You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Nguyễn Thành Trung Internship report AutosavedDocument41 pagesNguyễn Thành Trung Internship report AutosavedNguyễn Thanh PhươngNo ratings yet

- Taxation - Ins 3010: Group 2Document10 pagesTaxation - Ins 3010: Group 2nguyễnthùy dươngNo ratings yet

- Fianl Thesis InternshipDocument41 pagesFianl Thesis InternshipNguyễn Thanh PhươngNo ratings yet

- 5. Mẫu làm báo cáo, nhận xét gửi SVDocument6 pages5. Mẫu làm báo cáo, nhận xét gửi SVNguyễn Thanh PhươngNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Financial Metrics ExampleDocument2 pagesFinancial Metrics ExampleSourav shabuNo ratings yet

- Rategain 17052022121031 RG Ip 17052022Document51 pagesRategain 17052022121031 RG Ip 17052022Khustra ParveenNo ratings yet

- Business Finance Assignment EnaaDocument4 pagesBusiness Finance Assignment EnaaEna Bandyopadhyay100% (1)

- Ey Good Group Alternative Format 2021Document163 pagesEy Good Group Alternative Format 2021Michael Boules100% (1)

- F9 - Mock B - QuestionsDocument7 pagesF9 - Mock B - QuestionspavishneNo ratings yet

- 06 Actvity 1 1Document4 pages06 Actvity 1 14mpspxd5msNo ratings yet

- vW3 bb4EEemddAqBQMk Og Module-6-Example-Cases-SolutionsDocument53 pagesvW3 bb4EEemddAqBQMk Og Module-6-Example-Cases-SolutionsSonali AgarwalNo ratings yet

- New Research - MarchDocument8 pagesNew Research - MarchPradeep Rawat100% (1)

- Explain The Basic Features of Income and Expenditure Account and of Receipt and Payment AccountDocument2 pagesExplain The Basic Features of Income and Expenditure Account and of Receipt and Payment AccountSumit Goyal100% (1)

- Dividend Decision (India Bulls)Document9 pagesDividend Decision (India Bulls)Balakrishna ChakaliNo ratings yet

- Our Lady of The Pillar College Cauayan: Prelim Examination Accounting 1 &2Document8 pagesOur Lady of The Pillar College Cauayan: Prelim Examination Accounting 1 &2John Lloyd LlananNo ratings yet

- Intermediate Accounting 1 Final ExaminationDocument9 pagesIntermediate Accounting 1 Final ExaminationPearlyn Villarin100% (1)

- Week 4 Balance OffDocument16 pagesWeek 4 Balance OffNor LailyNo ratings yet

- Corporate FinanceDocument245 pagesCorporate FinanceLazarus AmaniNo ratings yet

- Finland Highlight TaxDocument9 pagesFinland Highlight TaxDogeNo ratings yet

- Assignment On Corporate GovernanceDocument22 pagesAssignment On Corporate GovernanceRakib TusharNo ratings yet

- Fakulti Ekonomi Dan Pengurusan Eppd1033 Prinsip Perakaunan Tutorial 6 Topic: MerchandisingDocument4 pagesFakulti Ekonomi Dan Pengurusan Eppd1033 Prinsip Perakaunan Tutorial 6 Topic: MerchandisingHani Syazani B. Kamarudin ArifinNo ratings yet

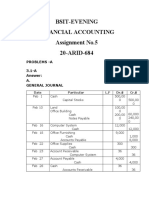

- Assignment No.5 AccountingDocument6 pagesAssignment No.5 Accountingibrar ghaniNo ratings yet

- Swisstek (Ceylon) PLC Swisstek (Ceylon) PLCDocument7 pagesSwisstek (Ceylon) PLC Swisstek (Ceylon) PLCkasun witharanaNo ratings yet

- Project Topics For Mutual Funds: A Study of Selected Indian Public Sector and Private Sector Banks Using Camel ModelDocument3 pagesProject Topics For Mutual Funds: A Study of Selected Indian Public Sector and Private Sector Banks Using Camel ModelShashank Pal100% (1)

- No Par Value Stock DefinitionDocument2 pagesNo Par Value Stock DefinitionblezylNo ratings yet

- Quiz For BAACCENDocument4 pagesQuiz For BAACCENJolyna E. AduanaNo ratings yet

- Final ProjectDocument59 pagesFinal Projectarchit sahayNo ratings yet

- Fantasy Fashions Had Used The Lifo Method of Costing InventoriesDocument6 pagesFantasy Fashions Had Used The Lifo Method of Costing Inventorieslaale dijaanNo ratings yet

- Income Statement To The NetDocument26 pagesIncome Statement To The NetOman SherNo ratings yet

- Chapter 6Document17 pagesChapter 6Yusuf Raharja100% (1)

- (VAL. METH.) I. Fundamental Principles of Valuation & II. Asset Valuation MethodsDocument15 pages(VAL. METH.) I. Fundamental Principles of Valuation & II. Asset Valuation MethodsJoanne SunielNo ratings yet

- The Accounting Equation and The Double-Entry SystemDocument24 pagesThe Accounting Equation and The Double-Entry SystemJohn Mark MaligaligNo ratings yet

- CH 8 Palepu JW C PDFDocument14 pagesCH 8 Palepu JW C PDFcherry wineNo ratings yet

- Fauji Fertilizer Company LimitedDocument12 pagesFauji Fertilizer Company Limitednadeemaccacfe100% (1)