You might also like

- CreditCardStatement PDFDocument3 pagesCreditCardStatement PDFrupal100% (1)

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- Pad Eye New ReleaseDocument10 pagesPad Eye New ReleaseEnrique BarajasNo ratings yet

- Financial Ratio Analysis of Bank Performance PDFDocument24 pagesFinancial Ratio Analysis of Bank Performance PDFRatnesh Singh100% (1)

- Financial Ratio Analysis of Bank Performance PDFDocument24 pagesFinancial Ratio Analysis of Bank Performance PDFRatnesh Singh100% (1)

- Financial Instruments by Sir AB JanjuaDocument14 pagesFinancial Instruments by Sir AB JanjuaMian Sajjad100% (1)

- Business Reporting July 2013 Marks Plan1Document28 pagesBusiness Reporting July 2013 Marks Plan1karlr9No ratings yet

- Debt Securities ReviewerDocument30 pagesDebt Securities Reviewerjhie boterNo ratings yet

- Tutorial On Ratio AnalysisDocument4 pagesTutorial On Ratio AnalysisRajyaLakshmiNo ratings yet

- Ch. 1-Fundamentals of Accounting IDocument20 pagesCh. 1-Fundamentals of Accounting IDèřæ Ô MáNo ratings yet

- SWOT Analysis TemplateDocument3 pagesSWOT Analysis Templaterwl s.r.l100% (1)

- FSA Vertical FormatDocument10 pagesFSA Vertical FormatMayank BahetiNo ratings yet

- UntitledDocument2 pagesUntitledAli Mubin FitranandaNo ratings yet

- Accounting For Managers Trimester 1 Mba Ktu 2016Document3 pagesAccounting For Managers Trimester 1 Mba Ktu 2016Mekhajith MohanNo ratings yet

- Quiz 2 Cashflows Final PDFDocument4 pagesQuiz 2 Cashflows Final PDFChito MirandaNo ratings yet

- Vertical Financial StatementsDocument3 pagesVertical Financial StatementsMANAN MEHTANo ratings yet

- RATIO ANALYSIS Q 1 To 4Document5 pagesRATIO ANALYSIS Q 1 To 4gunjan0% (1)

- Ratio Problems 1Document6 pagesRatio Problems 1Vivek MathiNo ratings yet

- Zinnia Ltd. Has Furnished Its Income Statement and Balance Sheet For The Year Ended 31 March 2012Document3 pagesZinnia Ltd. Has Furnished Its Income Statement and Balance Sheet For The Year Ended 31 March 2012Amit GodaraNo ratings yet

- Business Combination Accounted For Under The Equity MethodDocument4 pagesBusiness Combination Accounted For Under The Equity MethodMixx MineNo ratings yet

- Acctg110 FinalsDocument21 pagesAcctg110 FinalsRoman Dominic LlanoNo ratings yet

- Vertical BfsDocument4 pagesVertical BfsKrüpãl MãñgrùlêNo ratings yet

- Accounting Exercises On Cash FlowsDocument2 pagesAccounting Exercises On Cash FlowsMicaella GoNo ratings yet

- Ali Mubin Fitrananda - 2210312310066 - Trade Company Case For FR - AccountingDocument8 pagesAli Mubin Fitrananda - 2210312310066 - Trade Company Case For FR - AccountingAli Mubin FitranandaNo ratings yet

- CSS Ratio AnalysisDocument9 pagesCSS Ratio AnalysisMasood Ahmad AadamNo ratings yet

- MA Sem-4 2018-2019Document23 pagesMA Sem-4 2018-2019Akki GalaNo ratings yet

- Cash Flow Statement-ExampleDocument18 pagesCash Flow Statement-ExampleAnakha RadhakrishnanNo ratings yet

- CHP 2AnalysisInterpretationofAccountsDocument5 pagesCHP 2AnalysisInterpretationofAccountsalpeshmahto2004No ratings yet

- Cash Flow Statement QuestionDocument1 pageCash Flow Statement QuestionVarunNo ratings yet

- Internal Question Bank MA 2022Document7 pagesInternal Question Bank MA 2022singhalsanchit321No ratings yet

- Revision Pack QuestionsDocument12 pagesRevision Pack QuestionsAmmaarah PatelNo ratings yet

- Accounting Paper-Zoom 2Document7 pagesAccounting Paper-Zoom 2Sufyan SheikhNo ratings yet

- Net Working Capital Current Assets - Current LiabilitiesDocument11 pagesNet Working Capital Current Assets - Current LiabilitiesRahul YadavNo ratings yet

- Question Bank - Financial Reporting and AnalysisDocument8 pagesQuestion Bank - Financial Reporting and AnalysisSagar BhandareNo ratings yet

- Unit IIIDocument9 pagesUnit IIIkuselvNo ratings yet

- "Knowledge Is Superior To Marks",: PrefaceDocument12 pages"Knowledge Is Superior To Marks",: PrefaceTapan BarikNo ratings yet

- Bac 203 Cat 2Document3 pagesBac 203 Cat 2Brian MutuaNo ratings yet

- Ratio AnalysisDocument7 pagesRatio AnalysisDEEPA KUMARINo ratings yet

- Aspire CR - Conso Question - Bank - Nov 21Document12 pagesAspire CR - Conso Question - Bank - Nov 21Richie BoomaNo ratings yet

- FABM1 11 Quarter 4 Week 6 Las 3Document4 pagesFABM1 11 Quarter 4 Week 6 Las 3Janna PleteNo ratings yet

- JKN - Acc - 13 - Question Paper - 131020Document10 pagesJKN - Acc - 13 - Question Paper - 131020adityatiwari122006No ratings yet

- Financial Statement Analysis Probs On Funds Flow Analysis PDFDocument15 pagesFinancial Statement Analysis Probs On Funds Flow Analysis PDFSAITEJA ANUGULANo ratings yet

- Final AccountsDocument9 pagesFinal AccountsAbhinav Kumar YadavNo ratings yet

- 2018-06 ICMAB FL 001 PAC Year Question JUNE 2018Document4 pages2018-06 ICMAB FL 001 PAC Year Question JUNE 2018Mohammad ShahidNo ratings yet

- Proposed DividebdDocument34 pagesProposed DividebdPiyush SrivastavaNo ratings yet

- Business Combi PDF FreeDocument13 pagesBusiness Combi PDF FreeEricka RedoñaNo ratings yet

- Tugas 1 Lab Auditing OkDocument9 pagesTugas 1 Lab Auditing OkIrmalia Anastasia SiagianNo ratings yet

- F M ADocument11 pagesF M AAjay SahooNo ratings yet

- Profit and Loss Account For The Year Ended 31.03.2016 Particulars Amount Particulars Amount (Rs '000's) (Rs '000's)Document3 pagesProfit and Loss Account For The Year Ended 31.03.2016 Particulars Amount Particulars Amount (Rs '000's) (Rs '000's)Sushant SaxenaNo ratings yet

- 12th Cbse Accounts Paper 10 06 2017Document2 pages12th Cbse Accounts Paper 10 06 2017Harpreet Singh SainiNo ratings yet

- Attempt All Questions: Summer Exam-2015Document25 pagesAttempt All Questions: Summer Exam-2015ag swlNo ratings yet

- Ratio Analysis-1Document4 pagesRatio Analysis-1Aakash RamakrishnanNo ratings yet

- 2021 Business AccountingDocument5 pages2021 Business AccountingVISHESH 0009No ratings yet

- BBS 1st Year QuestionDocument2 pagesBBS 1st Year Questionsatya100% (1)

- RatioanalysisanswersDocument5 pagesRatioanalysisanswersAnu PriyaNo ratings yet

- FFS - NumericalsDocument5 pagesFFS - NumericalsFunny ManNo ratings yet

- Accountancy Auditing 2018Document7 pagesAccountancy Auditing 2018Abdul basitNo ratings yet

- Accounting Class Test 1.: DATE:10 APRIL, 2020 TIME: 1:hours MARKS: 30 Total No. of Questions: 3 Total No. of Pages: 03Document3 pagesAccounting Class Test 1.: DATE:10 APRIL, 2020 TIME: 1:hours MARKS: 30 Total No. of Questions: 3 Total No. of Pages: 03Mandeep KaurNo ratings yet

- Fabm2 First Grading ReviewerDocument3 pagesFabm2 First Grading ReviewerjhomarNo ratings yet

- Finals Quiz #2 Soce, Soci, Ahfs and Do Multiple Choice: Account Title AmountDocument3 pagesFinals Quiz #2 Soce, Soci, Ahfs and Do Multiple Choice: Account Title AmountNew TonNo ratings yet

- Cash Flow NewDocument4 pagesCash Flow NewAnkur GoyalNo ratings yet

- Financial AnalysisDocument15 pagesFinancial AnalysisRONALD SSEKYANZINo ratings yet

- Unit 3 - Business Finance - AppendixDocument5 pagesUnit 3 - Business Finance - Appendixmhmir9.95No ratings yet

- Incomplete RecordsDocument32 pagesIncomplete RecordsSunil KumarNo ratings yet

- Ratio Analysis ProblemsDocument4 pagesRatio Analysis ProblemsNavya SreeNo ratings yet

- Example CH 2Document1 pageExample CH 2HananNo ratings yet

- ABCDDocument4 pagesABCDYaseen Nazir MallaNo ratings yet

- Intacc 3 Fs ProblemsDocument25 pagesIntacc 3 Fs ProblemsUn knownNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Modul APSI - SDLCDocument10 pagesModul APSI - SDLCHafizh ArdiNo ratings yet

- System - Designing PrasentationDocument2 pagesSystem - Designing Prasentationrwl s.r.lNo ratings yet

- Management Information System May4Document23 pagesManagement Information System May4Jeeva MJNo ratings yet

- MIS ... in A NutshellDocument48 pagesMIS ... in A NutshellmwekezajiNo ratings yet

- Business System AssignmentDocument6 pagesBusiness System Assignmentrwl s.r.lNo ratings yet

- Management Information System May4Document23 pagesManagement Information System May4Jeeva MJNo ratings yet

- WHO Stake Holder AnalysisDocument378 pagesWHO Stake Holder AnalysisPurushothmanNo ratings yet

- 2015 AFR AnswersDocument7 pages2015 AFR Answersrwl s.r.lNo ratings yet

- WK 1Document24 pagesWK 1rwl s.r.lNo ratings yet

- Non-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model AnswersDocument8 pagesNon-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model Answersrwl s.r.lNo ratings yet

- 2014 AFR AnswersDocument8 pages2014 AFR Answersrwl s.r.lNo ratings yet

- ReadmeDocument1 pageReadmerwl s.r.lNo ratings yet

- 2013 AFR AnswersDocument8 pages2013 AFR Answersrwl s.r.lNo ratings yet

- Corporate Social Responsibilit1Document4 pagesCorporate Social Responsibilit1umeshNo ratings yet

- CreditCardStatement 3Document4 pagesCreditCardStatement 3rwl s.r.lNo ratings yet

- Sampath SimplifiedDocument392 pagesSampath SimplifiedumeshNo ratings yet

- Agency Law: Third-Party General Agent Special Agent Mandate Principal Agent Procuratio MandatumDocument37 pagesAgency Law: Third-Party General Agent Special Agent Mandate Principal Agent Procuratio Mandatumrwl s.r.lNo ratings yet

- Corporate Social Responsibilit1Document4 pagesCorporate Social Responsibilit1rwl s.r.lNo ratings yet

- Read MeDocument3 pagesRead Merwl s.r.lNo ratings yet

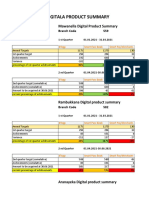

- Ratnapura Area - Digitala Product SummaryDocument12 pagesRatnapura Area - Digitala Product Summaryrwl s.r.lNo ratings yet

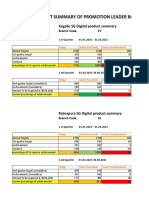

- Kegalle Area - Digitala Product SummaryDocument12 pagesKegalle Area - Digitala Product Summaryrwl s.r.lNo ratings yet

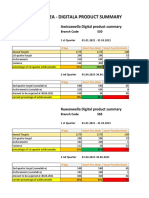

- Avissawella Area SummaryDocument13 pagesAvissawella Area Summaryrwl s.r.lNo ratings yet

- Digitala Product Summary of Promotion Leader BoardDocument2 pagesDigitala Product Summary of Promotion Leader Boardrwl s.r.lNo ratings yet

- Embilipitiya Area - Digitala Product SummaryDocument14 pagesEmbilipitiya Area - Digitala Product Summaryrwl s.r.lNo ratings yet

- Acquiring New Knowledge: Module 26 AgricultureDocument10 pagesAcquiring New Knowledge: Module 26 AgricultureAngelica Sanchez de VeraNo ratings yet

- Non Current Asset Held For SaleDocument27 pagesNon Current Asset Held For SaleAbdulmajed Unda MimbantasNo ratings yet

- IA2 20 Shareholders' EquityDocument61 pagesIA2 20 Shareholders' EquityLawrence NarvaezNo ratings yet

- Unilever TodayDocument34 pagesUnilever TodayEmee Haque50% (2)

- Practice 2AssetAcquisitionDocument11 pagesPractice 2AssetAcquisitionEllen KokaliNo ratings yet

- Chapter 15 AFAR SOLMAN (DAYAG 2015ed) - PROB 3 Case 3 & 4Document2 pagesChapter 15 AFAR SOLMAN (DAYAG 2015ed) - PROB 3 Case 3 & 4Ma Teresa B. CerezoNo ratings yet

- Advanced Accounting 11th Edition Hoyle Test Bank Full Chapter PDFDocument67 pagesAdvanced Accounting 11th Edition Hoyle Test Bank Full Chapter PDFToniPerryyedo100% (12)

- Cfas With AnsDocument20 pagesCfas With AnsFlehzy EstollosoNo ratings yet

- AFA CH 2Document60 pagesAFA CH 2Amaa Amaa100% (2)

- Biological AssetsDocument17 pagesBiological Assetsjmtiquio15No ratings yet

- Session 6 Assets Part 2 - Intangilbe and Investments (Marked Up)Document38 pagesSession 6 Assets Part 2 - Intangilbe and Investments (Marked Up)Kothari InvestmentsNo ratings yet

- AGTL - 2009 Al Ghazi Tractors Limited OpenDoors - PKDocument30 pagesAGTL - 2009 Al Ghazi Tractors Limited OpenDoors - PKMubashar TNo ratings yet

- Spotlight On Telecommunications AccountingDocument8 pagesSpotlight On Telecommunications AccountingHasan YasinNo ratings yet

- Suggested Answer CAP II Dec 2017Document109 pagesSuggested Answer CAP II Dec 2017Sushant MaskeyNo ratings yet

- Statement of Comprehensive Income - ValixDocument7 pagesStatement of Comprehensive Income - ValixYstefani ValderamaNo ratings yet

- Guidance Note On Derivative AccountingDocument9 pagesGuidance Note On Derivative AccountingHimanshu AggarwalNo ratings yet

- Eb Kiesofinaccifrs2ed Chapter 01Document48 pagesEb Kiesofinaccifrs2ed Chapter 01CamyNo ratings yet

- Ind-AS 19Document42 pagesInd-AS 19amarNo ratings yet

- cONCEPTUAL fRAMEWORK FasbDocument9 pagescONCEPTUAL fRAMEWORK FasbFauzanUlvaNo ratings yet

- Practical Accounting 1Document3 pagesPractical Accounting 1LyricVideoNo ratings yet

- Chapter 13 - IAS 12Document54 pagesChapter 13 - IAS 12Bahader AliNo ratings yet

- PSAK 16 EnglishDocument21 pagesPSAK 16 EnglishToko Hanafi50% (2)

- 94 - AFAR Preweek LectureDocument18 pages94 - AFAR Preweek LectureBarbado ArleneNo ratings yet

- Financial Asset at Fair ValueDocument10 pagesFinancial Asset at Fair ValuePgumballNo ratings yet