 pagesNelson Y. NG For Petitioner. The City Legal Officer For Respondents City Mayor and City TreasurerdingNo ratings yet

- BIT PhBangladeshDocument10 pagesBIT PhBangladeshNaim SubaNo ratings yet

- Facts:: 1. Fisher vs. Trinidad G.R. No. L-17518, October 30, 1922Document10 pagesFacts:: 1. Fisher vs. Trinidad G.R. No. L-17518, October 30, 1922Kaemy MalloNo ratings yet

- Sec-Ogc Opinion No. 16-18: Rodrigo Berenguer & GunoDocument4 pagesSec-Ogc Opinion No. 16-18: Rodrigo Berenguer & GunoAngeli PayongayongNo ratings yet

- Income Tax Case DigestDocument8 pagesIncome Tax Case DigestFrancisCzeasarChuaNo ratings yet

- Tio vs. Videogram Regulatory BoardDocument5 pagesTio vs. Videogram Regulatory BoardMay Marie Ann Aragon-Jimenez WESTERN MINDANAO STATE UNIVERSITY, COLLEGE OF LAWNo ratings yet

- Nelson Y. NG For Petitioner. The City Legal Officer For Respondents City Mayor and City TreasurerDocument7 pagesNelson Y. NG For Petitioner. The City Legal Officer For Respondents City Mayor and City TreasurerLeslie LernerNo ratings yet

- Court of Tax Appeals: DecisionDocument40 pagesCourt of Tax Appeals: DecisionNoznuagNo ratings yet

- TAXATION – DEFINITIONDocument147 pagesTAXATION – DEFINITIONGGT InteriorsNo ratings yet

- Cta 00 CV 03475 D 1987may20 Ass PDFDocument12 pagesCta 00 CV 03475 D 1987may20 Ass PDFjjbbrrNo ratings yet

- BIR Ruling ECCP 068-08Document4 pagesBIR Ruling ECCP 068-08Kendra Miranda LorinNo ratings yet

- Republic of The Philippines Vs CAGUIOADocument14 pagesRepublic of The Philippines Vs CAGUIOAAnonymous NWnRYIWNo ratings yet

- Intellectual property rights for foreign nationals and local lawsDocument15 pagesIntellectual property rights for foreign nationals and local lawsRikka ReyesNo ratings yet

- Cta 2D CV 10059 D 2023apr26 AssDocument47 pagesCta 2D CV 10059 D 2023apr26 AssFirenze PHNo ratings yet

- E.4 Tio Vs Videogram Regulatory Board GR No. L-75697 06181987 PDFDocument4 pagesE.4 Tio Vs Videogram Regulatory Board GR No. L-75697 06181987 PDFbabyclaire17No ratings yet

- Air Canada vs. CIRDocument60 pagesAir Canada vs. CIRRhinnell RiveraNo ratings yet

- Paper Industries Corp v. CADocument3 pagesPaper Industries Corp v. CAPio MathayNo ratings yet

- CasesDocument226 pagesCasesNicole AnngelaNo ratings yet

- Tio vs. Videogram Regulatory Board, 151 SCRA 208Document5 pagesTio vs. Videogram Regulatory Board, 151 SCRA 208Chino Sison100% (1)

- CIR vs. CTA (G.R. No. L-44007 March 20, 1991) - 11Document12 pagesCIR vs. CTA (G.R. No. L-44007 March 20, 1991) - 11Amir Nazri KaibingNo ratings yet

- First Division: Court of Tax AppealsDocument23 pagesFirst Division: Court of Tax AppealsGeorge Mitchell S. GuerreroNo ratings yet

- II. Preliminary MattersDocument4 pagesII. Preliminary Matterssarah_reyes_13No ratings yet

- Consti - Tio Vs Videogram Regulatory BoardDocument6 pagesConsti - Tio Vs Videogram Regulatory BoardPaul Christian Balin CallejaNo ratings yet

- CIR vs. S. C. Johnson and Son, Inc. (G.R. No. 127105 June 25, 1999) - H DIGESTDocument3 pagesCIR vs. S. C. Johnson and Son, Inc. (G.R. No. 127105 June 25, 1999) - H DIGESTHarleneNo ratings yet

- Nelson Y. NG For Petitioner. The City Legal Officer For Respondents City Mayor and City TreasurerDocument17 pagesNelson Y. NG For Petitioner. The City Legal Officer For Respondents City Mayor and City TreasurerJacqueline AnnNo ratings yet

- Tio Vs Videogram Regulatory BoardDocument8 pagesTio Vs Videogram Regulatory BoardReaderTim5No ratings yet

- Itad Bir Ruling No. 065-05Document4 pagesItad Bir Ruling No. 065-05msdivergentNo ratings yet

- ITAD BIR Ruling No. 005-20Document6 pagesITAD BIR Ruling No. 005-20Paul Erik CaracasNo ratings yet

- NAPOCOR Franchise Tax Case Explains LGU Authority and Tax Exemption RepealDocument11 pagesNAPOCOR Franchise Tax Case Explains LGU Authority and Tax Exemption RepealRejean EscalonaNo ratings yet

- Paris Convention For Protection of Industrial Property Rights (Paris Convention)Document3 pagesParis Convention For Protection of Industrial Property Rights (Paris Convention)Lizzette Dela Pena100% (1)

- Ghana Investment Agreement ProtectionsDocument13 pagesGhana Investment Agreement ProtectionsTimore FrancisNo ratings yet

- WIPO Advisory Committee Discusses Philippine IP EnforcementDocument13 pagesWIPO Advisory Committee Discusses Philippine IP EnforcementisraeljamoraNo ratings yet

- Tio V VideogramDocument9 pagesTio V VideogramVan CazNo ratings yet

- Contract HtechcorpDocument3 pagesContract Htechcorpherkimer.lightNo ratings yet

- Kepco v. CIRDocument8 pagesKepco v. CIRKhian JamerNo ratings yet

- Commissioner of Internal Revenue vs. S.C. Johnson and Sons, Inc. (G.R. No. 127105, June 25, 1999)Document2 pagesCommissioner of Internal Revenue vs. S.C. Johnson and Sons, Inc. (G.R. No. 127105, June 25, 1999)Jennilyn Gulfan YaseNo ratings yet

- ITAD Ruling No. 065-05Document3 pagesITAD Ruling No. 065-05Anezka Danett CortinaNo ratings yet

- KIENERDocument14 pagesKIENERKIM KARBBY ROXASNo ratings yet

- Tax 1 Cases 2015 Page 1-2 SyllabusDocument177 pagesTax 1 Cases 2015 Page 1-2 SyllabusRichard BakerNo ratings yet

- Patent Laws of the Republic of Hawaii and Rules of Practice in the Patent OfficeFrom EverandPatent Laws of the Republic of Hawaii and Rules of Practice in the Patent OfficeNo ratings yet

- 3 - 2551442 - Salary - Illustration - 7 - 19 - 2022 9 - 16 - 28 PMDocument1 page3 - 2551442 - Salary - Illustration - 7 - 19 - 2022 9 - 16 - 28 PMShauryaNo ratings yet

- BIR Form No. 0901-S1Document2 pagesBIR Form No. 0901-S1Aldrinn BenamirNo ratings yet

- Nishat Ali Gulfam S/O M Shareef Old Kahna: Web Generated BillDocument1 pageNishat Ali Gulfam S/O M Shareef Old Kahna: Web Generated BillshahzadtecNo ratings yet

- City of Iloilo vs. Smart CommunicationsDocument2 pagesCity of Iloilo vs. Smart CommunicationsKim SimagalaNo ratings yet

- GST 7th Edition PDFDocument366 pagesGST 7th Edition PDFUtkarshNo ratings yet

- Consolidated Revenue Regulations on Cigarette, Heated Tobacco and Vapor ProductsDocument15 pagesConsolidated Revenue Regulations on Cigarette, Heated Tobacco and Vapor ProductsJeorge VerbaNo ratings yet

- Compensation Fact Sheet - Filled UpDocument2 pagesCompensation Fact Sheet - Filled UpEarl Jenn AbellaNo ratings yet

- Electronic Billing Machine (EBM)Document3 pagesElectronic Billing Machine (EBM)Habinshuti Jean claudeNo ratings yet

- !fusion Tax - CompleteDocument3 pages!fusion Tax - Completewaste wasteNo ratings yet

- TAX-303 (Input Taxes)Document7 pagesTAX-303 (Input Taxes)Princess ManaloNo ratings yet

- Amount claimed for work period May-Aug 2006Document3 pagesAmount claimed for work period May-Aug 2006anup jenaNo ratings yet

- Tax Rev SyllabusDocument14 pagesTax Rev SyllabusIanLightPajaroNo ratings yet

- Item Name HSN Code GST Rate QTY Taxable Rate Taxable ValueDocument4 pagesItem Name HSN Code GST Rate QTY Taxable Rate Taxable ValueAnup gurung100% (3)

- Income Taxation Solution Manual 2019 ED Income Taxation Solution Manual 2019 EDDocument40 pagesIncome Taxation Solution Manual 2019 ED Income Taxation Solution Manual 2019 EDSha Leen100% (2)

- 6 - Case Study - Microsoft and Its Foreign Cash Holdings PDFDocument2 pages6 - Case Study - Microsoft and Its Foreign Cash Holdings PDFAhmerNo ratings yet

- Value Added TaxDocument3 pagesValue Added TaxChristine Igna100% (1)

- Bargarh Handloom and Agro Producer CompanyDocument2 pagesBargarh Handloom and Agro Producer CompanyOrmas OdishaNo ratings yet

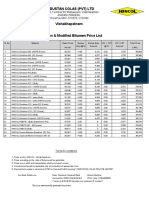

- HINDUSTAN COLAS Emulsion & Modified Bitumen Price ListDocument2 pagesHINDUSTAN COLAS Emulsion & Modified Bitumen Price ListRama Raju Gottumukkala0% (1)

- Revenue Dept PIO and Appellate Authority ContactDocument7 pagesRevenue Dept PIO and Appellate Authority Contactarulraj_ponnusamyNo ratings yet

- Liability of JDA entered prior to GST when SA is entered post GSTDocument3 pagesLiability of JDA entered prior to GST when SA is entered post GSTKunalKumarNo ratings yet

- 2014-15 Douglas County Secured Assessment RollDocument97 pages2014-15 Douglas County Secured Assessment RollcvalleytimesNo ratings yet

- Amazon Accounting 101Document11 pagesAmazon Accounting 101Acsaran Sangcad ObinayNo ratings yet

- Sales Plan Template 12Document17 pagesSales Plan Template 12Rocky LeroyNo ratings yet

- On January 1 2015 Evers Company Purchased The Following Two: Unlock Answers Here Solutiondone - OnlineDocument1 pageOn January 1 2015 Evers Company Purchased The Following Two: Unlock Answers Here Solutiondone - OnlineAmit PandeyNo ratings yet

- Monopoly Journal Entries Year 2Document2 pagesMonopoly Journal Entries Year 2AshliNo ratings yet

- Special Power of Attorney TitleDocument1 pageSpecial Power of Attorney TitleJo Therese Francisco TiuNo ratings yet

- Flaws of GST Bill Exposed in Strong ArgumentDocument3 pagesFlaws of GST Bill Exposed in Strong ArgumentKshitij Gaur100% (3)

- KINDS OF TAXPAYERS AND SITUS OF INCOMEDocument2 pagesKINDS OF TAXPAYERS AND SITUS OF INCOMEMelanie SamsonaNo ratings yet

- Value Added Tax NotesDocument12 pagesValue Added Tax NotesAimeeNo ratings yet