You might also like

- Unit 3 Cash ManagementDocument25 pagesUnit 3 Cash ManagementrehaarocksNo ratings yet

- FIN - Cash ManagementDocument24 pagesFIN - Cash Management29_ramesh170No ratings yet

- TextDocument2 pagesTextynsinojiaNo ratings yet

- Accounting FundamentalsDocument40 pagesAccounting Fundamentalsakon sanNo ratings yet

- What Is Cash Flow ForecastingDocument27 pagesWhat Is Cash Flow Forecastinggichana75peterNo ratings yet

- How To Take Charge of Your Farm's Financial Management: Terry Betker P.Ag., CAC, CMCDocument70 pagesHow To Take Charge of Your Farm's Financial Management: Terry Betker P.Ag., CAC, CMCTurner McKayNo ratings yet

- 05.02.2020, 1. S.srinivas Sir, Chartered Accountant, Accounting FundamentalsDocument40 pages05.02.2020, 1. S.srinivas Sir, Chartered Accountant, Accounting FundamentalsAradhana AndrewsNo ratings yet

- Accounting - Basics - Deloitte. 1Document56 pagesAccounting - Basics - Deloitte. 1Shubh100% (1)

- Cash Management by Group 9Document15 pagesCash Management by Group 9Noel GeorgeNo ratings yet

- Accounting FundamentalsDocument40 pagesAccounting FundamentalsPriyanka GoswamiNo ratings yet

- Weber - Cash Flow For CSO - ENDocument23 pagesWeber - Cash Flow For CSO - ENBranimir StefanovNo ratings yet

- Week 9: Introductory Accounting and The Balance Sheet: Public Health Accounting and Budgeting Lili Elkins-ThompsonDocument64 pagesWeek 9: Introductory Accounting and The Balance Sheet: Public Health Accounting and Budgeting Lili Elkins-Thompsons430230No ratings yet

- Methods of Accelarating Cash-InflowDocument23 pagesMethods of Accelarating Cash-InflowChannaveerayya Hiremath100% (1)

- Show Me Da Money!!!: Your Guide To Managing Personal Financial StatementsDocument32 pagesShow Me Da Money!!!: Your Guide To Managing Personal Financial StatementsStephen PommellsNo ratings yet

- Liquidity and Cash ManagementDocument9 pagesLiquidity and Cash ManagementSharath MenonNo ratings yet

- Management Information Systems: Books, Records & ControlsDocument35 pagesManagement Information Systems: Books, Records & ControlsParin ParekhNo ratings yet

- EFIN542 U12 T02 PowerPointDocument78 pagesEFIN542 U12 T02 PowerPointcustomsgyanNo ratings yet

- Nature of Cash & Cashflows Ma2Document12 pagesNature of Cash & Cashflows Ma2ali hansiNo ratings yet

- Cash Management: Reported By: Josephine P. JimenezDocument21 pagesCash Management: Reported By: Josephine P. JimenezPYNJIMENEZNo ratings yet

- Business 10 - Module 7Document5 pagesBusiness 10 - Module 7carrisanicole2No ratings yet

- Cash Management DemoDocument29 pagesCash Management DemoShakti ShivanandNo ratings yet

- Cash Management Chapter 11: Negative Cash Budget - A Period of Time When A Companies Disbursements ExceedDocument4 pagesCash Management Chapter 11: Negative Cash Budget - A Period of Time When A Companies Disbursements ExceedkeyyongparkNo ratings yet

- Cash ManagementDocument51 pagesCash ManagementDebasmita SahaNo ratings yet

- 23 - Cash Flow Forecasting and Working CapitalDocument29 pages23 - Cash Flow Forecasting and Working Capitalnader100% (1)

- Y12.U5.30 - Forecasting and Managing Cash FlowsDocument3 pagesY12.U5.30 - Forecasting and Managing Cash FlowsRuxandra ZahNo ratings yet

- RM U2 PPTDocument41 pagesRM U2 PPTPumba ConfessionNo ratings yet

- Working Capital Management: A PerspectiveDocument21 pagesWorking Capital Management: A PerspectiveSanthosh Philip GeorgeNo ratings yet

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- FM Cash ManagementDocument41 pagesFM Cash ManagementDimpol MagsalayNo ratings yet

- Summarized Topics in EntrepreneurshipDocument24 pagesSummarized Topics in EntrepreneurshipMarian AlfonsoNo ratings yet

- How To Make CVDocument3 pagesHow To Make CVnb34m1tNo ratings yet

- Accounting Basics Using Quickbooks: Presented by Mike KimutaiDocument17 pagesAccounting Basics Using Quickbooks: Presented by Mike KimutaiMike Kimutai 'Sonko'No ratings yet

- Lecture-4 Financial R&AnalysisDocument46 pagesLecture-4 Financial R&AnalysisinamNo ratings yet

- Cash Management Varun 10808154 Project OnDocument24 pagesCash Management Varun 10808154 Project Ondont_forgetme2004No ratings yet

- Accounts Receivable Management ExplainedDocument12 pagesAccounts Receivable Management ExplainedPurushottam KumarNo ratings yet

- Introduction To AccountingDocument25 pagesIntroduction To Accountingvkvivekkm163No ratings yet

- LESSON 6 Working Capital ManagementDocument25 pagesLESSON 6 Working Capital ManagementKisses BeginoNo ratings yet

- Global Financial ReportingDocument42 pagesGlobal Financial ReportingJay ModiNo ratings yet

- WORKING CAPITAL MANAGEMENET BPFA BCD BSC PM DIPMDocument90 pagesWORKING CAPITAL MANAGEMENET BPFA BCD BSC PM DIPMOreratile KeorapetseNo ratings yet

- Unit 5 Topic 4Document5 pagesUnit 5 Topic 4Ibrahim AbidNo ratings yet

- Working Capital Management: Executive Development ProgramDocument148 pagesWorking Capital Management: Executive Development ProgramsajjukrishNo ratings yet

- Working Capital ManagementDocument52 pagesWorking Capital ManagementPrashanth GowdaNo ratings yet

- Techniques of Cash ManagementDocument11 pagesTechniques of Cash ManagementJANEESHA V VNo ratings yet

- What Is Relationship Banking?Document36 pagesWhat Is Relationship Banking?llllkkkkNo ratings yet

- Why Manage Your Business FinancesDocument2 pagesWhy Manage Your Business FinancesTom John MamaradloNo ratings yet

- Working Capital Management: ConceptDocument22 pagesWorking Capital Management: ConceptshimonmakNo ratings yet

- 2 - FSA1 Handout (Topic 3) - Standard&incomeDocument73 pages2 - FSA1 Handout (Topic 3) - Standard&incomeGuyu PanNo ratings yet

- Cash Flow Forecast NotesDocument11 pagesCash Flow Forecast NoteslebaNo ratings yet

- Managing Construction CashflowDocument43 pagesManaging Construction CashflowomarizaidNo ratings yet

- AmfrDocument25 pagesAmfrPrashant ShokeenNo ratings yet

- Financial Management BasicsDocument21 pagesFinancial Management BasicsSalah StephenNo ratings yet

- Cash Flow ManagementDocument11 pagesCash Flow ManagementYudisthira Bayu PratamaNo ratings yet

- Accounting FOR Managers: Vineetha Raj S1 MBADocument23 pagesAccounting FOR Managers: Vineetha Raj S1 MBAVinu VaviNo ratings yet

- Group 3 - Cash and Marketable SecuritiesDocument71 pagesGroup 3 - Cash and Marketable SecuritiesNaia SNo ratings yet

- Petty CashDocument5 pagesPetty CashMikail Lee BelloNo ratings yet

- Working Capital ManagementDocument34 pagesWorking Capital ManagementPavas SinghalNo ratings yet

- Student - S Trivia Exam 2Document6 pagesStudent - S Trivia Exam 2Marcial Militante100% (1)

- Submission of Complete REportDocument1 pageSubmission of Complete REportMarcial MilitanteNo ratings yet

- Thermodynamics Trivia 2Document5 pagesThermodynamics Trivia 2Marcial MilitanteNo ratings yet

- Table of ContentsDocument1 pageTable of ContentsMarcial MilitanteNo ratings yet

- Terminology (Hvac)Document5 pagesTerminology (Hvac)Marcial MilitanteNo ratings yet

- Subject Code Subject Description Professor: Machine Elements IDocument2 pagesSubject Code Subject Description Professor: Machine Elements IMarcial MilitanteNo ratings yet

- Machines 07 00070Document15 pagesMachines 07 00070Marcial MilitanteNo ratings yet

- Part I. Multiple Choice Questions: Prepared By: Engr. Jose R. Francisco, PMEDocument6 pagesPart I. Multiple Choice Questions: Prepared By: Engr. Jose R. Francisco, PMEMarcial MilitanteNo ratings yet

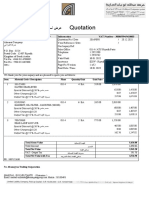

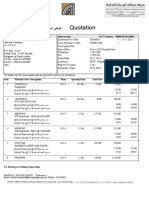

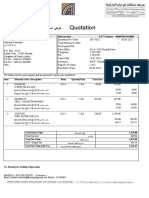

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document2 pagesQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document1 pageQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial Jr. MilitanteNo ratings yet

- Trivia (Elements) 3Document6 pagesTrivia (Elements) 3Marcial MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document2 pagesQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial MilitanteNo ratings yet

- Trivia (Problems) 2Document6 pagesTrivia (Problems) 2Marcial MilitanteNo ratings yet

- 9822/0310 B310-25-1 Loader Arm/Loader Boom 2Nd Intermediate BoomDocument2 pages9822/0310 B310-25-1 Loader Arm/Loader Boom 2Nd Intermediate BoomMarcial MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document1 pageQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial Jr. MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document1 pageQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial Jr. MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document2 pagesQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document2 pagesQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial MilitanteNo ratings yet

- Fuel Injection Pump AssemblyDocument3 pagesFuel Injection Pump AssemblyMarcial MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document1 pageQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial Jr. MilitanteNo ratings yet

- Quotation: Customer Code: 10000604 Information VAT Number - 300055945410003Document1 pageQuotation: Customer Code: 10000604 Information VAT Number - 300055945410003Marcial MilitanteNo ratings yet

- Fuel Pipes HP Assy 3 and 4 InjectorsDocument3 pagesFuel Pipes HP Assy 3 and 4 InjectorsMarcial MilitanteNo ratings yet

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Document1 pageQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial Jr. MilitanteNo ratings yet

- 9822/1045 V610-1-1 FUEL PUMP LIFT 320/25027: Marcial MilitanteDocument3 pages9822/1045 V610-1-1 FUEL PUMP LIFT 320/25027: Marcial MilitanteMarcial MilitanteNo ratings yet

- 9822/1045 V850-5-1 STARTER MOTOR 12V: Marcial MilitanteDocument3 pages9822/1045 V850-5-1 STARTER MOTOR 12V: Marcial MilitanteMarcial MilitanteNo ratings yet

- 9822/1045 V810-7-1 TURBOCHARGER ASSEMBLY 75kW: Marcial MilitanteDocument5 pages9822/1045 V810-7-1 TURBOCHARGER ASSEMBLY 75kW: Marcial MilitanteMarcial MilitanteNo ratings yet

- Pol Cooler and CoverDocument5 pagesPol Cooler and CoverMarcial MilitanteNo ratings yet

- 9822/1045 V710-1-1 AUTOTENSIONER 320/21585 1: Marcial MilitanteDocument3 pages9822/1045 V710-1-1 AUTOTENSIONER 320/21585 1: Marcial MilitanteMarcial MilitanteNo ratings yet

- 9822/1045 V820-1-1 TURBOCHARGER OIL FEED 320/25012/1: Marcial MilitanteDocument3 pages9822/1045 V820-1-1 TURBOCHARGER OIL FEED 320/25012/1: Marcial MilitanteMarcial MilitanteNo ratings yet

- 9822/1045 V410-2-1 WATER PUMP ASSEMBLY: Marcial MilitanteDocument3 pages9822/1045 V410-2-1 WATER PUMP ASSEMBLY: Marcial MilitanteMarcial MilitanteNo ratings yet

- 12 Business Combination Pt2 PDFDocument1 page12 Business Combination Pt2 PDFRiselle Ann SanchezNo ratings yet

- Standard Oil Co. of New York vs. Lopez CasteloDocument1 pageStandard Oil Co. of New York vs. Lopez CasteloRic Sayson100% (1)

- Criticism On Commonly Studied Novels PDFDocument412 pagesCriticism On Commonly Studied Novels PDFIosif SandoruNo ratings yet

- ĐỀ SỐ 6 - KEYDocument6 pagesĐỀ SỐ 6 - KEYAnh MaiNo ratings yet

- Lorax Truax QuestionsDocument2 pagesLorax Truax Questionsapi-264150929No ratings yet

- People vs. Chingh - GR No. 178323 - DigestDocument1 pagePeople vs. Chingh - GR No. 178323 - DigestAbigail TolabingNo ratings yet

- Motion For Re-RaffleDocument3 pagesMotion For Re-RaffleJoemar CalunaNo ratings yet

- Enterprise Risk ManagementDocument59 pagesEnterprise Risk Managementdarshani sandamaliNo ratings yet

- Tutorial Week 3 - WillDocument4 pagesTutorial Week 3 - WillArif HaiqalNo ratings yet

- Climate ChangeDocument3 pagesClimate ChangeBeverly TalaugonNo ratings yet

- Agrarian DisputesDocument15 pagesAgrarian DisputesBryle Keith TamposNo ratings yet

- Managing Transaction ExposureDocument34 pagesManaging Transaction Exposureg00028007No ratings yet

- Kelly Wright hw499 ResumeDocument2 pagesKelly Wright hw499 Resumeapi-526258935No ratings yet

- Color Code Look For Complied With ECE Look For With Partial Compliance, ECE Substitute Presented Look For Not CompliedDocument2 pagesColor Code Look For Complied With ECE Look For With Partial Compliance, ECE Substitute Presented Look For Not CompliedMelanie Nina ClareteNo ratings yet

- Group Floggers Outside The Flogger Abasto ShoppingDocument2 pagesGroup Floggers Outside The Flogger Abasto Shoppingarjona1009No ratings yet

- Windelband, W. - History of Ancient PhilosophyDocument424 pagesWindelband, W. - History of Ancient Philosophyolinto godoyNo ratings yet

- Management Decision Case: Restoration HardwaDocument3 pagesManagement Decision Case: Restoration HardwaRishha Devi Ravindran100% (5)

- 153 - "Authorizing The Utilization ofDocument28 pages153 - "Authorizing The Utilization ofhellomissreeNo ratings yet

- College Hazing Essay 113bDocument6 pagesCollege Hazing Essay 113bapi-283630039No ratings yet

- Intertek India Private LimitedDocument8 pagesIntertek India Private LimitedAjay RottiNo ratings yet

- Invited Discussion On Combining Calcium Hydroxylapatite and Hyaluronic Acid Fillers For Aesthetic IndicationsDocument3 pagesInvited Discussion On Combining Calcium Hydroxylapatite and Hyaluronic Acid Fillers For Aesthetic IndicationsChris LicínioNo ratings yet

- First Aid Is The Provision of Initial Care For An Illness or InjuryDocument2 pagesFirst Aid Is The Provision of Initial Care For An Illness or InjuryBasaroden Dumarpa Ambor100% (2)

- Internship ReportDocument44 pagesInternship ReportRAihan AhmedNo ratings yet

- "Land Enough in The World" - Locke's Golden Age and The Infinite Extension of "Use"Document21 pages"Land Enough in The World" - Locke's Golden Age and The Infinite Extension of "Use"resperadoNo ratings yet

- Islamic StudyDocument80 pagesIslamic StudyWasim khan100% (1)

- Amelia David Chelsea Cruz Ellaine Garcia Rica Mae Magdato Shephiela Mae Enriquez Jamaica Bartolay Jerie Mae de Castro Meryl Manabat Riejel Duran Alexis ConcensinoDocument9 pagesAmelia David Chelsea Cruz Ellaine Garcia Rica Mae Magdato Shephiela Mae Enriquez Jamaica Bartolay Jerie Mae de Castro Meryl Manabat Riejel Duran Alexis ConcensinoRadleigh MercadejasNo ratings yet

- Luovutuskirja Ajoneuvon Vesikulkuneuvon Omistusoikeuden Siirrosta B124eDocument2 pagesLuovutuskirja Ajoneuvon Vesikulkuneuvon Omistusoikeuden Siirrosta B124eAirsoftNo ratings yet

- Causes of UnemploymentDocument7 pagesCauses of UnemploymentBishwaranjan RoyNo ratings yet

- Application For DiggingDocument3 pagesApplication For DiggingDhathri. vNo ratings yet

- PPT7-TOPIK7-R0-An Overview of Enterprise ArchitectureDocument33 pagesPPT7-TOPIK7-R0-An Overview of Enterprise ArchitectureNatasha AlyaaNo ratings yet