You might also like

- 69238asb55316 As10Document26 pages69238asb55316 As10GybcNo ratings yet

- As 10 Revised NotesDocument37 pagesAs 10 Revised NotesIndhuja MNo ratings yet

- Ind AS 16 Property, Plant and Equipment AccountingDocument20 pagesInd AS 16 Property, Plant and Equipment AccountingSandeepPusarapuNo ratings yet

- Accounting SystemDocument14 pagesAccounting SystemPooja MaldeNo ratings yet

- Ias 16Document9 pagesIas 16ADEYANJU AKEEMNo ratings yet

- MAS16Document12 pagesMAS16Kyaw Htin Win50% (2)

- Micro and Other Legal Entities Code of Practice: 0. Taxpayers According To The Accounting ActDocument19 pagesMicro and Other Legal Entities Code of Practice: 0. Taxpayers According To The Accounting ActIvana MatovićNo ratings yet

- IAS 16 Property Plant Equipment AccountingDocument6 pagesIAS 16 Property Plant Equipment AccountinghemantbaidNo ratings yet

- IAS 16 Property, Plant and EquipmentDocument4 pagesIAS 16 Property, Plant and EquipmentSelva Bavani SelwaduraiNo ratings yet

- Nepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Document24 pagesNepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Gemini_0804No ratings yet

- (H) - 3rd Year - BCH 6.4 (DSE-4) - Sem-6 - Financial Reporting and Analysis - Week 4 - Himani DahiyaDocument19 pages(H) - 3rd Year - BCH 6.4 (DSE-4) - Sem-6 - Financial Reporting and Analysis - Week 4 - Himani DahiyaARGHYA MANDALNo ratings yet

- Property, Plant and Equipment: International Accounting Standard 16Document13 pagesProperty, Plant and Equipment: International Accounting Standard 16Tanvir PrantoNo ratings yet

- Banking Technology Information ItDocument13 pagesBanking Technology Information ItMughilan MNo ratings yet

- Accounting Policy as Per FSDocument17 pagesAccounting Policy as Per FSShubham TiwariNo ratings yet

- Indian Accounting Standard 16 Property, Plant & Equipment: By: Rahul DabralDocument9 pagesIndian Accounting Standard 16 Property, Plant & Equipment: By: Rahul DabralMangala BorkarNo ratings yet

- Ias 16 & Ias 40Document47 pagesIas 16 & Ias 40Etiel Films / ኢትኤል ፊልሞች100% (1)

- Test Bank For Fundamental Accounting Principles Canadian Vol 2 Canadian 14Th Edition by Larson Isbn 1259066517 978125906651 Full Chapter PDFDocument36 pagesTest Bank For Fundamental Accounting Principles Canadian Vol 2 Canadian 14Th Edition by Larson Isbn 1259066517 978125906651 Full Chapter PDFherschel.fanno254100% (14)

- Accounting For Plant Assets FinalDocument17 pagesAccounting For Plant Assets FinalAbdii Dhufeera100% (1)

- International Accounting Standard 16 Property, Plant and EquipmentDocument29 pagesInternational Accounting Standard 16 Property, Plant and EquipmentAbdullah Shaker TahaNo ratings yet

- IAS 16 Property Plant and EquipmentDocument13 pagesIAS 16 Property Plant and EquipmentLaura BalcanNo ratings yet

- PA2C2-PA & Dep-Non ACFNDocument33 pagesPA2C2-PA & Dep-Non ACFNSelamNo ratings yet

- DepreciationDocument10 pagesDepreciationsoumibasuNo ratings yet

- DepreciationDocument8 pagesDepreciationbhanu100% (1)

- As 10Document34 pagesAs 10Harsh PatelNo ratings yet

- Accounting Standard 10Document31 pagesAccounting Standard 10Yesha ShahNo ratings yet

- Accounting Standard 6 - DepreciationDocument34 pagesAccounting Standard 6 - DepreciationSarthak Gupta100% (2)

- Mfrs 116 PpeDocument41 pagesMfrs 116 PpeDINIE RUZAINI BINTI MOH ZAINUDIN0% (1)

- Solution Manual CH 08 FInancial Accounting Reporting and Analyzing Long-Term AssetsDocument54 pagesSolution Manual CH 08 FInancial Accounting Reporting and Analyzing Long-Term AssetsSherry AstroliaNo ratings yet

- Libby Financial Accounting Solution Manual Chapter 8 Entire VersionDocument5 pagesLibby Financial Accounting Solution Manual Chapter 8 Entire Versionmercy ko0% (1)

- FoA-CH-III - PPE - 2021Document17 pagesFoA-CH-III - PPE - 2021medhane negaNo ratings yet

- Property, Plant and Equipment: International Accounting Standard 16Document13 pagesProperty, Plant and Equipment: International Accounting Standard 16sdaNo ratings yet

- BBA II Chapter 3 Depreciation AccountingDocument28 pagesBBA II Chapter 3 Depreciation AccountingSiddharth Salgaonkar100% (1)

- Theory of Accounting - SUMMARY of PPEDocument15 pagesTheory of Accounting - SUMMARY of PPESteven Chou100% (2)

- Informe de Ingles Conta Superior 1Document6 pagesInforme de Ingles Conta Superior 1NOELIA CUNYA RONDOYNo ratings yet

- 1944ias 16 2017Document12 pages1944ias 16 2017Md Safayet IslamNo ratings yet

- PP (A) - Lect 2 - Ias 16 PpeDocument19 pagesPP (A) - Lect 2 - Ias 16 Ppekevin digumberNo ratings yet

- Survey of Accounting 5th Edition Edmonds Solutions ManualDocument65 pagesSurvey of Accounting 5th Edition Edmonds Solutions Manualmoriskledgeusud100% (20)

- Survey of Accounting 5Th Edition Edmonds Solutions Manual Full Chapter PDFDocument67 pagesSurvey of Accounting 5Th Edition Edmonds Solutions Manual Full Chapter PDFzanewilliamhzkbr100% (6)

- Ias 16 - PpeDocument4 pagesIas 16 - Ppecar itselfNo ratings yet

- Chapter 5 IFA NEWDocument17 pagesChapter 5 IFA NEWabdum1928No ratings yet

- Depreciation AccountingDocument42 pagesDepreciation AccountingGaurav SharmaNo ratings yet

- Summary PpeDocument8 pagesSummary PpeJenilyn CalaraNo ratings yet

- Accounting for Property, Plant and EquipmentDocument21 pagesAccounting for Property, Plant and Equipmentumarsaleem92No ratings yet

- Fixed AssetsDocument46 pagesFixed AssetsSprancenatu Lavinia0% (1)

- Accounting ch10 Solutions QuestionsDocument57 pagesAccounting ch10 Solutions Questionsaboodyuae2000No ratings yet

- Accounting StandardDocument9 pagesAccounting StandardVanshika GaneriwalNo ratings yet

- CH 5 Depreciation and AmortisationDocument50 pagesCH 5 Depreciation and AmortisationdeepakNo ratings yet

- Chap 010Document54 pagesChap 010MubasherAkramNo ratings yet

- ACC201 PPTs - 1T2018 - Workshop 07 - Week 08Document18 pagesACC201 PPTs - 1T2018 - Workshop 07 - Week 08Luu MinhNo ratings yet

- AS - 10 Property Plant Equipment Lyst6953Document18 pagesAS - 10 Property Plant Equipment Lyst6953Shubham ChauhanNo ratings yet

- GST Circular From IATODocument26 pagesGST Circular From IATOVivekanandNo ratings yet

- LESSON3Document19 pagesLESSON3Ira Charisse BurlaosNo ratings yet

- DocumentDocument17 pagesDocumentAdmNo ratings yet

- Property, Plant and Equipment AccountingDocument10 pagesProperty, Plant and Equipment Accountingbhettyna noayNo ratings yet

- Chapter 2-Plant assets and intangible assetsDocument15 pagesChapter 2-Plant assets and intangible assetsyared kebedeNo ratings yet

- Accounting for Property, Plant and EquipmentDocument26 pagesAccounting for Property, Plant and EquipmentJellai TejeroNo ratings yet

- PSBA - Property, Plant and EquipmentDocument13 pagesPSBA - Property, Plant and EquipmentAbdulmajed Unda MimbantasNo ratings yet

- Fixed AssetDocument25 pagesFixed AssetSisay Belong To JesusNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Lecturer-Led Tutorial Chapter 5 (2023)Document9 pagesLecturer-Led Tutorial Chapter 5 (2023)Ncebakazi DawedeNo ratings yet

- Maintaining Price Stability Ensuring Adequate Flow of Credit To The Productive Sectors of The Economy To Support Economic Growth Financial StabilityDocument54 pagesMaintaining Price Stability Ensuring Adequate Flow of Credit To The Productive Sectors of The Economy To Support Economic Growth Financial Stabilityfrancis reddyNo ratings yet

- LiabilitiesDocument2 pagesLiabilitiesFrederick AbellaNo ratings yet

- Director Business Development in West Palm Beach FL Resume Charles MillerDocument1 pageDirector Business Development in West Palm Beach FL Resume Charles MillerCharlesMiller2No ratings yet

- Rencana Bisnis Art Box Creative and Coworking SpaceDocument2 pagesRencana Bisnis Art Box Creative and Coworking SpacesupadiNo ratings yet

- Annuity (PMT)Document54 pagesAnnuity (PMT)bayu fajarNo ratings yet

- ACCT 101 Chapter 1 HandoutDocument3 pagesACCT 101 Chapter 1 HandoutLlana RoxanneNo ratings yet

- Financial Management Basics of Risk and ReturnDocument10 pagesFinancial Management Basics of Risk and ReturnHenok FikaduNo ratings yet

- Financial RatiosDocument30 pagesFinancial RatiosVenz LacreNo ratings yet

- Primary Dealer System - A Comparative StudyDocument5 pagesPrimary Dealer System - A Comparative Studyprateek.karaNo ratings yet

- Bonds valuation and amortization assessmentDocument2 pagesBonds valuation and amortization assessmentJohn FloresNo ratings yet

- S6-10 Digital Lending - Lending Club and AffirmDocument22 pagesS6-10 Digital Lending - Lending Club and AffirmVivek SinghNo ratings yet

- Brac Bank PresentationDocument24 pagesBrac Bank PresentationSumi Islam100% (2)

- Problems Chapter 11Document29 pagesProblems Chapter 11Incia100% (1)

- Chapter 15 Using Management and Accounting InformationDocument22 pagesChapter 15 Using Management and Accounting InformationPete JoempraditwongNo ratings yet

- Q.Discuss The Various Sources of Financing Working Capital. (OR) Q. Explain The Sources of Financing of Current AssetsDocument5 pagesQ.Discuss The Various Sources of Financing Working Capital. (OR) Q. Explain The Sources of Financing of Current AssetsSiva SankariNo ratings yet

- 123 PDFDocument9 pages123 PDFKhusru ShahbazNo ratings yet

- HH HDocument2 pagesHH HPrashant UpadhyayNo ratings yet

- Valet Parking Locations UAEDocument3 pagesValet Parking Locations UAEvineet sharmaNo ratings yet

- Alert Company S Shareholders Equity Prior To Any of The Following PDFDocument1 pageAlert Company S Shareholders Equity Prior To Any of The Following PDFHassan JanNo ratings yet

- CH 17Document23 pagesCH 17SaAl-ismailNo ratings yet

- Basel IiiDocument32 pagesBasel Iiivenkatesh pkNo ratings yet

- 2800021Document2 pages2800021Daood AbdullahNo ratings yet

- Role of Tech in Promoting Financial InclusionDocument66 pagesRole of Tech in Promoting Financial InclusionKheang VesalNo ratings yet

- Banking Regulation Act 1949Document13 pagesBanking Regulation Act 1949jhumli0% (1)

- AssignmentDocument8 pagesAssignmentSundas MashhoodNo ratings yet

- 2018 March B.com CBCSS Fifth Sem Special Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Document4 pages2018 March B.com CBCSS Fifth Sem Special Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Rainy GoodwillNo ratings yet

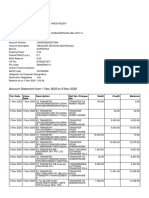

- Account Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancevinod reddyNo ratings yet

- Annual Report: Ekuiti Nasional BerhadDocument131 pagesAnnual Report: Ekuiti Nasional BerhadFiruz Abd RahimNo ratings yet