You might also like

- Investing for Beginners 2024: How to Achieve Financial Freedom and Grow Your Wealth Through Real Estate, The Stock Market, Cryptocurrency, Index Funds, Rental Property, Options Trading, and More.From EverandInvesting for Beginners 2024: How to Achieve Financial Freedom and Grow Your Wealth Through Real Estate, The Stock Market, Cryptocurrency, Index Funds, Rental Property, Options Trading, and More.Rating: 5 out of 5 stars5/5 (89)

- Introduction to Index Funds and ETF's - Passive Investing for BeginnersFrom EverandIntroduction to Index Funds and ETF's - Passive Investing for BeginnersRating: 4.5 out of 5 stars4.5/5 (7)

- How to Make Money While You Sleep (Beginner Guide to Investment)From EverandHow to Make Money While You Sleep (Beginner Guide to Investment)No ratings yet

- How To Begin Investing In The Stock Market: Obtaining Financial FreedomFrom EverandHow To Begin Investing In The Stock Market: Obtaining Financial FreedomNo ratings yet

- Investing In Stock Market For Beginners: understanding the basics of how to make money with stocksFrom EverandInvesting In Stock Market For Beginners: understanding the basics of how to make money with stocksRating: 4 out of 5 stars4/5 (13)

- Stock Market Investing for Beginners: 7 Steps to Learn How You Can Create Financial Freedom Through Stock Investing, With These Golden Nuggets!From EverandStock Market Investing for Beginners: 7 Steps to Learn How You Can Create Financial Freedom Through Stock Investing, With These Golden Nuggets!Rating: 4.5 out of 5 stars4.5/5 (2)

- Construct Your Own Wealth: A Guide to Making Profit From The Stock MarketFrom EverandConstruct Your Own Wealth: A Guide to Making Profit From The Stock MarketNo ratings yet

- A BEGINNER’S BASIC GUIDE TO STOCK MARKET INVESTING: UNDERSTANDING THE BIG PICTURE: The Investing Series, #1From EverandA BEGINNER’S BASIC GUIDE TO STOCK MARKET INVESTING: UNDERSTANDING THE BIG PICTURE: The Investing Series, #1Rating: 3.5 out of 5 stars3.5/5 (3)

- A Beginners’s Basic Guide to Stock Market Investing: Understanding The Big PictureFrom EverandA Beginners’s Basic Guide to Stock Market Investing: Understanding The Big PictureRating: 4 out of 5 stars4/5 (1)

- Stock Market Investing for Beginners: How to Build Wealth and Achieve Financial Freedom with a Diversified Portfolio Using Index Funds, Technical Analysis, Options, Penny Stocks, Dividends, and REITS.From EverandStock Market Investing for Beginners: How to Build Wealth and Achieve Financial Freedom with a Diversified Portfolio Using Index Funds, Technical Analysis, Options, Penny Stocks, Dividends, and REITS.Rating: 5 out of 5 stars5/5 (54)

- Investing For Beginners: Introduction to Investing, #1From EverandInvesting For Beginners: Introduction to Investing, #1Rating: 4 out of 5 stars4/5 (6)

- The Everything Guide to Investing in Your 20s & 30s: Your Step-by-Step Guide to: * Understanding Stocks, Bonds, and Mutual Funds * Maximizing Your 401(k) * Setting Realistic Goals * Recognizing the Risks and Rewards of Cryptocurrencies * Minimizing Your Investment Tax LiabilityFrom EverandThe Everything Guide to Investing in Your 20s & 30s: Your Step-by-Step Guide to: * Understanding Stocks, Bonds, and Mutual Funds * Maximizing Your 401(k) * Setting Realistic Goals * Recognizing the Risks and Rewards of Cryptocurrencies * Minimizing Your Investment Tax LiabilityNo ratings yet

- The How To Book on Dividend Growth Investing: Create Generational Wealth and Passive Income for Life!From EverandThe How To Book on Dividend Growth Investing: Create Generational Wealth and Passive Income for Life!No ratings yet

- Investing Made Simple - Warren Buffet Strategies To Building Wealth And Creating Passive IncomeFrom EverandInvesting Made Simple - Warren Buffet Strategies To Building Wealth And Creating Passive IncomeNo ratings yet

- Value Investing: A Comprehensive Beginner Investor's Guide to Finding Undervalued Stock, Value Investing Strategy and Risk ManagementFrom EverandValue Investing: A Comprehensive Beginner Investor's Guide to Finding Undervalued Stock, Value Investing Strategy and Risk ManagementNo ratings yet

- Market Secrets: Step-By-Step Guide to Develop Your Financial Freedom - Best Stock Trading Strategies, Complete Explanations, Tips and Finished InstructionsFrom EverandMarket Secrets: Step-By-Step Guide to Develop Your Financial Freedom - Best Stock Trading Strategies, Complete Explanations, Tips and Finished InstructionsNo ratings yet

- Millionaires Simple Guide to Big Money and Wealth Building For BeginnersFrom EverandMillionaires Simple Guide to Big Money and Wealth Building For BeginnersNo ratings yet

- Investing Made Simple: Strategies for Building a Profitable Investment Portfolio through Real Estate, Stocks, Options Trading, Index Funds, Bonds, REITs, Bitcoin, and Beyond.From EverandInvesting Made Simple: Strategies for Building a Profitable Investment Portfolio through Real Estate, Stocks, Options Trading, Index Funds, Bonds, REITs, Bitcoin, and Beyond.Rating: 5 out of 5 stars5/5 (57)

- Stock Market Simplified: A Beginner's Guide to Investing Stocks, Growing Your Money and Securing Your Financial Future: Personal Finance and Stock Investment StrategiesFrom EverandStock Market Simplified: A Beginner's Guide to Investing Stocks, Growing Your Money and Securing Your Financial Future: Personal Finance and Stock Investment StrategiesRating: 5 out of 5 stars5/5 (1)

- Don't Invest and Forget: A Look at the Importance of Having a Comprehensive, Dynamic Investment PlanFrom EverandDon't Invest and Forget: A Look at the Importance of Having a Comprehensive, Dynamic Investment PlanNo ratings yet

- Dividend Investing: The Ultimate Guide to Create Passive Income Using Stocks. Make Money Online, Gain Financial Freedom and Retire Early Earning Double-Digit ReturnsFrom EverandDividend Investing: The Ultimate Guide to Create Passive Income Using Stocks. Make Money Online, Gain Financial Freedom and Retire Early Earning Double-Digit ReturnsNo ratings yet

- Dividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.From EverandDividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.No ratings yet

- Investing 101: From Stocks and Bonds to ETFs and IPOs, an Essential Primer on Building a Profitable PortfolioFrom EverandInvesting 101: From Stocks and Bonds to ETFs and IPOs, an Essential Primer on Building a Profitable PortfolioRating: 4.5 out of 5 stars4.5/5 (38)

- Dividend Investing for Beginners: How to Build Your Investment Strategy, Find The Best Dividend Stocks to Buy, and Generate Passive Income: Investing for Beginners, #1From EverandDividend Investing for Beginners: How to Build Your Investment Strategy, Find The Best Dividend Stocks to Buy, and Generate Passive Income: Investing for Beginners, #1No ratings yet

- Investing for Beginners: Minimize Risk, Maximize Returns, Grow Your Wealth, and Achieve Financial Freedom Through The Stock Market, Index Funds, Options Trading, Cryptocurrency, Real Estate, and More.From EverandInvesting for Beginners: Minimize Risk, Maximize Returns, Grow Your Wealth, and Achieve Financial Freedom Through The Stock Market, Index Funds, Options Trading, Cryptocurrency, Real Estate, and More.Rating: 5 out of 5 stars5/5 (49)

- Stock Market Investing for Beginners: Investing Tactics, Tools, Lessons, and Proven Strategies to Make Money by Investing & Trading Like Pro in the Stock Market for BeginnersFrom EverandStock Market Investing for Beginners: Investing Tactics, Tools, Lessons, and Proven Strategies to Make Money by Investing & Trading Like Pro in the Stock Market for BeginnersNo ratings yet

- Take On the Street (Review and Analysis of Levitt's Book)From EverandTake On the Street (Review and Analysis of Levitt's Book)No ratings yet

- At A Price Below Your Buying Price: SH Are Various Financial InstrumentsDocument7 pagesAt A Price Below Your Buying Price: SH Are Various Financial InstrumentsrahulsmankameNo ratings yet

- Basic Finance Eliza Mari L. Cabardo Ms. Alfe Solina BSHRM - 3A 07 Sept. 2012Document4 pagesBasic Finance Eliza Mari L. Cabardo Ms. Alfe Solina BSHRM - 3A 07 Sept. 2012cutiepattotieNo ratings yet

- Realistic Guide to Financial Freedom Through: Investing Activity. With step-by-step guide!: How to make millions with a simple investing strategy, part 1, #1From EverandRealistic Guide to Financial Freedom Through: Investing Activity. With step-by-step guide!: How to make millions with a simple investing strategy, part 1, #1No ratings yet

- Stock market investing for beginners 2022: A Simplified Beginner’s Guide To Starting Investing In The Stock Market And Achieve Your Financial FreedomFrom EverandStock market investing for beginners 2022: A Simplified Beginner’s Guide To Starting Investing In The Stock Market And Achieve Your Financial FreedomNo ratings yet

- Dividend Growth Investing: How to Build Future Income Streams Using Dividend AristocratsFrom EverandDividend Growth Investing: How to Build Future Income Streams Using Dividend AristocratsNo ratings yet

- Dividend Investing for Beginners: The Ultimate Guide to Double-Digit Your Returns. Learn How to Create Passive Income and Get One Step Closer to Your Financial Freedom.From EverandDividend Investing for Beginners: The Ultimate Guide to Double-Digit Your Returns. Learn How to Create Passive Income and Get One Step Closer to Your Financial Freedom.No ratings yet

- Muslim Investor: The Stock Market Made SimpleFrom EverandMuslim Investor: The Stock Market Made SimpleRating: 5 out of 5 stars5/5 (1)

- Stock Market Investing For Beginners - ANYONE Can Learn How To Trade Safely, Successfully, And Achieve Financial Stability: A Proven Guide For Beginners To Build A Risk-Free Passive IncomeFrom EverandStock Market Investing For Beginners - ANYONE Can Learn How To Trade Safely, Successfully, And Achieve Financial Stability: A Proven Guide For Beginners To Build A Risk-Free Passive IncomeNo ratings yet

- Dividend Investing for Beginners Learn the Basics to Generate Dividend Income from stock market: Stock Market for Beginners, #1From EverandDividend Investing for Beginners Learn the Basics to Generate Dividend Income from stock market: Stock Market for Beginners, #1Rating: 4 out of 5 stars4/5 (6)

- Investment and Portfolio ManagementDocument36 pagesInvestment and Portfolio ManagementMiguel MartinezNo ratings yet

- Dividend Investing I Complete Beginner’s Guide to Learn How to Create Passive Income by Trading Dividend Stocks I Start Achieving Financial Freedom and Planning Your Early RetirementFrom EverandDividend Investing I Complete Beginner’s Guide to Learn How to Create Passive Income by Trading Dividend Stocks I Start Achieving Financial Freedom and Planning Your Early RetirementNo ratings yet

- What Is Investing?: Stocks Bonds Mutual FundsDocument10 pagesWhat Is Investing?: Stocks Bonds Mutual Fundsarunchary007No ratings yet

- How To Make Money In Stocks Value Investing StrategiesFrom EverandHow To Make Money In Stocks Value Investing StrategiesNo ratings yet

- 3 Steps to Investment Success: How to Obtain the Returns, While Controlling RiskFrom Everand3 Steps to Investment Success: How to Obtain the Returns, While Controlling RiskNo ratings yet

- Canadian Mutual Funds Investing for Beginners: A Basic Guide for BeginnersFrom EverandCanadian Mutual Funds Investing for Beginners: A Basic Guide for BeginnersNo ratings yet

- Anxietysenstivity Er JADDocument12 pagesAnxietysenstivity Er JADAnonymous YkDJkSqNo ratings yet

- Spare A Thought For ParkinsonsDocument3 pagesSpare A Thought For ParkinsonsAnonymous YkDJkSqNo ratings yet

- Prediabetes: What To Know: Amy Campbell, MS, RD, LDN, CDE PrintDocument4 pagesPrediabetes: What To Know: Amy Campbell, MS, RD, LDN, CDE PrintAnonymous YkDJkSqNo ratings yet

- Key Ratios For Picking Good Stocks: 1. Ploughback and ReservesDocument6 pagesKey Ratios For Picking Good Stocks: 1. Ploughback and ReservesAnonymous YkDJkSqNo ratings yet

- Blood Sugar Chart: What's The Normal Range For Blood Sugar?: by - Published June 11, 2019Document5 pagesBlood Sugar Chart: What's The Normal Range For Blood Sugar?: by - Published June 11, 2019Anonymous YkDJkSqNo ratings yet

- Surface GrindingDocument6 pagesSurface GrindingAnonymous YkDJkSqNo ratings yet

- Industrial Engineering Question Bank for Comprehensive VivaDocument1 pageIndustrial Engineering Question Bank for Comprehensive VivaAnonymous YkDJkSqNo ratings yet

- QB For Comprehenive Viva-Voce - CAD - CAMDocument1 pageQB For Comprehenive Viva-Voce - CAD - CAMAnonymous YkDJkSqNo ratings yet

- Unit Built Machine ToolsDocument21 pagesUnit Built Machine ToolsAnonymous YkDJkSq100% (2)

- Objective Questions - CAD/CAM Unit - 3Document5 pagesObjective Questions - CAD/CAM Unit - 3Anonymous YkDJkSqNo ratings yet

- QB For First Mid - Objective-IEDocument4 pagesQB For First Mid - Objective-IEAnonymous YkDJkSqNo ratings yet

- QB For Mid2 - objective-IEDocument10 pagesQB For Mid2 - objective-IEAnonymous YkDJkSqNo ratings yet

- CAD/CAM - Objective Questions - Unit1Document2 pagesCAD/CAM - Objective Questions - Unit1Anonymous YkDJkSq100% (1)

- QB For Comprehenive Viva-Voce - DMM2Document1 pageQB For Comprehenive Viva-Voce - DMM2Anonymous YkDJkSqNo ratings yet

- 2-Marks Question Bank - Industrial Engineering - MID1 UNIT - 1Document1 page2-Marks Question Bank - Industrial Engineering - MID1 UNIT - 1Anonymous YkDJkSqNo ratings yet

- 2-Marks Question Bank - CAD/CAM - MID1 UNIT - 1Document2 pages2-Marks Question Bank - CAD/CAM - MID1 UNIT - 1Anonymous YkDJkSqNo ratings yet

- QB For First Mid - Objective-IEDocument4 pagesQB For First Mid - Objective-IEAnonymous YkDJkSqNo ratings yet

- Global Aspects of EntrepreneurshipDocument15 pagesGlobal Aspects of EntrepreneurshipAnonymous YkDJkSqNo ratings yet

- CNC Objective Question BankDocument2 pagesCNC Objective Question BankAnonymous YkDJkSq56% (9)

- CAD/CAM - Objective Questions - Unit2Document2 pagesCAD/CAM - Objective Questions - Unit2Anonymous YkDJkSqNo ratings yet

- MRP &JIT Objective Questions - Unit5Document1 pageMRP &JIT Objective Questions - Unit5Anonymous YkDJkSqNo ratings yet

- Basics of LubricationDocument10 pagesBasics of LubricationAnonymous YkDJkSq100% (1)

- Objective Questions - Group Technology & RoboticsDocument1 pageObjective Questions - Group Technology & RoboticsAnonymous YkDJkSqNo ratings yet

- Cutting Tool MaterialsDocument2 pagesCutting Tool MaterialsAnonymous YkDJkSqNo ratings yet

- Energy Systems - Bit Questions-Units 1 To 4Document2 pagesEnergy Systems - Bit Questions-Units 1 To 4Madan RaoNo ratings yet

- Global Aspects of EntrepreneurshipDocument15 pagesGlobal Aspects of EntrepreneurshipAnonymous YkDJkSqNo ratings yet

- Thermal PropertiesDocument1 pageThermal PropertiesAnonymous YkDJkSqNo ratings yet

- Robotics - PresentationDocument57 pagesRobotics - PresentationAnonymous YkDJkSqNo ratings yet

- Glossary of Spring TerminologyDocument4 pagesGlossary of Spring TerminologyGthulasi78No ratings yet

- Mfa Test 1Document4 pagesMfa Test 1Shantanu PorelNo ratings yet

- Estimating A Firm's Cost of Capital: Chapter 4 OutlineDocument17 pagesEstimating A Firm's Cost of Capital: Chapter 4 OutlineMohit KediaNo ratings yet

- Unit Viii - Audit of Equity Accounts T1 2014-2015 PDFDocument9 pagesUnit Viii - Audit of Equity Accounts T1 2014-2015 PDFSed ReyesNo ratings yet

- Tata Power Company: Capital StructureDocument5 pagesTata Power Company: Capital Structureharsh kotNo ratings yet

- IFRS for SMEs FAQsDocument5 pagesIFRS for SMEs FAQsMelicent FaithNo ratings yet

- 11.11.07 wp438Document41 pages11.11.07 wp438Thanhtam NhiNo ratings yet

- Capital Structure of Jindal Steel and PowerDocument2 pagesCapital Structure of Jindal Steel and PowerAshok VenkatNo ratings yet

- BVG Capital ExpenditureDocument15 pagesBVG Capital ExpenditureSeyton123No ratings yet

- Group 2 Written ReportDocument4 pagesGroup 2 Written Reportsharielles /No ratings yet

- Feasib Chapter 4Document9 pagesFeasib Chapter 4Red SecretarioNo ratings yet

- Tumelo Matjekane Finance 2009 RevisedDocument12 pagesTumelo Matjekane Finance 2009 RevisedMoatasemMadianNo ratings yet

- 1 To 4 Overview and Technical AnalysisDocument21 pages1 To 4 Overview and Technical AnalysisnomanNo ratings yet

- Name Full Company Name Legal Address E-Mail AddressDocument25 pagesName Full Company Name Legal Address E-Mail Addressmarketing lakshNo ratings yet

- JM Financial Asset Reconstruction Company Limited Corporate PresentationDocument28 pagesJM Financial Asset Reconstruction Company Limited Corporate PresentationbestdealsNo ratings yet

- Long-term investment analysisDocument13 pagesLong-term investment analysissamuel kebedeNo ratings yet

- Recommendation On The Acquisation of VitasoyDocument8 pagesRecommendation On The Acquisation of Vitasoyapi-237162505No ratings yet

- Birch Paper CompanyDocument1 pageBirch Paper CompanySwami R RNo ratings yet

- Analysis and Interpretation of Financial Statements: Christine Talimongan ABM - BezosDocument37 pagesAnalysis and Interpretation of Financial Statements: Christine Talimongan ABM - BezostineNo ratings yet

- MFF Convention Emphatic Accounts Live Funds Trading PayoutsDocument4 pagesMFF Convention Emphatic Accounts Live Funds Trading Payoutsmacosd4450No ratings yet

- Chapter Four - Books of Original EntryDocument5 pagesChapter Four - Books of Original EntryHezel GreationNo ratings yet

- Assignment QuestionsDocument12 pagesAssignment QuestionsyogendradilwalaNo ratings yet

- What-If Analysis TemplateDocument18 pagesWhat-If Analysis TemplateDardan DeskuNo ratings yet

- Leverage and Capital Structure SolutionsDocument10 pagesLeverage and Capital Structure SolutionsmaazNo ratings yet

- Dhan Ki BaatDocument12 pagesDhan Ki Baattest hrmNo ratings yet

- Sanskriti School Dr. S. Radhakrishnan Marg New DelhiDocument7 pagesSanskriti School Dr. S. Radhakrishnan Marg New DelhiAVNEET XII-CNo ratings yet

- Acctg 10 Midterm Lesson Part .1Document21 pagesAcctg 10 Midterm Lesson Part .1NANNo ratings yet

- Questions - Answers - Financial EngineeringDocument7 pagesQuestions - Answers - Financial EngineeringSidharth ChoudharyNo ratings yet

- Book BuildingDocument7 pagesBook BuildingshivathilakNo ratings yet

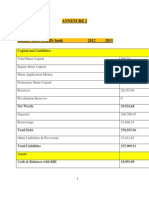

- Annexure 2Document13 pagesAnnexure 2Shalini SrivastavNo ratings yet

- Group Meeting 3Document6 pagesGroup Meeting 3Ve DekNo ratings yet